|

시장보고서

상품코드

2035161

인도의 반도체 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)India Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

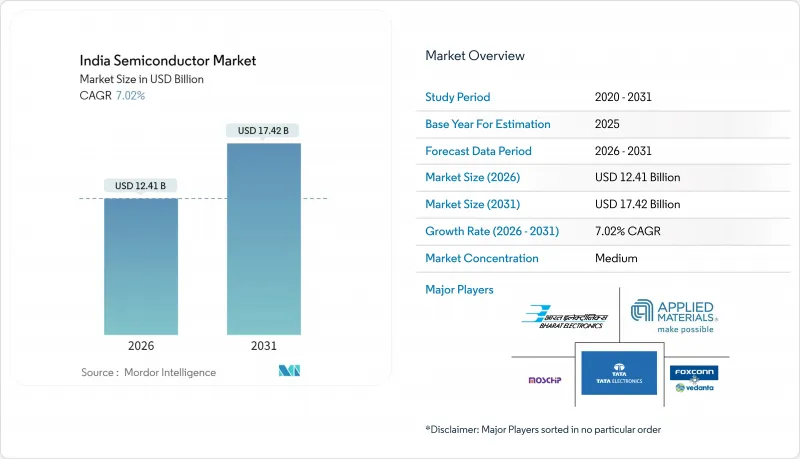

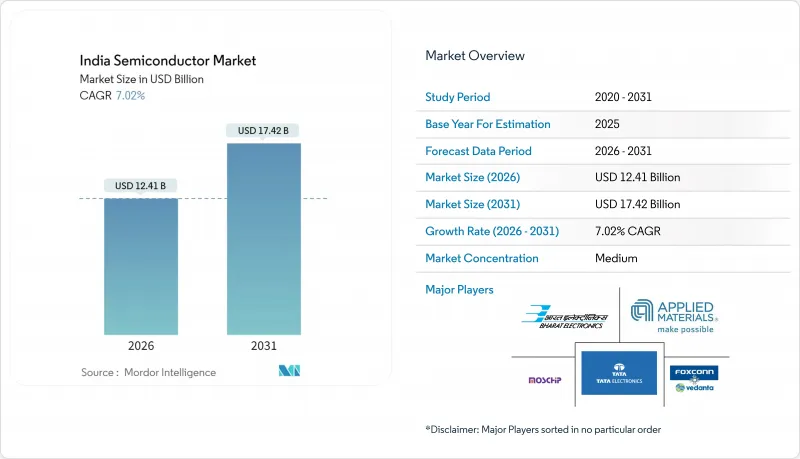

인도의 반도체 시장 규모는 2026년에 124억 1,000만 달러로 예상되며, 2031년까지 174억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 7.02%로 성장할 전망입니다.

"생산연계형 인센티브(PLI) 및 설계연계형 인센티브(DLI) 제도에 기반한 꾸준한 재정지원으로 진입장벽이 낮아져 자본집약적인 웨이퍼 제조 및 조립-테스트-마킹-패키징(ATMP) 시설을 유치하고 있습니다. 특히 28-110나노미터의 성숙한 노드에서 생산 능력의 증설은 아날로그, 전력 관리, 마이크로컨트롤러 디바이스에 대한 국내 수요의 급증과 일치합니다. 운송 장비의 계획적인 전기화, BharatNet 광섬유 네트워크의 확장, 하이퍼스케일 데이터센터의 건설은 각각 다른 실리콘 수요를 불러일으키고 있으며, 다국적 집적 회로 제조업체들이 현지 설계 기반을 강화하도록 촉구하고 있습니다. 한편, 국내 기업들은 오픈소스 RISC-V 코어를 활용하여 틈새 마이크로컨트롤러, 전력반도체, 센서 시장 기회를 개척하고 있어 수입 의존에서 자국 내 가치 창출로 단계적 전환을 시사하고 있습니다.

인도의 반도체 시장 동향과 인사이트

정부 인센티브 제도(PLI, DLI)

생산 연동형 인센티브(PLI) 및 설계 연동형 인센티브(DLI) 프로그램에 총 7,600억 루피(91억 달러)가 투입되어 대상 프로젝트의 자본비용을 최대 50%까지 절감할 수 있습니다. 이를 통해 과거에는 실현하기 어려웠던 신규 팹 건설이 상업적으로도 가능해졌습니다. 타타 일렉트로닉스는 Drela에월5만 장의 웨이퍼 생산을 목표로 하는 300mm 팹 건설을 위한 부지 개발을 시작했으며, Micron Technology의 Sanand에 위치한 백엔드 공장은 2024년 말 첫 패키징된 메모리를 출하했습니다. 2025년 연방 예산안은 리소그래피 장비 및 초순수 가스에 대한 관세를 추가로 철폐하여 건설 기간을 단축하고 수입 장벽을 낮추도록 했습니다. 이러한 재정적 조치와 함께 인도의 반도체 시장은 보다 수직적으로 통합된 기반을 향해 나아가고 있습니다.

운송 부문의 급속한 전동화

'하이브리드 및 전기자동차 보급 및 제조 촉진(FAMEV)' 계획에 따라 충전 인프라에 1,000억 루피(12억 달러)가 배정되어 전기자동차 판매량이 급증하고 있습니다. 고전압 구동 시스템에는 실리콘 카바이드 MOSFET, 절연 게이트 바이폴라 트랜지스터(IGBT) 및 전력 관리 IC가 필요하며, 이는 인도가 기존에 수입에 의존해 왔던 장치 수요를 증가시키고 있습니다. 따라서 자동차 최종 사용자 매출은 CAGR 8.66%를 나타낼 것으로 예측되며, 이는 전체 산업 중 가장 높은 성장률을 보일 것으로 예측됩니다. 건설 예정인 드레라 공장은 생산능력의 일부를 전기 이륜차 및 승용차용 아날로그 전원관리 IC 및 마이크로컨트롤러에 투입할 계획이며, 이를 통해 해외 파운드리에 대한 공급망 의존도를 낮출 수 있을 것으로 기대됩니다.

첨단 공정 기술 분야의 인력 부족

인도전자-반도체협회(IESA)의 추산에 따르면, 2027년까지 8만 5,000명의 추가 인력이 필요함에도 불구하고 설계, 제조, 테스트 분야에서 총 30만 명의 엔지니어가 부족할 것으로 예측됩니다. 현지 대학들은 커리큘럼을 확대하고 있고, 인도의 반도체 미션은 장학금과 실습제도에 50억 루피(6,000만 달러)를 지원하고 있지만, 주요 설계 거점에서는 여전히 20%가 넘는 이직률이 지속되고 있습니다. 이러한 인력 부족은 특히 2나노미터 이하 공정에서 테이프아웃 지연 및 양산 개시까지의 기간이 길어질 수 있는 위험이 있습니다.

부문 분석

트랜지스터는 2025년 개별 디바이스 매출의 48.92%를 차지했지만, 전기자동차 충전기 및 재생에너지 인버터에서 스위칭 손실을 최소화하는 실리콘 카바이드(SiC) 쇼트키 설계가 선호됨에 따라 다이오드는 2031년까지 CAGR 7.82%를 나타낼 것으로 예측됩니다. 따라서 FAME 프로그램과 관련된 전국적인 충전기 도입에 따라 인도의 이산형 다이오드 시장 규모는 확대될 것으로 예측됩니다. 바리스터, 사이리스터, 과도 전압 억제기는 통신 장비 및 가전제품의 서지 보호에서 여전히 중요한 역할을 하고 있으며, 균형 잡힌 제품 구성을 보장하고 있습니다.

2026년 중반 생산 개시 예정인 Cyient-Azimuth의 ARKA GKT-1 시스템온칩은 게이트 드라이버와 MOSFET을 하나의 다이에 통합하여 이륜차 OEM 제조업체의 기판 공간을 줄일 수 있습니다. 'Design Linked Incentive' 제도가 화합물 반도체에 초점을 맞추고 있는 것은 국내 질화갈륨 트랜지스터 개발을 촉진하고, 5G 기지국 장비 및 위성 단말기의 수입 의존도를 낮출 것으로 예측됩니다. 산업 자동화 및 UPS(무정전 전원 공급 장치) 용도에서 절연 게이트 바이폴라 트랜지스터(IGBT)는 고전류 스위칭 분야를 계속 지배하고 있으며, 다이오드 출하가 가속화되고 있는 가운데 트랜지스터 수요의 기반이 되고 있습니다.

2025년에는 LED가 광전자 장비 매출의 38.83%를 차지했지만, 데이터센터의 400기가비트 및 800기가비트 이더넷으로의 업그레이드를 반영하여 레이저 다이오드가 CAGR 8.02%로 이를 상회할 것으로 예측됩니다. 이미지 센서(주로 CMOS)는 연간 출하량 1억 5,000만 대가 넘는 스마트폰 시장을 뒷받침하고 있으며, 옵토커플러는 산업용 모터 구동장치의 전기적 절연을 실현하고 있습니다.

인도 국내 광전자기기 생산은 아직 초기 단계에 있으며, 부품의 80% 이상을 수입에 의존하고 있기 때문에 포토닉 IC 팹에 15%의 자본 보조금을 제공하는 단계적 제조 프로그램이 추진되고 있습니다. BharatNet의 광섬유망 구축에는 2030년까지 약 5,000만 개의 광트랜시버가 필요하며, 수직공진기면발광레이저(VCSEL)의 경우 상당한 규모의 독점 시장이 창출될 것으로 예측됩니다. 케랄라 주와 텔랑가나 주에서는 포토닉스 조립 라인 도입을 검토하고 있으며, 이는 인도의 반도체 시장의 지역 분산화 초기 단계임을 시사하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The India semiconductor market size stood at USD 12.41 billion in 2026 and is projected to reach USD 17.42 billion by 2031, advancing at a 7.02% CAGR during 2026-2031.

A steady fiscal push under the Production Linked Incentive and Design Linked Incentive schemes is lowering entry barriers and attracting capital-intensive wafer fabrication as well as assembly, test, mark, and pack facilities. Mature-node capacity additions, especially at 28-110 nanometers, are aligning with surging domestic demand for analog, power-management, and microcontroller devices. Programmed electrification of transport, expansion of BharatNet fiber, and the construction of hyperscale data centers are each catalyzing distinct waves of silicon demand, prompting multinational integrated-device manufacturers to deepen local design footprints. Meanwhile, domestic firms are leveraging open-source RISC-V cores to tap niche microcontroller, power semiconductor, and sensor opportunities, signaling a gradual shift from import dependence toward indigenous value creation.

India Semiconductor Market Trends and Insights

Government Incentive Schemes (PLI, DLI)

A combined outlay of INR 760 billion (USD 9.1 billion) under the Production Linked Incentive and Design Linked Incentive programs is lowering capital costs by as much as 50% for qualified projects, making greenfield fabs commercially viable where they once were prohibitive. Tata Electronics began site preparation for a 300-millimeter facility in Dholera that targets 50,000 wafer starts per month at mature nodes, and Micron Technology's back-end plant in Sanand dispatched its first packaged memory in late 2024. The Union Budget 2025 further eliminated customs duties on lithography tools and ultrapure gases, trimming build-out timelines and import barriers. Collectively, these fiscal levers are steering the India semiconductor market toward a more vertically integrated footing.

Rapid Electrification of Transport

Electric-vehicle sales are rising precipitously under the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles scheme, which allocates INR 100 billion (USD 1.2 billion) to charging infrastructure. Higher voltage drivetrains require silicon-carbide MOSFETs, insulated-gate bipolar transistors, and power-management ICs, boosting demand for devices that India has historically imported. Automotive end-user revenue is therefore forecast to grow at an 8.66% CAGR, the fastest among all verticals. The upcoming Dholera fab will dedicate part of its capacity to analog power-management ICs and microcontrollers for electric two-wheelers and passenger cars, narrowing supply-chain exposure to offshore foundries.

Skill Shortage in Advanced-node Engineering

The India Electronics and Semiconductor Association estimates a shortfall of 300,000 engineers across design, fabrication and test disciplines, despite a projected need for 85,000 additional professionals by 2027. Local universities are expanding curricula, and the India Semiconductor Mission has set aside INR 5 billion (USD 60 million) for scholarships and apprenticeships, yet attrition rates above 20% persist in key design hubs. The talent squeeze risks delaying tape-outs and stretching ramp-up timelines, especially for 2-nanometer and below.

Other drivers and restraints analyzed in the detailed report include:

- 5G Roll-out and BharatNet Fibre Expansion

- Data-Center and AI Workloads

- Limited Ultrapure Water and Power Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transistors held 48.92% of discrete-device revenue in 2025, yet diodes are expected to grow at a 7.82% CAGR to 2031 as electric-vehicle chargers and renewable-energy inverters favor silicon-carbide Schottky designs that minimize switching losses. The India semiconductor market size for discrete diodes is therefore set to expand in line with nationwide charger rollouts linked to the FAME program. Varistors, thyristors and transient-voltage suppressors remain relevant for surge protection in telecom and consumer devices, ensuring a balanced product mix.

Cyient-Azimuth's ARKA GKT-1 system-on-chip, slated for mid-2026 production, integrates gate drivers and MOSFETs on one die, shrinking board space for two-wheeler OEMs. The Design Linked Incentive scheme's emphasis on compound semiconductors is poised to unlock domestic gallium-nitride transistor development, reducing import reliance for 5G base-station equipment and satellite terminals. Across industrial automation and UPS applications, insulated-gate bipolar transistors continue to dominate high-current switching, anchoring transistor demand even as diode shipments accelerate.

Light-emitting diodes commanded 38.83% of optoelectronic revenue in 2025, but laser diodes are projected to outpace with an 8.02% CAGR, reflecting data-center upgrades to 400-gigabit and 800-gigabit Ethernet. Image sensors, chiefly CMOS, service a buoyant smartphone market of more than 150 million annual shipments, while optocouplers enable galvanic isolation in industrial motor drives.

India's local optoelectronics output remains nascent, with over 80% of parts imported, prompting the phased manufacturing program to offer 15% capital subsidies for photonic IC fabs. BharatNet's fiber build-out will require roughly 50 million optical transceivers by 2030, creating a sizable captive market for vertical-cavity surface-emitting lasers. Initiatives in Kerala and Telangana are exploring photonics assembly lines, signaling early-stage regional diversification within the India semiconductor market.

The India Semiconductor Market Report is Segmented by Device Type (Discrete Semiconductors, Optoelectronics, Sensors and MEMS, and Integrated Circuits), Integrated Circuit Type (Analog, Micro, Logic, and Memory), Technology Node (Less Than or Equal To 3nm, 5nm, 7nm, 16nm, 28nm, and More), End-User Industry (Automotive, Communication, Consumer Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Tata Electronics Private Limited

- Vedanta-Foxconn Semiconductors Limited

- Bharat Electronics Limited

- MosChip Technologies Limited

- Applied Materials India Private Limited

- ASM Technologies Limited

- Suchi Semiconductors Private Limited

- NXP Semiconductors N.V.

- HCL Technologies Limited

- Infineon Technologies AG

- Renesas Electronics Corporation

- STMicroelectronics N.V.

- Powerchip Semiconductor Manufacturing Corporation

- Intel Corporation

- Samsung Electronics Co., Ltd.

- Qualcomm Incorporated

- Micron Technology, Inc.

- Texas Instruments Incorporated

- MediaTek Inc.

- Taiwan Semiconductor Manufacturing Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Incentive Schemes (PLI, DLI)

- 4.2.2 Rapid Electrification of Transport

- 4.2.3 5G Roll-out and BharatNet Fibre Expansion

- 4.2.4 Data-Centre and AI Workloads

- 4.2.5 Indigenous GaN/SiC Pilot Fabs

- 4.2.6 Trusted Defense-grade Fab Accreditation

- 4.3 Market Restraints

- 4.3.1 Skill Shortage in Advanced-node Engineering

- 4.3.2 Limited Ultrapure Water and Power Infrastructure

- 4.3.3 Fragmented OSAT Capacity

- 4.3.4 Land and Environmental Clearance Delays

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory and Incentive Framework

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of Substitute Products

- 4.7.4 Threat of New Entrants

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 SWOT Analysis (India IC Design D Fab D ATP)

- 4.9 Investment Analysis (CapEx Trends and Funding Flows)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 Discrete Semiconductors

- 5.1.1.1 Diodes

- 5.1.1.2 Transistors

- 5.1.1.3 Power Transistors

- 5.1.1.4 Rectifiers and Thyristors

- 5.1.1.5 Other Discrete Devices

- 5.1.2 Optoelectronics

- 5.1.2.1 Light-Emitting Diodes (LEDs)

- 5.1.2.2 Laser Diodes

- 5.1.2.3 Image Sensors

- 5.1.2.4 Optocouplers

- 5.1.2.5 Other Optoelectronic Devices

- 5.1.3 Sensors and MEMS

- 5.1.3.1 Pressure Sensors

- 5.1.3.2 Magnetic Field Sensors

- 5.1.3.3 Actuators

- 5.1.3.4 Acceleration and Yaw Rate Sensors

- 5.1.3.5 Temperature and Other Sensors

- 5.1.4 Integrated Circuits

- 5.1.4.1 By Integrated Circuit Type

- 5.1.4.1.1 Analog

- 5.1.4.1.2 Micro

- 5.1.4.1.2.1 Microprocessors (MPU)

- 5.1.4.1.2.2 Microcontrollers (MCU)

- 5.1.4.1.2.3 Digital Signal Processors

- 5.1.4.1.3 Logic

- 5.1.4.1.4 Memory

- 5.1.4.2 By Technology Node (For Integrated Circuits)

- 5.1.4.2.1 Less Than or Equal to 3nm

- 5.1.4.2.2 5 nm

- 5.1.4.2.3 7 nm

- 5.1.4.2.4 16 nm

- 5.1.4.2.5 28 nm

- 5.1.4.2.6 Greater Than 28nm

- 5.1.4.1 By Integrated Circuit Type

- 5.1.1 Discrete Semiconductors

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Communication (Wired and Wireless)

- 5.2.3 Consumer Electronics

- 5.2.4 Industrial

- 5.2.5 Computing and Data Storage

- 5.2.6 Data Center

- 5.2.7 Artificial Intelligence

- 5.2.8 Government (Aerospace and Defense)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, MoUs)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments}

- 6.4.1 Tata Electronics Private Limited

- 6.4.2 Vedanta-Foxconn Semiconductors Limited

- 6.4.3 Bharat Electronics Limited

- 6.4.4 MosChip Technologies Limited

- 6.4.5 Applied Materials India Private Limited

- 6.4.6 ASM Technologies Limited

- 6.4.7 Suchi Semiconductors Private Limited

- 6.4.8 NXP Semiconductors N.V.

- 6.4.9 HCL Technologies Limited

- 6.4.10 Infineon Technologies AG

- 6.4.11 Renesas Electronics Corporation

- 6.4.12 STMicroelectronics N.V.

- 6.4.13 Powerchip Semiconductor Manufacturing Corporation

- 6.4.14 Intel Corporation

- 6.4.15 Samsung Electronics Co., Ltd.

- 6.4.16 Qualcomm Incorporated

- 6.4.17 Micron Technology, Inc.

- 6.4.18 Texas Instruments Incorporated

- 6.4.19 MediaTek Inc.

- 6.4.20 Taiwan Semiconductor Manufacturing Company Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment