|

시장보고서

상품코드

2035142

인도의 이륜차 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Two Wheeler - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

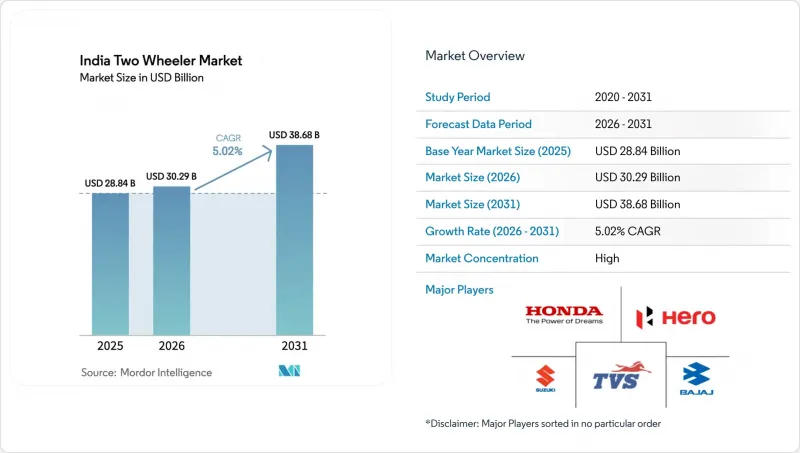

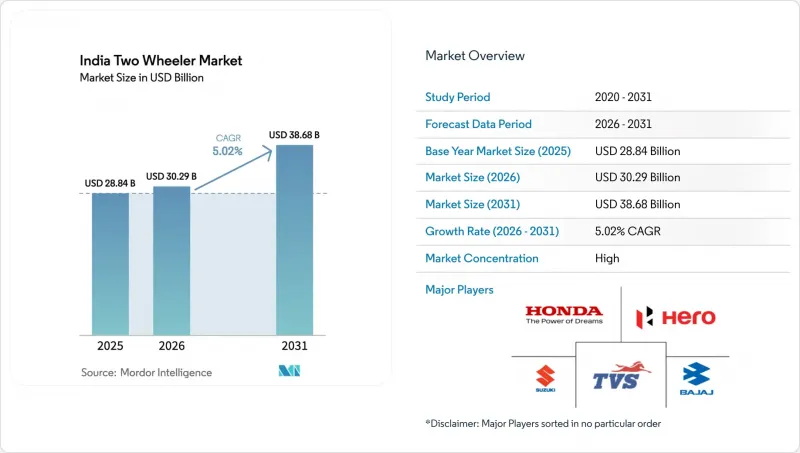

인도의 이륜차 시장 규모는 2025년에 288억 4,000만 달러로 평가되었고 2026년 302억 9,000만 달러에서 2031년까지 386억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.02%를 나타낼 전망입니다.

이러한 성장 궤도를 뒷받침하는 것은 전동화에 대한 강력한 정책적 지원, 수출 수요 회복, 그리고 디지털 소매 채널의 확대입니다. 혼잡한 도심에서의 이동성 높은 이동수단에 대한 수요, 팬데믹 이후 가처분 소득의 회복, 그리고 물류용 차량 증가가 판매량 증가를 견인하고 있습니다. 배터리 교체 경제성이 전기차 보급을 촉진하는 한편, 내연기관(ICE) 차량 수출에 따른 규모의 경제 효과로 제조업체는 수익률 저하 없이 전동화에 투자할 수 있습니다. 기존 브랜드와 전기차 전문 업체 간의 경쟁 심화는 모델 교체 주기 단축, 커넥티비티 기능 추가, 공격적인 가격 전략 등을 촉진하고 있으며, 이로 인해 인도의 이륜차 시장은 일반 소비자부터 프리미엄 소비자에 이르기까지 다양한 구매자들에게 매력적인 시장으로 자리매김하고 있습니다.

인도의 이륜차 시장 동향과 인사이트

FAME-II 보조금 연장 및 주정부의 EV 인센티브 제공

정부의 인센티브가 전기 이륜차의 급속한 보급을 촉진하고 있습니다. 국가 차원의 노력은 구매 보조금 제공과 인프라 투자를 통해 지속적인 수요를 보장하고 종합적인 충전 및 배터리 교체 네트워크를 구축하고 있습니다. 주정부 차원에서는 현금 인센티브와 자본 보조금을 통해 구매 부담을 경감시키고 있습니다. 또한, 전기차 전용 공원 설립은 장기적인 노력을 강조하는 것입니다. 이러한 일관된 전략은 OEM의 비즈니스 사례를 강화하고, 시장에서 전동화로의 전환을 위한 토대를 마련하고 있습니다.

도심의 교통체증으로 오토바이 선호도 높아져

델리와 뭄바이의 러시아워 평균 속도는 시속 20km 미만이지만, 이륜차는 자동차에 비해 시내 이동을 40% 더 빨리 완료할 수 있고, 주차 공간도 85% 덜 차지합니다. 혁신적인 도시 프로젝트는 현재 이륜차 전용 차선과 안전한 주차 공간을 확보하여 교통 체증 완화에 있어 이륜차의 역할을 제도화하고 있습니다. 배달 차량 또한 스쿠터와 소형 오토바이를 이용한 30분 이내 배송을 약속함으로써 이러한 이점을 뒷받침하고 있으며, 인도 도시 지역에서 이륜차가 실용적인 이동수단이라는 소비자의 인식을 강화시키고 있습니다.

배터리 원재료 가격 변동

국내 배터리 제조업체들은 리튬 가격의 극심한 변동과 수입 리튬-코발트에 대한 과도한 의존으로 인해 환리스크와 공급차질에 직면해 있습니다. 이러한 압력은 이윤율을 압박하고, 결국 OEM의 가격 책정에 영향을 미칩니다. 그 결과, 전기차와 내연기관차의 비용 격차가 때때로 확대되어 보조금 지원에도 불구하고 구매 결정이 정체되는 상황이 발생하고 있습니다.

부문 분석

2025년, 오토바이는 도시와 농촌 도로 모두에서 활용도가 높아 인도 오토바이 시장 점유율 74.05%를 유지했습니다. 하지만, 스톱 앤 고 교통 상황에 적합한 자동 변속기와 여성 라이더 증가에 힘입어 스쿠터는 2031년까지 연평균 복합 성장률(CAGR) 6.05%로 더 빠른 속도로 성장하고 있습니다. 상업용 배송업체들은 평평한 바닥판과 시트 아래 수납공간을 높이 평가하고 있으며, 기업 수요가 증가함에 따라 스쿠터에 대한 수요는 더욱 확대되고 있습니다. 또한, 필요한 출력이 낮기 때문에 소형 배터리 팩이 필요한 전기 기술은 스쿠터에 적합하며, 저렴한 가격과 가벼운 차량 중량을 실현하고 있습니다. 이에 따라 기존 브랜드들은 전기 스쿠터 라인업을 출시하는 한편, 지방 시장 점유율을 지키기 위해 100-125cc급 오토바이의 모델 체인지에 주력하고 있습니다.

스쿠터의 위험성은 고속 주행 시 안정성이 제한적이라는 점인데, 이는 고속도로 이용자나 장거리 이동이 많은 지방 통근자들에게는 매력적으로 다가갈 수 없는 부분입니다. 노면 상황이 복잡한 교외 지역에서는 높은 최저지상고와 견고한 서스펜션이 요구되기 때문에 오토바이가 주류를 이루고 있습니다. 투어링과 어드벤처와 같은 하위 부문이 오토바이 판매량을 견인하고 있으며, 이는 부유한 젊은 층 사이에서 취미와 레저로 라이딩이 인기를 끌고 있기 때문입니다. 전반적으로 인도의 이륜차 시장은 스쿠터와 오토바이의 기존 세력이 균형을 이루고 있으며, 지역에 관계없이 두 형태가 공존할 수 있는 여지가 남아 있습니다.

2025년 기준, 내연기관 플랫폼은 인도 오토바이 시장 규모의 88.15%를 차지했으며, 이는 주유소 정착과 낮은 구매비용을 반영합니다. 보조금에 의한 가격 혜택, BaaS(Battery-as-a-Service), 그리고 저렴한 재생에너지에 의한 전력 공급은 전기차 판매량을 증가시켜 2031년까지 연평균 복합 성장률(CAGR) 7.02%의 견조한 성장세를 보이고 있습니다. 하루 80-100km를 주행하는 차량 사업자는 18-24개월 이내에 손익분기점에 도달하기 때문에 전동화로의 전환이 가속화되고 있습니다. 각 OEM사의 제품 라인업은 현재 두 가지 파워트레인을 모두 아우르고 있습니다. Hero MotoCorp와 TVS Motor는 48V 아키텍처 스쿠터에 투자하는 한편, 엄격해지는 배기가스 규제에 대응하기 위해 BS-VI 엔진을 개선하고 있습니다. 이러한 전략적 헤징을 통해 기술 격차를 넘어 존재감을 유지하고, 인도의 이륜차 시장이 점차 전동화되는 가운데 수익성을 보호하고 있습니다.

과제는 여전히 남아있습니다. 배터리 폐기 관련 규제, 3급 지역의 전력망 용량, 그리고 실제 주행거리에 대한 소비자의 인식 등을 꼽을 수 있습니다. 내연기관(ICE)은 거의 즉각적으로 연료를 보충할 수 있다는 장점을 계속 누리고 있습니다. 그러나 배터리 팩의 가격은 매년 20%씩 하락하고 있으며, 인도의 PLI-ACC 제도에 따른 국내 셀 제조로 인해 비용 격차는 더욱 줄어들 것으로 예측됩니다. 장기적으로는 경제성 수렴과 인프라 개선으로 2028년경 전환점이 도래하여 도시지역에서의 판매가 전기차로 크게 기울어질 것으로 예측됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 주요 업계 동향

제5장 시장 구도

제6장 시장 규모와 성장 예측(금액(달러) 및 수량(대수))

제7장 경쟁 구도

제8장 시장 기회와 향후 전망

제9장 CEO을 위한 중요 전략적 과제

JHS 26.05.20The India two-wheeler market size was valued at USD 28.84 billion in 2025 and estimated to grow from USD 30.29 billion in 2026 to reach USD 38.68 billion by 2031, at a CAGR of 5.02% during the forecast period (2026-2031).

Strong policy backing for electrification, export demand recovery, and widening digital retail channels underpin this trajectory. Preference for agile transport in congested cities, the return of disposable incomes after the pandemic, and growing logistics fleets reinforce volume growth. Electric vehicle uptake is amplified by battery swapping economics, while scale benefits from ICE exports allow manufacturers to fund electrification without eroding margins. Intensifying competition among legacy brands and EV specialists encourages faster model refresh cycles, added connectivity features, and aggressive pricing strategies that keep the India two-wheeler market attractive for both mass and premium buyers.

India Two Wheeler Market Trends and Insights

FAME-II Subsidy Extension and State EV Incentives

Government incentives are driving the swift adoption of electric two-wheelers. National initiatives offer purchase subsidies and invest in infrastructure, guaranteeing sustained demand and establishing a comprehensive charging and swapping network. On the state level, programs boost affordability with cash incentives and capital subsidies. Additionally, the establishment of dedicated EV parks underscores a long-term commitment. This cohesive strategy bolsters OEM business cases and sets the stage for a significant move towards electrification in the market.

Urban Congestion Driving 2W Preference

Peak-hour speeds in Delhi and Mumbai fall below 20 km/h, yet a two-wheeler completes typical cross-town trips 40% quicker than a car while occupying 85% less parking space. Innovative city projects now earmark dedicated lanes and secure parking for two-wheelers, institutionalizing their role in reducing traffic congestion. Delivery fleets further validate the advantage by meeting 30-minute delivery promises via scooters and small motorcycles, reinforcing consumer perception that two-wheelers are the pragmatic mobility choice in urban India.

Battery-Raw-Material Price Volatility

Domestic battery manufacturers face currency risks and supply disruptions due to extreme swings in lithium prices and a heavy reliance on imported lithium and cobalt. These pressures compress profit margins, which in turn influence OEM pricing. As a result, the cost gap between electric vehicles and internal combustion vehicles occasionally widens, stalling purchase decisions even with subsidy support .

Other drivers and restraints analyzed in the detailed report include:

- Swappable-battery Business Models Lowering TCO

- Digital Lending Expanding Credit to Informal Riders

- Sparse Charging and Swapping Infrastructure Outside Metros

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Motorcycles sustained 74.05% of the India two-wheeler market share in 2025, owing to their versatility across city and rural roads. Yet scooters are growing faster at a 6.05% CAGR through 2031, aided by automatic transmissions that suit stop-start traffic and rising female ridership. Commercial delivery firms value the flat floorboard and under-seat storage, adding corporate volumes that further widen scooter demand. Electric technology also fits scooters well because lower power needs align with smaller battery packs, ensuring reasonable prices and curb weights. In response, legacy brands unveil electric scooter lines while doubling down on 100-125 cc motorcycle refreshes to defend share in hinterland districts.

Risks for scooters lie in limited high-speed stability, which restricts appeal for highway users and rural commuters travelling longer distances. Motorcycles dominate semi-urban zones where mixed road surfaces require higher ground clearance and robust suspension. Tourer and adventure sub-segments anchor motorcycle volumes, as hobby and leisure riding are popular among affluent youth segments. Overall, the India two-wheeler market thus balances scooter momentum with motorcycle incumbency, leaving room for both formats to co-exist across geographies.

Internal combustion engine platforms accounted for 88.15% of the India two-wheeler market size in 2025, reflecting entrenched fuel stations and lower purchase costs. Subsidized pricing, battery-as-a-service, and cheaper renewables electricity push electric volumes forward, delivering a robust 7.02% CAGR to 2031. Fleet operators with 80-100 km daily realize break-even within 18-24 months, accelerating conversions. OEM portfolios now straddle both powertrains; Hero MotoCorp and TVS Motor invest in 48 V architecture scooters while upgrading BS-VI engines to meet tightening emission rules. Strategic hedging ensures relevance across the technology divide and shields revenues as the India two-wheeler market gradually electrifies.

Challenges remain: battery disposal norms, grid capacity in tier-III regions, and consumer awareness of real-world range. ICE continues to enjoy near-instant refueling advantages. However, pack prices fall at a 20% annual clip, and domestic cell manufacturing under India's PLI-ACC scheme will narrow cost gaps further. Long-term, converging economics and improved infrastructure suggest a tipping point around 2028 when urban sales tilt materially toward electric.

The India Two-Wheeler Market Report is Segmented by Vehicle Type (Motorcycles and Scooters), Propulsion (ICE and Electric), Engine Capacity/Motor Power (Up To 110cc, and More), Price Band (Up To USD 1, 000, and More), End User (B2C and B2B), Sales Channel (Online and Offline), and by State. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Hero MotoCorp Ltd.

- Honda Motorcycle and Scooter India Pvt. Ltd.

- TVS Motor Company Ltd.

- Bajaj Auto Ltd.

- Suzuki Motorcycle India Pvt. Ltd.

- Royal Enfield

- Yamaha Motor India Pvt. Ltd.

- Piaggio Vehicles Pvt. Ltd.

- Mahindra Two Wheelers Ltd.

- India Kawasaki Motors Pvt. Ltd.

- Ampere Vehicles Pvt. Ltd.

- Ather Energy Pvt. Ltd.

- Okinawa Autotech Pvt. Ltd.

- Ola Electric Mobility Pvt. Ltd.

- Revolt Intellicorp Pvt. Ltd.

- Kinetic Green Energy and Power Solutions Ltd.

- Simple Energy Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Key Industry Trends

- 4.1 Population and Urbanization Rate

- 4.2 GDP per Capita (PPP) and Median Disposable Income

- 4.3 Consumer Spend on Vehicle Purchase/Transport (CVP)

- 4.4 Fuel Prices

- 4.5 Interest Rate for 2W/Auto Loans and Credit Access

- 4.6 2W Penetration (units per 1,000) and Parc

- 4.7 Dealer/Service Network Density

- 4.8 Two-Wheeler Trade and Revenue (Imports/Exports)

- 4.9 Electrification Readiness (Infra and Power)

- 4.10 Battery Pack Price and Chemistry Mix

- 4.11 Battery Swapping Stations (Network Density and Utilization)

- 4.12 New Model Pipeline and OEM Coverage

- 4.13 Value-Chain Localization and Assembly Capacity

- 4.14 Regulatory Framework

- 4.14.1 Vehicle Standards, Safety and Roadworthiness

- 4.14.2 CBU/CKD/SKD Duties and VAT; Local-content Rules; Assembly Incentives

- 4.14.3 Electrification, Energy and Environmental Policy

- 4.14.4 Bike-Taxi, Delivery-Fleet, Platform and Financing Rules

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 FAME-II Subsidy Extension and State-EV Incentives

- 5.2.2 Urban Congestion Driving 2W Preference

- 5.2.3 Swappable-Battery Business Models Lowering TCO

- 5.2.4 Tier-II/III E-Commerce Boom Boosting Last-Mile Demand

- 5.2.5 Digital Lending Expanding Credit to Informal Riders

- 5.2.6 ICE Export Demand Sustaining Domestic Scale

- 5.3 Market Restraints

- 5.3.1 Battery-Raw-Material Price Volatility

- 5.3.2 Sparse Charging/Swapping Infra Outside Metros

- 5.3.3 Policy Uncertainty on GST and Import Duties

- 5.3.4 Rising Insurance Premiums for Road-Safety Compliance

- 5.4 Value / Supply-Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Suppliers

- 5.7.3 Bargaining Power of Buyers

- 5.7.4 Threat of Substitutes

- 5.7.5 Competitive Rivalry

6 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 6.1 By Vehicle Type

- 6.1.1 Motorcycles

- 6.1.2 Scooters

- 6.2 By Propulsion

- 6.2.1 Internal Combustion Engine

- 6.2.2 Electric

- 6.3 By Engine Capacity / Motor Power

- 6.3.1 Internal Combustion Engine

- 6.3.1.1 Up to110 cc

- 6.3.1.2 111-125 cc

- 6.3.1.3 126-150 cc

- 6.3.1.4 151-200 cc

- 6.3.1.5 201-250 cc

- 6.3.1.6 250-350 cc

- 6.3.1.7 350-500 cc

- 6.3.1.8 Above 500 cc

- 6.3.2 Electric

- 6.3.2.1 Up to 1.0 kW

- 6.3.2.2 1.1-3.0 kW

- 6.3.2.3 3.1-5.0 kW

- 6.3.2.4 Above 5.0 kW

- 6.3.1 Internal Combustion Engine

- 6.4 By Price Band

- 6.4.1 Up to USD 1,000

- 6.4.2 USD 1,000-1,500

- 6.4.3 USD 1,501-2,000

- 6.4.4 USD 2,001-3,000

- 6.4.5 USD 3,001-5,000

- 6.4.6 Above USD 5,000

- 6.5 By End User

- 6.5.1 B2C

- 6.5.2 B2B

- 6.5.2.1 Ride-hail / Bike-Taxi / Rental / Tourism

- 6.5.2.2 Delivery and Logistics

- 6.5.2.3 Corporate and SME Fleets

- 6.5.2.4 Others (Govt, Institutional, NGO)

- 6.6 Sales Channel

- 6.6.1 Online

- 6.6.2 Offline

- 6.7 By State

- 6.7.1 Uttar Pradesh

- 6.7.2 Maharashtra

- 6.7.3 Tamil Nadu

- 6.7.4 Karnataka

- 6.7.5 Gujarat

- 6.7.6 Rajasthan

- 6.7.7 Andhra Pradesh

- 6.7.8 Bihar

- 6.7.9 West Bengal

- 6.7.10 Telangana

- 6.7.11 Kerala

- 6.7.12 Madhya Pradesh

- 6.7.13 Haryana

- 6.7.14 Punjab

- 6.7.15 Delhi

- 6.7.16 Rest of India

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Landscape

- 7.5 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 7.5.1 Hero MotoCorp Ltd.

- 7.5.2 Honda Motorcycle and Scooter India Pvt. Ltd.

- 7.5.3 TVS Motor Company Ltd.

- 7.5.4 Bajaj Auto Ltd.

- 7.5.5 Suzuki Motorcycle India Pvt. Ltd.

- 7.5.6 Royal Enfield

- 7.5.7 Yamaha Motor India Pvt. Ltd.

- 7.5.8 Piaggio Vehicles Pvt. Ltd.

- 7.5.9 Mahindra Two Wheelers Ltd.

- 7.5.10 India Kawasaki Motors Pvt. Ltd.

- 7.5.11 Ampere Vehicles Pvt. Ltd.

- 7.5.12 Ather Energy Pvt. Ltd.

- 7.5.13 Okinawa Autotech Pvt. Ltd.

- 7.5.14 Ola Electric Mobility Pvt. Ltd.

- 7.5.15 Revolt Intellicorp Pvt. Ltd.

- 7.5.16 Kinetic Green Energy and Power Solutions Ltd.

- 7.5.17 Simple Energy Pvt. Ltd.