|

시장보고서

상품코드

2034999

인도의 건설장비 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Construction Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

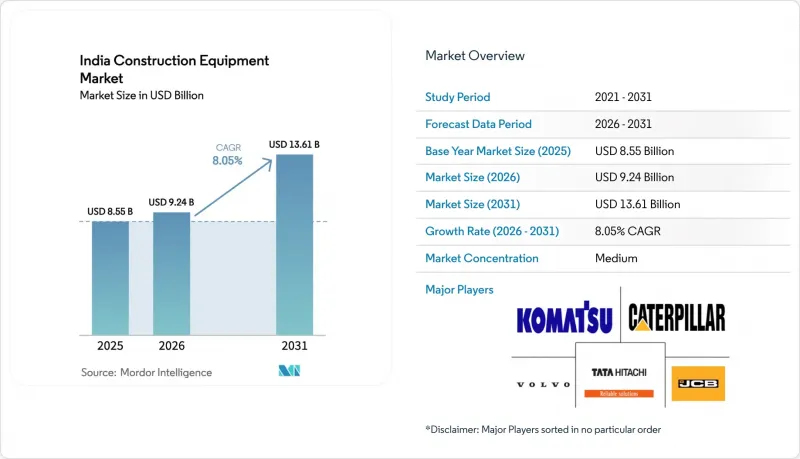

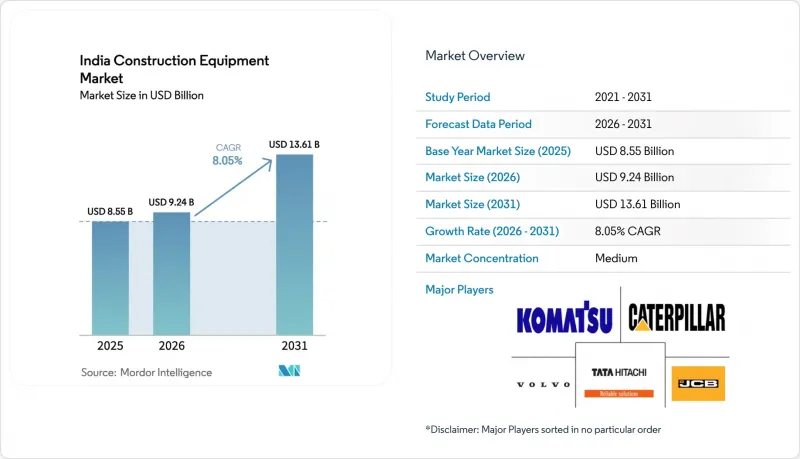

인도의 건설장비 시장 규모는 2025년 85억 5,000만 달러에서 2026년에는 92억 4,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 8.05%로 성장을 지속하여, 2031년까지 136억 1,000만 달러에 이를 것으로 예측됩니다.

이러한 성장의 배경에는 1조 4,000억 달러 규모의 '국가 인프라 계획'이 있으며, 이는 토목, 도로 건설, 자재 운반용 기계 수주를 가속화하고 있습니다. 2025년에 도입된 보다 엄격한 CEV Stage V 배출가스 규제는 청정 구동 시스템에 대한 투자를 촉진하고, 현지화 프로그램은 공급망을 단축하고 수입 비용을 억제할 수 있습니다. 정부가 북동부 지역에 대한 자금 배분을 추진하고, 광업 개혁이 고출력 장비에 대한 수요 기회를 창출하고, 렌탈 플랫폼이 소규모 계약업체에 대한 접근성을 확대함에 따라 지역별 수요 추세가 변화하고 있습니다.

인도의 건설장비 시장 동향과 인사이트

정부 주도의 메가 인프라 프로젝트

국가 인프라 계획에는 교통, 에너지, 도시 부문에 걸쳐 9,742건, 총 3조 8천억 달러 규모의 프로젝트가 포함되어 있습니다. 이 계획에 힘입어 2023-24 회계연도 기계 판매는 26% 증가했으며, 그 중 토목 기계와 도로 마감 기계가 견인차 역할을 했습니다. 델리-뭄바이 산업 회랑과 바랏말라 1단계와 같은 주요 회랑에서만 미화 1,720억 달러의 지출이 발생했으며, 이는 굴삭기, 백호 로더, 컴팩터에 대한 지속적인 수요를 견인하고 있습니다.

2, 3급 도시의 급속한 도시화

중산층의 라크나우, 자이푸르, 코임바토르 등 도시로의 이주에 따라 고층 주택 착공 건수는 2023년 대비 35% 증가할 것으로 예측됐습니다. 이러한 협소한 부지에서는 좁은 공간에서도 기동성이 뛰어난 소형 굴삭기, 트럭 크레인, 텔레핸들러가 선호됩니다. 설치 면적이 작고, 텔레매틱스를 활용한 안전 기능을 갖춘 장비 제조업체들이 이 도시 재개발 붐에서 점유율을 확대되고 있습니다.

철강 가격 변동

철강 가격의 변동은 시장 성장의 중요한 제약 요인으로 부상하고 있습니다. 건설장비 제조원가 중 원재료비가 60-65%를 차지하기 때문입니다. 단기간에 15-20%의 가격 변동이 발생하면 생산 계획이 혼란스러워지고, OEM 업체, 특히 헤지 능력이 제한적인 국내 업체들의 수익률이 압박을 받게 됩니다. 이러한 비용 압박은 최종 사용자에게 전가되는 경향이 강해지고 있으며, 2024년 기계 가격은 전년 대비 8-12% 상승할 것으로 예측됐습니다. 또한, CEV Stage V 배출가스 규제 도입으로 인해 기계 비용이 12-15% 더 증가할 것으로 예상되어 상황이 더욱 복잡해지고 있습니다(4).

부문 분석

토공기계는 2025년 판매량의 56.62%를 차지했습니다. 백호 로더만 해도 판매량의 절반 이상을 차지하며, 굴착, 도랑 파기, 경미한 리프팅 작업에서 그 다재다능함을 입증하고 있습니다. 도로건설장비는 고속도로 및 간선도로 프로젝트가 가속화되면서 연간 40%의 가장 가파른 성장세를 기록했습니다. 그러나 도로 건설장비는 2031년까지 연평균 복합 성장률(CAGR) 10.05%로 확대될 것으로 예측됩니다.

토목기계는 인프라, 광업, 부동산 등 다양한 분야에서 활용도가 높아 인도의 건설장비 시장의 근간을 이루고 있습니다. 한편, 물류단지와 항만의 현대화에 따라 휠로더, 지게차, 리치 스태커에 대한 수요가 증가하면서 자재관리 기계의 판매량이 급증하고 있습니다. 텔레매틱스 도입이 빠르게 진행되면서 과거 '단순한 기계'가 가동 중단 시간과 연료 소비를 줄이는 커넥티드 자산으로 변모하고 있습니다.

2025년에는 디젤 유압식 리그가 전체 납품량의 94.72%를 차지할 것으로 예측됐습니다. 이는 잘 구축된 연료 인프라와 입증된 견고성을 바탕으로 한 것입니다. 그러나 전기/하이브리드 장비는 출하량의 5.28%에 불과하지만, OEM 업체들이 Stage V 규제를 준수하는 로더, 컴팩터, 미니 굴삭기를 잇달아 출시하면서 CAGR 15.68%로 확대되고 있습니다.

배터리 밀도의 향상, 건설 현장의 모듈식 충전 컨테이너 도입, 배출가스 규제 강화로 인해 구매자의 경제성은 무공해 기계로 기울어지고 있습니다. 도시철도 및 공항 건설의 초기 도입자들은 라이프사이클 비용 절감과 엄격한 소음 및 배기가스 규제가 부과되는 도시 프로젝트에서 컴플라이언스의 용이성을 꼽고 있습니다. 인도의 건설장비 시장에서 전기 모델 시장 규모는 2031년까지 3배로 증가할 것으로 예측됩니다.

인도의 건설장비 시장은 기계 유형(토공 기계, 도로 건설 기계, 자재 운반 기계, 콘크리트 기계, 자재 가공 및 파쇄 기계), 구동 방식(기존 유압/디젤 등), 최종 사용자 산업, 출력 등급, 소유 형태, 지역별로 세분화되어 있습니다. 시장 예측은 금액(USD) 및 수량(대수)으로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액, 10억 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Indian construction equipment market size is expected to grow from USD 8.55 billion in 2025 to USD 9.24 billion in 2026 and is forecast to reach USD 13.61 billion by 2031 at 8.05% CAGR over 2026-2031.

Growth is underpinned by the National Infrastructure Pipeline, a USD 1.4 trillion program accelerating orders for earthmoving, road-building, and material-handling machinery. Stricter CEV Stage V emission norms in 2025 catalyze investment in cleaner drive systems while localization programs shorten supply chains and temper import costs. Regional demand is shifting as the government channels funds toward the North-East, mining reforms open high-horsepower equipment opportunities, and rental platforms broaden access for small contractors.

India Construction Equipment Market Trends and Insights

Government-led Mega Infrastructure Projects

The National Infrastructure Pipeline spans 9,742 projects worth USD 3.08 trillion across transport, energy and urban sectors. Equipment sales jumped 26% in FY 2023-24 on the back of this pipeline, led by earthmoving machines and road finishers. Flagship corridors such as the Delhi-Mumbai Industrial Corridor and Bharatmala Phase I alone account for USD 172 billion of spending and drive sustained demand for excavators, backhoe loaders and compactors.

Rapid Urbanization in Tier II & III Cities

Middle-class migration to cities such as Lucknow, Jaipur, and Coimbatore is pushing high-rise residential starts 35% higher than 2023 levels. These constrained sites favor compact excavators, truck-mounted cranes, and telehandlers that maneuver in tight spaces. Equipment makers offering smaller footprints and telematics-enabled safety features are capturing share in this urban infill wave.

Volatile Steel Prices

Steel price volatility has emerged as a critical constraint on market growth, with raw material costs accounting for 60-65% of construction equipment manufacturing expenses. Price fluctuations of 15-20% within short timeframes have disrupted production planning and eroded profit margins for OEMs, particularly domestic manufacturers with limited hedging capabilities. These cost pressures are increasingly being passed on to end-users, with equipment prices rising by 8-12% in 2024 compared to the previous year.The situation is further complicated by the implementation of CEV Stage V emission norms, which is expected to add another 12-15% to equipment costs[4].

Other drivers and restraints analyzed in the detailed report include:

- Mining Sector Reforms

- Fast-Track Road Corridor Execution

- Persistent Land Acquisition Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Earthmoving machinery generated 56.62% of 2025 unit sales. Backhoe loaders alone secured more than half of that volume, a testament to their versatility in excavation, trenching, and minor lifting tasks. Road-building equipment, logged the sharpest 40% annual growth as highway and corridor projects accelerated. However, road construction machinery is projected to expand at a 10.05% CAGR through 2031.

Earthmoving remains the anchor of the Indian construction equipment market thanks to cross-sector utility in infrastructure, mining, and real estate. Meanwhile, material-handling units sales surge as logistics parks and port modernization absorbed wheel loaders, forklifts, and reach stackers. Telematics adoption is rising swiftly, turning formerly "dumb iron" into connected assets that cut idle time and fuel burn.

Diesel-hydraulic rigs controlled 94.72% of deliveries in 2025, supported by mast-ready fuel infrastructure and proven ruggedness. Yet the electric/hybrid cohort, though only 5.28% of shipments, is scaling at a 15.68% CAGR as OEMs unveil Stage V-compliant loaders, compactors, and mini excavators.

Battery density gains, modular charging containers at project sites, and tightening emission norms are tilting buyer economics in favor of zero-tailpipe machines. Early adopters in metro rail and airport builds cite lower lifetime operating costs and easier compliance for urban projects with strict noise and emission caps. The Indian construction equipment market size for electric models is projected to triple by 2031.

India Construction Equipment Market is Segmented by Equipment Type (Earthmoving Equipment, Road Construction Equipment, Material Handling Equipment, Concrete Equipment, and Material Processing and Crushing Equipment), by Drive Type (Conventional Hydraulic / Diesel, and More), by End-User Industry, by Power Output Rating, by Ownership Model, and Region. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- JCB India Ltd.

- Tata Hitachi Construction Machinery Co. Pvt. Ltd.

- Caterpillar Inc.

- Komatsu India Pvt. Ltd.

- Volvo Construction Equipment India

- Larsen & Toubro Construction & Mining Equipment

- SANY Heavy Industry India

- XCMG Construction Machinery Co. Ltd.

- Hyundai Construction Equipment India

- BEML Ltd.

- Action Construction Equipment Ltd.

- Kobelco Construction Equipment India

- CNH Industrial (CASE Construction)

- Doosan Bobcat India

- Zoomlion Heavy Industry Science & Technology

- LiuGong India

- Mahindra Construction Equipment

- Wirtgen India (John Deere)

- Schwing Stetter India

- Putzmeister India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-led Mega Infrastructure Projects Under National Infrastructure Pipeline (NIP) Stimulating Equipment Demand

- 4.2.2 Rapid Urbanization Propelling High-rise Residential Construction in Tier II & III Cities

- 4.2.3 Acceleration of Mining Sector Reforms Increasing Demand for High-Capacity Excavators

- 4.2.4 Fast-Track Execution of Bharatmala & Gati Shakti Corridor Programs Boosting Road Equipment Orders

- 4.2.5 Proliferation of Equipment Rental Platforms Expanding Access for SME Contractors

- 4.2.6 OEM Investment in Localized Manufacturing & CKD Assembly Lowering Lead Times & Costs

- 4.3 Market Restraints

- 4.3.1 Volatile Steel Prices Inflating OEM Production Costs & Customer Capex Budgets

- 4.3.2 Persistent Delays in Land Acquisition Slowing Equipment Utilization Rates on Projects

- 4.3.3 Limited Charging Infrastructure Hindering Adoption of Electric & Hybrid Machines

- 4.3.4 Regulatory Uncertainty Around Upcoming CEV Stage V Emission Norms Adding Compliance Burden

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook (Telematics, Autonomous Operation, Electrification)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Equipment Type

- 5.1.1 Earthmoving Equipment

- 5.1.1.1 Excavator

- 5.1.1.2 Backhoe Loader

- 5.1.1.3 Wheeled Loader

- 5.1.1.4 Bulldozer

- 5.1.1.5 Motor Grader

- 5.1.1.6 Compaction Roller

- 5.1.2 Road Construction Equipment

- 5.1.2.1 Asphalt Paver & Finishers

- 5.1.2.2 Cold Planers & Milling Machines

- 5.1.3 Material Handling Equipment

- 5.1.3.1 Mobile Cranes

- 5.1.3.2 Forklift & Telehandler

- 5.1.3.3 Aerial Work Platforms

- 5.1.4 Concrete Equipment

- 5.1.4.1 Transit Mixer

- 5.1.4.2 Concrete Pump

- 5.1.4.3 Batching Plant

- 5.1.5 Material Processing & Crushing Equipment

- 5.1.5.1 Jaw & Cone Crushers

- 5.1.5.2 Screening Plants

- 5.1.5.3 Pile-Driving & Drilling Rigs

- 5.1.1 Earthmoving Equipment

- 5.2 By Drive Type

- 5.2.1 Conventional Hydraulic / Diesel

- 5.2.2 Electric / Hybrid

- 5.3 By End-User Industry

- 5.3.1 Infrastructure (Roads, Rail, Airports, Ports)

- 5.3.2 Real Estate (Residential, Commercial)

- 5.3.3 Mining & Quarrying

- 5.3.4 Industrial & Energy

- 5.4 By Power Output Rating

- 5.4.1 less than 100 HP

- 5.4.2 101- 200 HP

- 5.4.3 201- 400 HP

- 5.4.4 greater than 400 HP

- 5.5 By Ownership Model

- 5.5.1 Rental Fleet

- 5.5.2 Contractor-Owned

- 5.6 By Region

- 5.6.1 North India

- 5.6.2 South India

- 5.6.3 West India

- 5.6.4 East India

- 5.6.5 Central India

- 5.6.6 North-East India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JV, Localization, Product Launches)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 JCB India Ltd.

- 6.4.2 Tata Hitachi Construction Machinery Co. Pvt. Ltd.

- 6.4.3 Caterpillar Inc.

- 6.4.4 Komatsu India Pvt. Ltd.

- 6.4.5 Volvo Construction Equipment India

- 6.4.6 Larsen & Toubro Construction & Mining Equipment

- 6.4.7 SANY Heavy Industry India

- 6.4.8 XCMG Construction Machinery Co. Ltd.

- 6.4.9 Hyundai Construction Equipment India

- 6.4.10 BEML Ltd.

- 6.4.11 Action Construction Equipment Ltd.

- 6.4.12 Kobelco Construction Equipment India

- 6.4.13 CNH Industrial (CASE Construction)

- 6.4.14 Doosan Bobcat India

- 6.4.15 Zoomlion Heavy Industry Science & Technology

- 6.4.16 LiuGong India

- 6.4.17 Mahindra Construction Equipment

- 6.4.18 Wirtgen India (John Deere)

- 6.4.19 Schwing Stetter India

- 6.4.20 Putzmeister India

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment