|

시장보고서

상품코드

2035134

필리핀의 데이터센터 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Philippines Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

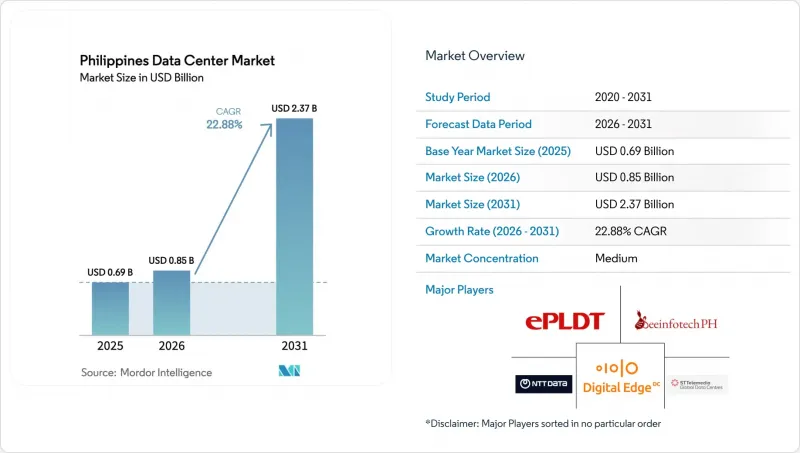

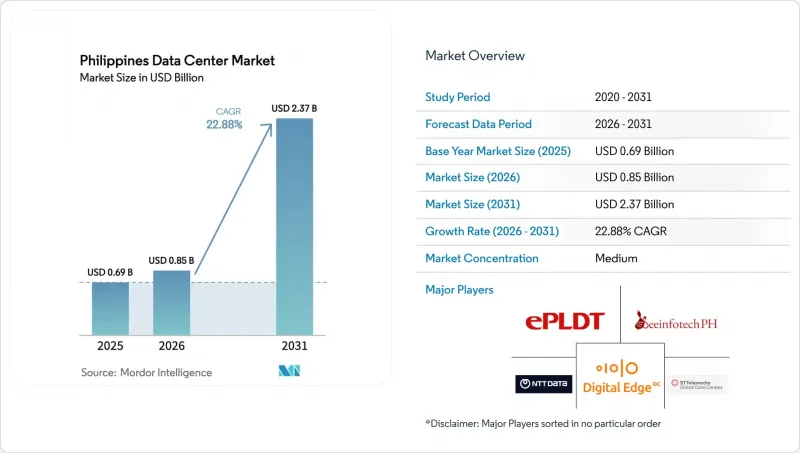

2026년 필리핀의 데이터센터 시장 규모는 8억 5,000만 달러로 추계되며 2025년 6억 9,000만 달러에서 확대되어, 2031년에는 23억 7,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 22.88%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

설치 용량 측면에서 시장은 2025년 632.80MW에서 2030년까지 852.80MW로 확대될 것으로 예상되며, 예측 기간(2025-2030년) 동안 6.15%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 시장 세분화에서의 점유율 및 예측치는 MW 단위로 계산되어 보고되고 있습니다. 하이퍼스케일 개발, 정부의 '클라우드 우선' 정책, 해저 케이블망의 확장으로 건설 일정이 단축되고 있으며, 사업자들은 우량 부지, 재생에너지, 숙련된 인력을 확보하기 위해 서두르고 있습니다. 새로운 태평양 횡단 경로를 통해 공급되는 국제 대역폭은 지연을 줄이고 중복성을 향상시켜 전 세계 공급자들을 마닐라, 클락 및 신흥 지역 허브로 끌어들이고 있습니다. 은행, 통신, 전자상거래 등 기업의 디지털 전환(DX) 프로그램을 통해 고객 기반이 꾸준히 확대되고 있으며, 지속가능성 목표 달성을 위해 액체 냉각 및 재생에너지 도입이 가속화되고 있습니다. 국내 기존 사업자들이 점유율을 지키기 위해 노력하는 가운데, 시설을 캐리어 중립적, AI 대응, 에너지 효율성이 뛰어난 시설로 포지셔닝하는 국제적인 코로케이션 전문 기업들이 진입하면서 경쟁이 치열해지고 있습니다.

필리핀의 데이터센터 시장 동향 및 인사이트

클라우드 및 OTT 구축 가속화

하이퍼스케일 클라우드 제공업체들은 워크로드 현지화를 진행하고 있으며, 알리바바 클라우드는 2025년 말까지 필리핀에 첫 번째 시설을 건설할 계획입니다. 한편, 미국에 기반을 둔 사업자들은 메트로 마닐라 및 중부 루손 지역의 입지를 평가했습니다. '국가 클라우드 우선 정책'에 따라 공공기관의 워크로드 전환이 의무화되면서 멀티테넌트 용량에 대한 안정적인 수요가 발생하고 있습니다. eGov PH 슈퍼앱과 같은 전자정부 플랫폼은 공유 인프라에 서비스를 통합하고 있으며, 이로 인해 컴퓨팅 요구사항이 증가하고 있습니다. 산업통상자원부는 2030년까지 인공지능이 GDP의 12%를 차지할 것으로 예측하고 있으며, 이는 GPU 지원 데이터센터에 대한 투자를 촉진하고 있습니다. 따라서 사업자는 미래를 내다보는 자산 구축을 위해 고밀도 랙, 액체 냉각, 전용 AI 존을 갖춘 캠퍼스를 설계하고 있습니다.

저지연 에지 노드에 대한 기업 수요 급증

금융기관, 통신사, 디지털 플랫폼 업체들은 점점 높아지는 사용자 경험 기준을 충족시키기 위해 트랜잭션 처리를 최종 사용자와 가까운 곳으로 옮기고 있습니다. 유니온뱅크는 데이터 아키텍처 현대화를 통해 대출 승인 주기를 6주에서 3분 이내로 단축하고, 근접 컴퓨팅 환경의 저지연 이점을 강조하고 있습니다. 필리핀 중앙은행(Bangko Sentral ng Pilipinas)의 보고서에 따르면, 2024년에는 소매 결제의 50%가 디지털화될 것이며, 이는 즉각적인 사기 감지 엔진에 대한 수요를 견인할 것으로 예측됩니다. 글로브 텔레콤은 18개 거점 및 퍼블릭 클라우드 지역으로 프리즈마 클라우드의 보안 제어를 확장하여 4,600만 명의 GCash 사용자를 지원하고 있습니다. 이러한 워크로드에는 마이크로초 단위의 지연 시간이 요구되기 때문에 통신사들은 주요 허브와의 상호 연결을 유지하면서 지방 도시에 위성 시설을 구축하는 추세입니다.

전기요금 폭등과 전력망 불안정성 심화

상업용 전력 평균 가격은 1kWh당 0.18달러로 동남아시아에서 가장 높아 영업이익률을 압박하고 있습니다. 현물시장의 변동성은 여전히 심각하며, 2024년 초에는 비사야 지역의 도매가격이 42% 급등하여 전력비용 예측이 더욱 어려워졌습니다. 정전은 연평균 28회 발생하며, 5시간 정전으로 인한 생산성 손실은 5억 5,600만 필리핀 페소(9억 8,000만 달러)에 달할 것으로 추정됩니다. 사업자는 재생에너지 전력 구매 계약 체결, 현장 내 디젤 발전기 설치, 유연한 전력 사용 효율을 고려한 설계를 통해 리스크를 헤지하고 있습니다. 그럼에도 불구하고 말레이시아나 태국에 비해 높은 전기요금이 하이퍼스케일 시설의 자체 건설을 억제하고 있어 잠재적 수요 증가를 둔화시키고 있습니다.

부문 분석

2025년 필리핀의 데이터센터 시장에서 대규모 시설이 46.10%를 차지했습니다. 이는 연속적인 화이트스페이스와 효율적인 운영을 원하는 하이퍼스케일 고객의 요구사항에 따른 것입니다. VITRO Sta. Rosa 캠퍼스는 4,500 랙과 50MW를 추가하여, 이 사업자의 전국 총 용량을 100MW로 확대했습니다. 한편, STT Fairview는 완공 시 124MW를 목표로 하고 있습니다. CAGR 4.42%로 성장하고 있는 중형 홀은 특히 지방 경제특구에서 지연시간과 비용의 균형을 중시하는 기업들이 선호하고 있습니다. 나라테크놀로지파크가 계획하고 있는 3단계 300MW 규모의 메가캠퍼스는 전력 공급과 수요 증가에 맞추어 개발업체가 단계적으로 자본 지출을 하는 방식을 보여줍니다.

0.5-2MW 대역의 엣지 노드는 특히 세부와 다바오에서 핀테크, 전자상거래, 미디어 워크로드에 대한 지역 규제 요건을 충족합니다. 60MW 이상의 메가 시설은 여전히 제한적이지만, 에너지 효율 기준의 벤치마크가 되고 있으며, 많은 경우 ASHRAE의 열 설계 가이드라인을 능가하는 액체 침지 냉각을 통합하고 있습니다. 이러한 양극화를 통해 사업자는 포트폴리오형 접근 방식을 제공할 수 있습니다. 즉, AI를 위한 메가 캠퍼스 내 고밀도 구역과 컨텐츠 캐시 및 재해복구 워크로드를 위해 2급 도시에 설치된 소규모 시설을 결합한 형태입니다.

2025년에는 Tier 3 환경이 71.42%의 점유율을 차지했으며, 이는 동시 유지보수가 가능한 인프라를 요구하는 기업의 서비스 수준 계약(SLA)을 반영합니다. PLDT의 클락 지점은 마닐라를 제외한 지역 최초로 TIA-942 Rated-3 인증을 획득하여 지역 개발 사업자들의 모범이 되고 있습니다. 필리핀의 데이터센터 시장에서 Tier 4에 할당된 규모는 여전히 작지만, 은행과 주요 SaaS 제공업체들이 다운타임 없이 비동기식 유지보수가 가능한 내결함성 플랫폼을 요구함에 따라 그 확대가 가속화될 것으로 보입니다.

사업자들은 듀얼 전원 경로와 이중화 및 중복성 향상에 대한 단계적 투자를 통해 Tier 4로 업그레이드할 수 있도록 설계된 'Tier 3 플러스'로 신규 시설을 계획하고 있습니다. 가동 시간보다 비용 효율성이 우선시되는 아카이브 및 재해복구 워크로드의 경우, Tier 1-2 공간이 계속 활용되고 있습니다. 필리핀 중앙은행(Bangko Sentral ng Pilipinas)의 2시간 이내 위반 보고에 대한 규제 지침은 중복 전원 및 냉각 설비에 대한 고객의 기대치를 높이고, 신규 프로젝트의 진입점으로 Tier 3를 촉진하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(메가와트)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Philippines Data Center Market size in 2026 is estimated at USD 0.85 billion, growing from 2025 value of USD 0.69 billion with 2031 projections showing USD 2.37 billion, growing at 22.88% CAGR over 2026-2031.

In terms of installed base, the market is expected to grow from 632.80 megawatt in 2025 to 852.80 megawatt by 2030, at a CAGR of 6.15% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. Hyperscale deployments, government cloud-first mandates, and a widening submarine-cable footprint are compressing build timelines, while operators race to secure prime land, renewable power, and skilled talent. International bandwidth supplied by new trans-Pacific routes is reducing latency and improving redundancy, attracting global providers toward Manila, Clark, and emerging provincial hubs. Enterprise digital transformation programs in banking, telecom, and e-commerce are steadily expanding the customer base, and sustainability targets are accelerating the adoption of liquid cooling and renewable energy procurement. Competitive intensity is rising as domestic incumbents defend their share against international colocation specialists, who are positioning facilities as carrier-neutral, AI-ready, and energy-efficient.

Philippines Data Center Market Trends and Insights

Accelerating cloud and OTT build-outs

Hyperscale cloud providers are localizing workloads, with Alibaba Cloud planning to build its first Philippine facility by the end of 2025, while United States-based operators are evaluating sites around Metro Manila and Central Luzon. The National Cloud First Policy obliges public agencies to migrate workloads, thereby creating a steady demand for multi-tenant capacity. E-government platforms such as the eGov PH Super App consolidate services on shared infrastructure, amplifying compute requirements. The Department of Trade and Industry projects that artificial intelligence could contribute 12% to GDP by 2030, catalyzing investment in GPU-ready data centers. Operators are therefore designing campuses with high-density racks, liquid cooling, and dedicated AI zones to future-proof assets.

Surging enterprise demand for low-latency edge nodes

Financial institutions, telecom operators, and digital platforms are shifting transaction processing closer to end users to meet rising user-experience standards. Union Bank reduced loan approval cycles from six weeks to under three minutes after modernizing its data architecture, underscoring the latency advantage of proximate compute. The Bangko Sentral ng Pilipinas reports that 50% of retail payments were digital in 2024, driving demand for instant fraud-detection engines. Globe Telecom supports 46 million GCash users by extending Prisma Cloud security controls across 18 sites and public cloud regions. Such workloads require microsecond latency, prompting operators to develop satellite facilities in secondary cities while maintaining interconnections to core hubs.

Rising electricity tariffs and grid instability

The average commercial electricity price stands at USD 0.18 per kWh, the highest in Southeast Asia, eroding operating margins. Spot-market volatility remains acute; Visayas wholesale rates jumped 42% in early 2024, escalating power-cost forecasting challenges. Outages occur on average 28 times annually, and a five-hour interruption costs an estimated PHP 556 million (USD 9.8 million) in lost productivity. Operators hedge exposure by signing renewable power purchase agreements, installing on-site diesel backup, and designing for flexible power usage effectiveness. Nevertheless, elevated tariffs restrain hyperscale self-builds when compared with Malaysia or Thailand, slowing potential demand.

Other drivers and restraints analyzed in the detailed report include:

- Government incentives for hyperscale investment

- Strengthening submarine-cable landing ecosystem

- Complex right-of-way and permitting procedures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large facilities accounted for 46.10% of the Philippines' data center market in 2025, driven by hyperscale customer requirements for contiguous white space and streamlined operations. The VITRO Sta. Rosa campus adds 4,500 racks and 50 MW, bringing the operator's nationwide capacity to 100 MW, while STT Fairview targets 124 MW upon completion. Medium-sized halls, growing at a 4.42% CAGR, appeal to enterprises that balance latency and cost, especially in provincial economic zones. The Narra Technology Park's planned three-phase 300-MW megacampus illustrates how developers stagger capital outlays to align with power and demand ramp-ups.

Edge nodes in the 0.5-2 MW band meet locality compliance for fintech, e-commerce, and media workloads, particularly in Cebu and Davao. Mega facilities above 60 MW remain limited but set the benchmark for energy-efficiency standards, often exceeding ASHRAE thermal guidelines and integrating liquid immersion cooling. This bifurcation enables operators to offer a portfolio approach: high-density zones in mega campuses for AI, complemented by smaller footprints in Tier 2 cities for content caching and disaster-recovery workloads.

Tier 3 environments dominated 71.42% share in 2025, reflecting enterprise service-level agreements that require concurrently maintainable infrastructure. PLDT's Clark site received the first TIA-942 Rated-3 certification outside Manila, setting a template for regional developers. The Philippines' data center market size allocated to Tier 4 remains small, but it could accelerate as banks and critical SaaS providers demand fault-tolerant platforms capable of asynchronous maintenance without downtime.

Operators design new builds as Tier 3-plus, engineered to upgrade to Tier 4 through incremental investments in dual power paths and higher redundancy. Tier 1-2 space persists for archival and disaster-recovery workloads where cost efficiency outweighs uptime. Regulatory guidance from the Bangko Sentral ng Pilipinas regarding two-hour breach reporting reinforces customer expectations for redundant power and cooling, pushing Tier 3 as the entry point for new projects.

The Philippines Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-built, Enterprise/Edge, and Colocation [Non-Utilized, and Utilized {Retail Colocation, Wholesale Colocation}]), End User (BFSI, IT and ITES, and More), and Hotspot. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- Bee Information Technology Philippines Inc

- ePLDT Inc

- NTT Global Data Centers Philippines Inc

- ST Telemedia Global Data Centres Philippines

- Digital Edge (Singapore) Holdings Pte Ltd

- FLOW Digital Infrastructure and AyalaLand Logistics Holdings Corp Joint Venture

- Alibaba Cloud

- DITO Telecommunity

- Converge ICT Solutions Inc

- YCO Global Cloud Centers Holdings Inc

- GTI Telecom

- VST ECS Phils Inc

- Bitstop Network Services

- Equinix Inc

- Globe Telecom Inc

- Amazon Web Services Inc

- Google Cloud Philippines

- Microsoft Philippines Inc

- Princeton Digital Group

- Space DC Pte Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating cloud and OTT build-outs

- 4.2.2 Surging enterprise demand for low-latency edge nodes

- 4.2.3 Government incentives for hyperscale investment

- 4.2.4 Strengthening submarine-cable landing ecosystem

- 4.2.5 Rapid fiberization outside Metro Manila

- 4.2.6 Green-energy policy boosting PUE optimization

- 4.3 Market Restraints

- 4.3.1 Rising electricity tariffs and grid instability

- 4.3.2 Complex right-of-way and permitting procedures

- 4.3.3 Skilled-labor shortages in critical facility ops

- 4.3.4 Elevated sovereign-risk premium for USD financing

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MEGAWATT)

- 5.1 By Data Center Size

- 5.1.1 Large

- 5.1.2 Massive

- 5.1.3 Medium

- 5.1.4 Mega

- 5.1.5 Small

- 5.2 By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale/Self-built

- 5.3.2 Enterprise/Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End User

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Hotspot

- 5.5.1 Angeles City

- 5.5.2 Metro Manila

- 5.5.3 Bamban

- 5.5.4 Rest of Philippines

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bee Information Technology Philippines Inc

- 6.4.2 ePLDT Inc

- 6.4.3 NTT Global Data Centers Philippines Inc

- 6.4.4 ST Telemedia Global Data Centres Philippines

- 6.4.5 Digital Edge (Singapore) Holdings Pte Ltd

- 6.4.6 FLOW Digital Infrastructure and AyalaLand Logistics Holdings Corp Joint Venture

- 6.4.7 Alibaba Cloud

- 6.4.8 DITO Telecommunity

- 6.4.9 Converge ICT Solutions Inc

- 6.4.10 YCO Global Cloud Centers Holdings Inc

- 6.4.11 GTI Telecom

- 6.4.12 VST ECS Phils Inc

- 6.4.13 Bitstop Network Services

- 6.4.14 Equinix Inc

- 6.4.15 Globe Telecom Inc

- 6.4.16 Amazon Web Services Inc

- 6.4.17 Google Cloud Philippines

- 6.4.18 Microsoft Philippines Inc

- 6.4.19 Princeton Digital Group

- 6.4.20 Space DC Pte Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment