|

시장보고서

상품코드

2035143

인도의 원료의약품(API) 시장 : 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)India Active Pharmaceutical Ingredients (API) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

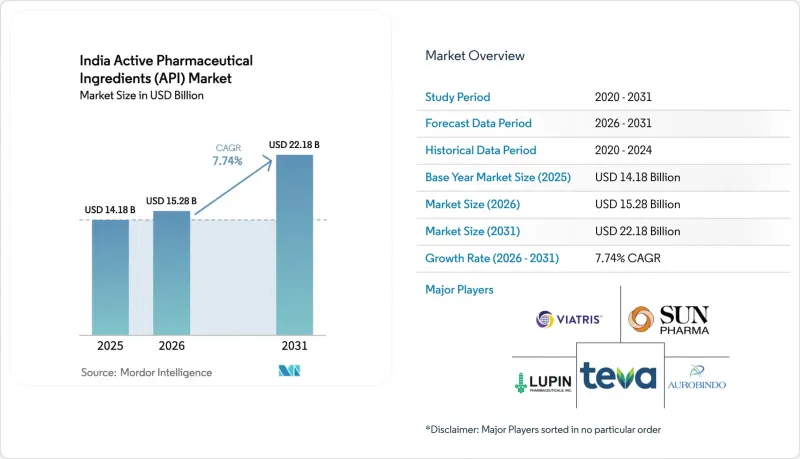

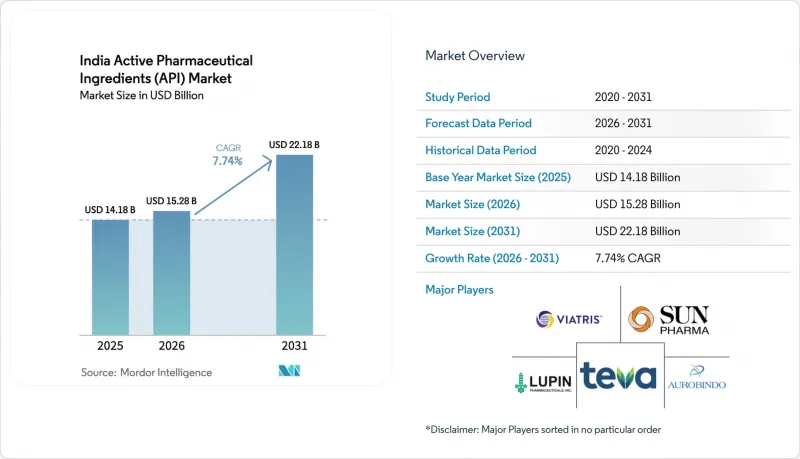

인도의 원료의약품(API) 시장 규모는 2025년 141억 8,000만 달러에서 2026년에는 152억 8,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 7.74%로 성장을 지속하여, 2031년까지 221억 8,000만 달러에 이를 것으로 예측됩니다.

확고한 정책적 인센티브, 가속화되는 수출 수요, 그리고 빠른 생산능력 확대가 결합되어 이러한 성장 궤도를 뒷받침하고 있습니다. "생산연계형 인센티브(PLI) 제도는 그린필드 공장 및 원료의약품 단지에 대한 장기 투자 자금을 공급하여 물류비용을 절감하고 생산자의 유틸리티(공공 인프라)에 대한 접근성을 개선하고 있습니다. 동시에 미국 및 유럽 바이어들은 '바이오 보안법'의 통과에 따라 중국으로부터 조달처를 옮기고 있으며, 그 결과 2024년에는 인도의 주요 위탁 생산업체들의 견적 요청량이 50% 급증했습니다. 국내 기업들도 고부가가치 종양학 및 바이오테크 분야 수주를 위해 발효, 봉쇄, 연속 제조 설비의 업그레이드를 진행하고 있으며, AI를 활용한 공정 제어를 통해 사이클 타임과 에너지 소비를 절감하고 있습니다. 한편, 중국산 주요 원료(KSM)의 가격 변동과 중소영세기업(MSME) 시설의 컴플라이언스 이슈와 같은 역풍도 존재하지만, 이러한 요인들은 모두 장기적인 경쟁력 강화를 위한 수직적 통합과 품질 시스템 개선에 힘을 실어주고 있습니다.

인도의 원료의약품(API) 시장 동향 및 인사이트

정부의 PLI와 벌크 드럭파크의 자급자족을 위한 노력

총 402억 4,000만 루피에 달하는 32개의 PLI 프로젝트가 가동 중이며, 당초 승인된 투자금액을 초과 달성하고 페니실린G 등 중요 분자의 국내 합성을 30년 만에 실현하고 있습니다. 구자라트, 히말차르 프라데시, 안드라 프라데시 주에 위치한 벌크 드럭 파크는 용제 회수 시설, 폐수 처리 시설 및 공용 유틸리티를 제공하여 운영 비용을 절감하고 있습니다. 아우로빈드 파마의 연간 15,000톤 규모의 신규 페니실린 G 생산 블록은 자급자족으로의 전환을 상징하는 사례입니다. 신규 건설 중인 자산이 정격 가동률에 도달하면 중요 중간체 수입 의존도가 절반으로 줄어들 것으로 예상되며, 상공부는 2021년 이후 민간 제약 투자 누계액을 1610억 루피로 추산하고 있습니다. 환경 인허가 신속화 및 원스톱 승인으로 프로젝트 착수 기간이 단축되어 정책의 효과가 더욱 강화되고 있습니다.

바이오보안법 통과 후 미국-EU의 주문이 인도로 빠르게 이동하고 있습니다.

2024년 미국 바이오보안법(US Biosecure Act of 2024)은 중국 생명공학 기업과 연관된 기업으로부터의 연방정부 조달을 제한하고 있으며, 원료의약품 제조업체는 공급망을 다각화할 수밖에 없습니다. 이미 750개 이상의 미국 FDA 승인 시설을 운영하고 있는 인도 생산업체들은 2024년 3분기 이후 견적요청서(RFQ)와 감사 요청이 50%나 급증했습니다. kg당 비용면에서 인도가 우위를 점하고 있으며, 동등한 품질 등급에서 인도의 도착 가격은 중국의 평균 가격보다 약 20% 낮습니다. 규제상 기술이전 주기는 여전히 18-24개월이 소요되지만, 인도의 신청 서류 작성 실적에 따라 신규 진출기업에 비해 일정을 단축할 수 있습니다. 유럽과 미국의 스폰서 기업들이 중국 공급업체로부터 잇따라 철수하는 가운데, 인도 CDMO 기업들은 계속적인 계약으로 다년간의 수익을 기대할 수 있게 되었습니다.

현지화 진행 중에도 불안정한 중국산 KSM의 비용 문제

국내 생산능력 증가에도 불구하고 인도는 2024년도에 3,770억 루피 상당의 API를 수입했으며, 이는 전체 수요의 약 35%를 차지했습니다. 2025년 초 발효용 원료 가격이 15-20% 급등하면서 애널리스트들이 12-14%까지 상승할 것으로 예상했던 영업이익률이 압박을 받았습니다. 대기업은 다지역 계약이나 자체 생산 중간체 블록을 통해 리스크 헤지를 하고 있지만, 규모가 작은 MSME(중소영세기업)는 생산을 중단하거나 생산능력 증설을 미루고 있어 공급망에 혼란을 초래하고 있습니다. PLI파크의 전면 가동 지연으로 2026년까지 의존 상태가 지속되어 투입비용 변동이 지속될 것으로 보입니다.

부문 분석

현재 일반 공급업체의 생산량 점유율은 39% 미만이지만, 개발업체들이 변동비 모델을 선호하고 기존 합성 블록을 매각함에 따라 CAGR 9.42%를 나타낼 것으로 예측됩니다. CDMO가 규제 관련 서류의 유지 관리, 밸리데이션 배치, 정기적인 현장 감사를 맡음으로써 인도 API 시장은 혜택을 받고, 스폰서 기업은 바이오 의약품 및 디지털 치료제 출시에 필요한 자금을 확보할 수 있게 됩니다. 혁신 기업들은 초기 단계의 화학, 독성학 및 임상 1상 시험용 공급을 단일 벤더 계약으로 통합하는 경향이 증가하고 있으며, 이는 엔드투엔드 역량을 갖춘 대규모 CDMO에 유리하게 작용하고 있습니다. 스타틴, 메트포르민 등 대량 생산품의 경우 단일 공장에 의한 경제성이 거래상의 간접비를 상회하기 때문에 자체 생산이 여전히 유효합니다. 하지만 환경 규제 강화와 공공요금 인플레이션으로 인해 총소유비용은 외주업체가 더 유리해지고 있습니다. 피라말 파마 솔루션즈가 켄튀르키예 주에 건설한 8,000만 달러 규모의 무균 주사제 제조 시설 확장은 세계 수요에 대응할 수 있는 아웃소싱 플랫폼의 확장성을 여실히 보여줍니다.

부차적인 장점으로는 유연한 기술이전 시기를 들 수 있습니다. 이를 통해 스폰서들은 지역별로 출시 시기를 분산시킬 수 있으며, 그 결과 외부 생산 기지의 가동률을 평준화할 수 있습니다. 인도 API 시장에서도 주요 CDMO 간의 수직적 통합이 더욱 심화되고 있습니다. 현재 반응기 공원에는 용제 회수 설비와 폐수 소각 시설이 함께 설치되어 환경-위생-안전(EH&S) 감사의 효율성을 높이고 있습니다. 반면, 자체 공장에서는 제품 구성의 복잡성으로 인한 잠재적 오염 위험에 직면하여 품질 관리 인력의 증원과 배치당 비용 증가가 불가피한 상황입니다.

합성화학은 자본집약도가 낮고 규제의 선례가 확립되어 있기 때문에 2025년에도 매출의 72.80%를 차지했습니다. 그러나 생명공학 API는 CAGR 9.18%로 성장을 지속하고, 있으며, 단클론 항체, 재조합 호르몬, mRNA 벡터가 후기 임상시험 단계에 도달함에 따라 부가가치를 창출할 것입니다. 연속 제조 스키드 및 고처리량 결정화 장치로 합성 배치 주기를 단축하는 한편, 발효 반응기에서는 실시간 대사물 센서를 채용하여 생산량(타이터)을 향상시키고 있습니다. Laurus Bio가 추가로 건설하는 120억 루피 규모의 발효 블록은 바이오 의약품 파이프라인에서 수요가 많은 아미노산 및 효소 중간체를 대상으로 합니다.

바이오텍 API의 규제적 복잡성은 여전히 높으며, 검증된 바이러스 제거 과정과 고도의 특성화 플랫폼이 필요합니다. 그러나 합성 활성물질 대비 3-5배의 가격 프리미엄이 있어 추가 설비투자는 상쇄됩니다. 인도 API 시장에서는 하이브리드 업체들이 기존 소분자 라인을 활용하여 바이오텍 사업 확장에 따른 변동성 리스크를 완화하는 등 리스크 분산이 진행되고 있습니다. 한편, 합성업체들은 원가경쟁력을 유지하기 위해 친환경 촉매와 마이크로 리액터 기술을 도입하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The India API market size is expected to grow from USD 14.18 billion in 2025 to USD 15.28 billion in 2026 and is forecast to reach USD 22.18 billion by 2031 at 7.74% CAGR over 2026-2031.

Solid policy incentives, accelerating export demand and rapid capacity additions collectively underpin this growth trajectory. The Production Linked Incentive (PLI) scheme is releasing patient capital for green-field plants and bulk-drug parks, compressing logistics costs and improving utility access for producers. At the same time, U.S. and European buyers are moving sourcing away from China after passage of the Biosecure Act, resulting in a 50% jump in request-for-quotation volumes at leading Indian contract manufacturers during 2024. Domestic firms are also upgrading fermentation, containment and continuous-manufacturing assets to capture premium Oncology and Biotech volumes, while AI-enabled process control is shaving cycle time and energy consumption. Counter-pressures stem from volatile prices of China-sourced key starting materials (KSMs) and compliance gaps at MSME facilities, yet both forces are driving the sector toward vertical integration and quality-system upgrades that strengthen long-run competitiveness.

India Active Pharmaceutical Ingredients (API) Market Trends and Insights

Government PLI & Bulk-Drug-Park Push for Self-Reliance

Thirty-two PLI projects worth Rs 4,024 crore are operational, exceeding originally sanctioned investment and enabling domestic synthesis of critical molecules such as Penicillin G for the first time in three decades. Bulk-drug parks in Gujarat, Himachal Pradesh and Andhra Pradesh provide solvent-recovery units, effluent treatment and common utilities that lower operating costs. Aurobindo Pharma's new 15,000 tpa Pen-G block exemplifies the turnaround in self-reliance. Import dependence on critical intermediates is forecast to halve once the green-field assets reach nameplate utilization, and the Ministry of Commerce & Industry pegs cumulative private pharma investment at Rs 1.61 lakh-crore since 2021. Faster environmental clearances and single-window approvals shorten project gestation, reinforcing policy impact.

Accelerated Shift of U.S./EU Orders to India Post-Biosecure Act

The 2024 U.S. Biosecure Act restricts federal procurement from firms tied to Chinese biotech entities, compelling originators to diversify supply chains. Indian producers, already running more than 750 U.S. FDA-approved sites, have seen a 50% spike in RFQs and audits since Q3 2024. Cost-per-kg parity favors India; landed quotes sit roughly 20% below Chinese averages for similar quality grades. Regulatory tech-transfer cycles still take 18-24 months, yet India's dossier experience compresses timelines relative to first-time entrants. As Western sponsors sequence departures from Chinese suppliers, rolling contracts give Indian CDMOs multi-year revenue visibility.

Volatile Cost of China-Sourced KSMs Despite Localization

Even with rising domestic capacity, India imported APIs worth Rs 377 billion in FY 2024, roughly 35% of total demand. A sudden 15-20% price surge in fermentation inputs during early 2025 compressed operating margins that analysts expected to climb to 12-14%. Larger corporates hedge via multi-region contracts and captive intermediate blocks; MSMEs, lacking scale, shutter production or defer capacity upgrades, disrupting supply chains. Delays in full PLI park commissioning mean dependence will persist through 2026, keeping input costs volatile.

Other drivers and restraints analyzed in the detailed report include:

- Scale-up in Oncology HPAPI Blocks (Visakhapatnam & Hyderabad)

- Growth of CRDMO Exports Serving Phase I/II Innovators

- Persistent Compliance Gaps at MSME API Units (WHO-GMP)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Merchant suppliers currently contribute under 39% of output but will post a 9.42% CAGR as originators divest legacy synthesis blocks in favor of variable-cost models. The India API market benefits when CDMOs assume regulatory dossier maintenance, validation batches and periodic site audits, freeing sponsor capital for biologics and digital therapeutics launches. Increasingly, innovators bundle early-stage chemistry, toxicology and Phase-I supply under single-vendor contracts that reward scale CDMOs with end-to-end capabilities. Captive manufacture remains viable for high-volume statins or metformin where single-plant economies outweigh transaction overhead. Nevertheless, stricter environmental mandates and inflationary utility tariffs tilt total cost of ownership toward merchant operators. Piramal Pharma Solutions' USD 80 million sterile-injectables expansion in Kentucky underscores the scalability of outsourced platforms to serve global demand.

Second-order benefits include flexible tech-transfer windows, which help sponsors stagger launch waves across geographies, thereby smoothing utilization at merchant sites. The India API market also sees deeper backward integration among top CDMOs; reactor parks now co-locate with solvent-recovery and effluent incineration to streamline EH&S audits. Conversely, captive plants grapple with latent contamination risks tied to product-mix complexity, compelling larger quality-control staffing and higher cost per batch.

Synthetic chemistry still anchors 72.80% of 2025 revenue due to lower capital intensity and well-trodden regulatory precedent. Yet biotech APIs, logging a 9.18% CAGR, will capture incremental value as monoclonal antibodies, recombinant hormones and mRNA vectors reach late-stage trials. Continuous-manufacturing skids and high-throughput crystallizers compress synthetic batch cycles, while fermentation reactors adopt real-time metabolite sensors to boost titers. Laurus Bio's extra 120-crore fermentation block aims at amino-acid and enzyme intermediates demanded by biologics pipelines.

Regulatory complexity remains higher for biotech APIs, necessitating validated viral-clearance steps and advanced characterization platforms. However, price premiums of 3-5 X versus synthetic actives offset added capex. The India API market diversifies risk as hybrid manufacturers leverage existing small-molecule lines to cushion biotech scale-up volatility. Meanwhile, synthetic producers pursue green catalysts and micro-reactor technology to maintain cost leadership.

The India API Market Report is Segmented by Business Model (Captive API, Merchant/Contract API), Synthesis Type (Synthetic APIs, Biotech APIs), Drug Type (Generic, Branded, Biosimilar), Therapeutic Area (Oncology, Anti-Infectives, Cardio-Metabolic, CNS, Respiratory, Others), End-Use (Formulation Companies Domestic, Export-Oriented Formulators, CRDMOs/CDMOs), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Divi's Laboratories Ltd

- Aurobindo Pharma

- Laurus Labs Ltd

- Dr Reddy's Laboratories Ltd

- Sun Pharmaceuticals Industries

- Viatris India (Agila)

- Teva API India

- Lupin

- Cipla

- Zydus Group

- Intas Pharmaceuticals

- Piramal Group

- Biocon Biologics

- Samsung Biologics India JV

- Syngene International

- Torrent Pharmaceuticals

- Granules India

- Glenmark Active Pharma Ingredients

- Hetero Drugs

- Alembic Pharma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government PLI & Bulk-Drug-Park push for self-reliance

- 4.2.2 Accelerated shift of US/EU orders to India post-Biosecure Act

- 4.2.3 Scale-up in oncology HPAPI blocks (Visakhapatnam, Hyderabad clusters)

- 4.2.4 Growth of CRDMO exports serving Phase-I/II innovators

- 4.2.5 Green-chemistry route adoption to lower solvent import bill

- 4.2.6 AI-driven process-optimization cutting cycle-times <=20 %

- 4.3 Market Restraints

- 4.3.1 Volatile cost of China-sourced KSMs despite localization

- 4.3.2 Persistent compliance gaps at MSME API units (WHO-GMP)

- 4.3.3 Talent crunch in large-molecule downstream & containment

- 4.3.4 Rising energy tariffs eroding margins in West-coast plants

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Business Model

- 5.1.1 Captive API

- 5.1.2 Merchant / Contract API

- 5.2 By Synthesis Type

- 5.2.1 Synthetic API

- 5.2.2 Biotech API

- 5.3 By Molecule Size

- 5.3.1 Small-Molecule

- 5.3.2 Large-Molecule / Biologic

- 5.4 By Potency

- 5.4.1 High-Potency API

- 5.4.2 Low/Medium Potency API

- 5.5 By Therapeutic Area

- 5.5.1 Oncology

- 5.5.2 Cardiovascular

- 5.5.3 Infectious Diseases

- 5.5.4 Metabolic Disorders

- 5.5.5 CNS & Neurology

- 5.5.6 Respiratory

- 5.5.7 Others

- 5.6 By End-User

- 5.6.1 Pharma & Biopharma Companies

- 5.6.2 CDMOs / CMOs

- 5.6.3 CROs & Academia

- 5.6.4 Export-Oriented Formulators

- 5.6.5 CRDMOs / CDMOs

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Divi's Laboratories Ltd

- 6.3.2 Aurobindo Pharma Ltd

- 6.3.3 Laurus Labs Ltd

- 6.3.4 Dr Reddy's Laboratories Ltd

- 6.3.5 Sun Pharmaceutical Industries Ltd

- 6.3.6 Viatris India (Agila)

- 6.3.7 Teva API India

- 6.3.8 Lupin Ltd

- 6.3.9 Cipla Ltd

- 6.3.10 Cadila Pharmaceuticals

- 6.3.11 Intas Pharmaceuticals

- 6.3.12 Piramal Pharma Solutions

- 6.3.13 Biocon Biologics

- 6.3.14 Samsung Biologics India JV

- 6.3.15 Syngene International

- 6.3.16 Torrent Pharma

- 6.3.17 Granules India

- 6.3.18 Glenmark Active Pharma Ingredients

- 6.3.19 Hetero Drugs

- 6.3.20 Alembic Pharma

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment