|

시장보고서

상품코드

2044177

헤비 및 씬 게이지 열성형 플라스틱 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Heavy Gauge And Thin Gauge Thermoformed Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

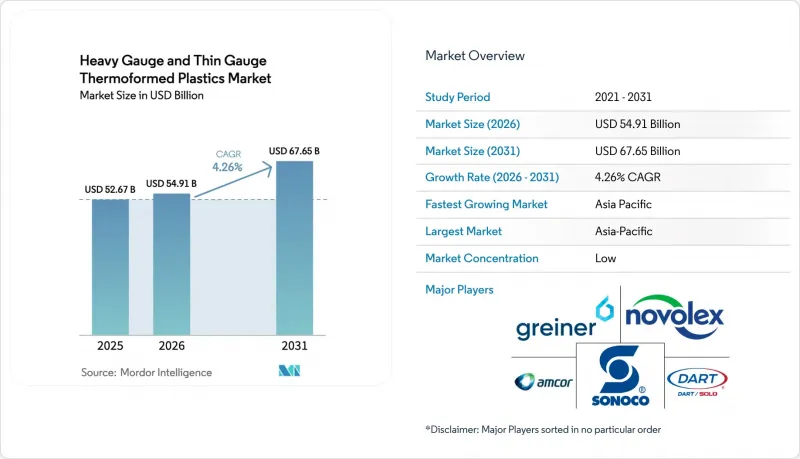

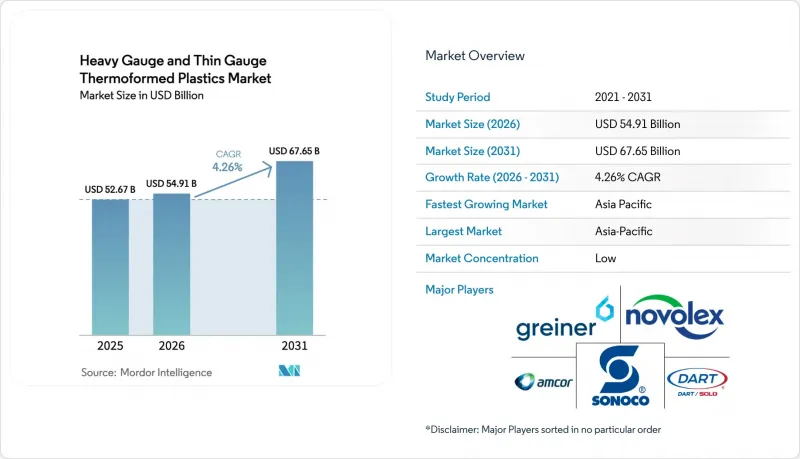

헤비 및 씬 게이지 열성형 플라스틱 시장 규모는 2025년 526억 7,000만 달러에서 2026년에는 549억 1,000만 달러로 확대되어 2031년까지 676억 5,000만 달러에 이를 것으로 예상되고 있으며 2026년부터 2031년까지 CAGR 4.26%로 성장할 전망입니다.

컨버터 업체들은 지속적인 식품 안전 규제, 확대되는 의약품 콜드체인, 순환 경제에 대한 인센티브에 대응하고 있습니다. 그들은 수지 블렌드 재설계, rPET 오염 제거에 대한 투자, 디지털 인몰드 라벨링 도입을 추진하고 있습니다. 아시아태평양에서는 각국의 재생재 함량 의무화가 강화되면서 시트 수요가 증가하고 있습니다. 한편, 북미의 생산자들은 PFAS의 단계적 폐지에 따른 비용과 성형 섬유로의 대체에 따른 위험에 직면해 있습니다. 업계에서는 Novolex가 Pactiv Evergreen을 67억 달러에 인수한 사례에서 알 수 있듯이 규모의 경제와 통합된 재활용을 지향하는 추세를 볼 수 있습니다. 두꺼운 벽체 제품의 성장은 전기자동차 및 산업용 로봇의 경량화 노력에 힘입어 성장하고 있습니다. 또한, 의약품 블리스터 포장에 탈중합 rPET 필름을 채택한 것은 규제 환경 하에서 재생 소재의 유효성을 입증하는 것입니다.

세계 헤비 및 씬 열성형 플라스틱 시장 동향 및 인사이트

신선식품 및 냉동식품 포장 수요 급증

세계 소매업체들은 음식물 쓰레기를 줄이고 생산자책임재활용제도(EPR) 수수료를 절감하기 위해 가스 대체 트레이와 전자레인지용 CPET 용기를 채택하고 있습니다. 결정질 PET와 폴리프로필렌으로 제작된 다실 구조 설계는 반복적인 동결 및 해동 사이클을 견딜 수 있어 보존 기간을 단축하지 않고도 브랜드를 다양화할 수 있습니다. 유럽에서는 폐자재를 포함하고 내열성을 갖춘 Perstorp의 Akestra 공압출 폴리에스테르가 승인을 받음에 따라 트레이에서 트레이로의 재활용이 더욱 활발해지고 있습니다. 영국은 2024년 EPR 규정을 도입하여 검증된 폐쇄형 루프 회수에 대한 요금 상쇄를 허용하고 있습니다. 이는 Cirrec이 연간 수십억 개의 트레이를 처리하겠다는 야심찬 확장 계획을 포함한 투자를 촉진하고 있습니다. 한편, 북미에서는 공급이 부족합니다. 2023년 국내에서 재활용되는 PET 열성형 용기는 한정된 양에 불과하고, 식품용 rPET 플레이크를 둘러싼 경쟁이 치열해지고 있기 때문입니다.

제약용 블리스터 및 트레이의 사용 확대

규제 당국이 추출물과 용출물에 대한 규제를 강화하면서 재활용 가능한 고차단성 필름에 대한 수요가 증가하고 있습니다. 2024년, Amkor는 위스콘신 주에 ISO 13485를 준수하는 열성형과 다이컷 뚜껑을 단일 시설에 통합한 자동화된 클래스 7 생산 능력을 구축했습니다. 테크닙렉스는 알펙과 함께 탈중합 기술을 활용하여 유럽 약전 및 미국 약전 기준을 모두 충족하면서 폴리에스테르 재활용 스트림에서 재활용성을 유지하는 블리스터 필름을 출시했습니다. EU의 PPWR 규제에 따라 2038년 이후에는 재활용성 A 또는 B 등급만 허용되기 때문에 컨버터는 모노 PET 구조로 전환해야 합니다.

성형 섬유 트레이의 대체 위험

2024년, Dart Container는 Palpac과 제휴하여 미국에 건식 성형 섬유 라인을 도입했습니다. 이 라인은 기존 펄프 설비보다 훨씬 빠른 속도로 가동되며, 테이크아웃 서비스에서 저배리어성 열성형 용기를 대체하는 것을 목표로 하고 있습니다. 이구스도의 '인바폼'은 고형 표백판(SBB)을 기판으로 한 제품으로, 성형성이 우수하고 종이 재활용이 가능해 어린이 간편식용 제품으로 각광을 받고 있습니다. 하지만, 섬유계 대체 소재는 문제점도 있습니다. 내유성 및 내습성 문제가 있고, 산업용 퇴비 처리 인프라도 제한적이며, 주로 미국 및 유럽연합(EU) 일부 지역에만 국한되어 있습니다. 이 때문에 육류, 해산물 등 장벽이 높은 시장에서의 가능성이 제한되고 있습니다.

부문 분석

2025년 기준, 얇은 벽 제품은 두꺼운 벽과 얇은 벽 열성형 플라스틱 시장의 76.22%를 차지하고 있으며, 2026년부터 2031년까지 예측 기간 동안 연평균 4.33%의 성장률을 보일 것으로 예측됩니다. 푸드서비스용 조개껍질 용기, 조제식품 뚜껑, 결정화 폴리에틸렌 테레프탈레이트(CPET)로 만든 즉석식품 트레이가 소비량의 대부분을 차지하지만, 의료용 블리스터 포장은 더 높은 수익률을 가져옵니다. 컨버터 업체들은 2030년까지 매출의 100%를 재활용 또는 재생 가능한 소재로 달성하는 것을 목표로 하고 있으며, 이는 재생 폴리에틸렌 테레프탈레이트(rPET) 및 단일 소재인 폴리프로필렌 기판의 채택을 촉진하고 있습니다.

0.060-0.500인치 후판은 자동차, 백색가전 및 산업용 케이스에 사용됩니다. 이러한 응용 분야에서는 대형 부품 및 중량 생산에서 진공 성형의 높은 비용 효율성이 활용되고 있습니다. 예를 들어, 로클링의 컨버터블 루프 빔은 메르세데스-벤츠의 프로그램에서 경량화를 실현하여 부품 수를 크게 줄였습니다. 또한, 인몰드 코팅 필름이 적용된 특수 아크릴로니트릴-부타디엔-스티렌/폴리카보네이트(ABS/PC) 블렌드 소재를 사용함으로써 후공정 마무리 작업을 줄일 수 있습니다. 그러나 연간 생산량이 10만 대를 넘어서면 사출 금형의 경제성이 더 유리해지기 때문에 두꺼운 벽체 용도 시장 점유율은 제한적일 수밖에 없습니다.

지역별 분석

아시아태평양은 2025년 세계 매출의 44.45%를 차지했으며, 가처분 소득 증가, 엄격한 식품 안전 기준, 의약품 생산량 확대에 힘입어 2026-2031년의 예측 기간 동안 연평균 4.46%의 성장률을 보일 것으로 예측됩니다. 재활용 소재 함유량 관련 법규에 대응하기 위해 인도는 국내 트레이 수요를 충족시키기 위해 이집트에 PET 재활용 시설을 개설했습니다. 중국에서는 콜드체인 기준 강화와 더불어 EC의 밀키트 출시로 인해 얇은 육류 제품의 소비가 급증하고 있습니다. 한편, 아세안 지역에서는 위탁가공 분야에 대한 외국간접투자(FDI)를 유치하고 있습니다.

북미는 잘 구축된 외식산업 네트워크에 힘입어 여전히 2위 시장 규모를 유지하고 있습니다. Novolex는 시장 점유율을 유지하기 위해 폐쇄형 rPET 조달과 PFAS 프리 코팅에 중점을 두고 대규모 전략적 통합을 추진하고 있습니다. 캘리포니아주 SB 54법에 따라 열성형 베일의 분리수거가 가속화되고 있습니다. 그러나 재활용률이 유럽에 비해 뒤쳐져 있는 북미는 정책 입안자들의 주목을 받고 있습니다.

유럽에서는 엄격한 규제에 직면해 있습니다. 2030년까지 PPWR(플라스틱 포장 규제)은 식품 접촉용 PET에 재생재 사용을 의무화하고, 2035년에는 재활용 가능성 기준을 설정합니다. 스위스 바흐만(BACHMANN)사의 라인으로 대표되는 제염 공정에 대한 투자가 규제 준수를 보장하고 있습니다. 트레이의 회수량은 연간 상당한 규모에 달하지만, 주로 다층 구조의 문제로 인해 재활용되는 것은 극히 일부에 불과합니다. 한편, 남미, 중동 및 아프리카는 도시 소매업과 제약 산업의 충전 및 마감 능력이 확대됨에 따라 잠재적인 성장 지역으로 부상하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Heavy Gauge and Thin Gauge Thermoformed Plastics Market size is expected to increase from USD 52.67 billion in 2025 to USD 54.91 billion in 2026 and reach USD 67.65 billion by 2031, growing at a CAGR of 4.26% over 2026-2031.

Converters are responding to ongoing food safety regulations, an expanding pharmaceutical cold chain, and incentives for a circular economy. They are redesigning resin blends, investing in rPET decontamination, and incorporating digital in-mold labeling. In the Asia-Pacific, intensified national recycled-content mandates are driving up sheet demand. Meanwhile, North American producers are grappling with the costs of phasing out PFAS and the risks of substituting molded fiber. The industry is witnessing a trend toward scale efficiency and integrated recycling, highlighted by Novolex's USD 6.7 billion acquisition of Pactiv Evergreen. Heavy-gauge growth is bolstered by lightweighting initiatives in electric vehicles and industrial robots. Furthermore, the adoption of depolymerized rPET film in pharmaceutical blisters underscores the validation of recycled content in regulated environments.

Global Heavy Gauge And Thin Gauge Thermoformed Plastics Market Trends and Insights

Demand Spike from Fresh and Frozen Food Packaging

Global retailers are adopting modified-atmosphere trays and microwave-ready CPET containers to reduce food waste and take advantage of extended producer responsibility (EPR) fee reductions. Crystalline PET and polypropylene multicompartment designs endure repeated freeze-thaw cycles, enabling brand diversification without reducing shelf life. In Europe, tray-to-tray recycling is gaining traction after Perstorp's Akestra co-extrusion polyester, which features post-consumer content and heat resistance, received an endorsement. The United Kingdom introduced EPR rules in 2024, permitting fee offsets for verified closed-loop collections. This has spurred investments, including Cirrec's ambitious expansion to process billions of trays annually. Meanwhile, North America faces a tight supply, as only a limited amount of PET thermoforms were recycled domestically in 2023, increasing competition for food-grade rPET flake.

Expanding Pharma-Grade Blister and Tray Usage

As regulators tighten limits on extractables and leachables, the demand for recyclable high-barrier films is increasing. In 2024, Amcor established automated Class 7 capacity in Wisconsin, integrating ISO 13485-compliant thermoforms and die-cut lids within a single facility. TekniPlex, in collaboration with Alpek, utilized depolymerization to introduce a blister film that ensures compliance with both European and U.S. Pharmacopeias while maintaining recyclability in polyester streams. Under EU PPWR regulations, only A or B recyclability grades will be accepted after 2038, driving converters toward mono-PET structures.

Molded-Fiber Tray Substitution Risk

In 2024, Dart Container partnered with PulPac, introducing dry-molded-fiber lines to the United States. These lines operate significantly faster than traditional pulp equipment, with the goal of replacing low-barrier thermoforms in takeaway services. Iggesund's Inverform, a solid-bleached-board substrate, boasts formability and compatibility with paper recycling, making it more appealing for chilled ready meals. However, fiber alternatives face challenges. They struggle with grease and moisture resistance and encounter limited industrial composting infrastructure, primarily confined to select regions in the United States and the European Union. This restricts their potential in high-barrier markets such as meat and seafood.

Other drivers and restraints analyzed in the detailed report include:

- Closed-Loop rPET Thermoforming Initiatives

- Autonomous Mobile-Robot Housings Require Large Thermoformed Enclosures

- Tightening PFAS Barrier-Coating Regulations on Food Trays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thin-gauge captured 76.22% of the Heavy Gauge and Thin Gauge Thermoformed Plastics market share in 2025 and is expected to grow at a 4.33% CAGR during the forecast period of 2026-2031. Foodservice clamshells, deli lids, and crystallized polyethylene terephthalate (CPET) ready-meal trays dominate in volume consumption, while medical blisters offer higher margins. Converters aim to achieve 100% recyclable or renewable sales by 2030, driving the adoption of recycled polyethylene terephthalate (rPET) and mono-material polypropylene substrates.

Heavy-gauge sheets, ranging from 0.060 to 0.500 inches, are used in automotive, white-goods, and industrial housings. These applications benefit from the cost-effectiveness of vacuum forming for large parts and mid-volume production. For example, Rochling's convertible roof beam reduced weight in a Mercedes-Benz program and decreased the part count significantly. Additionally, specialized acrylonitrile butadiene styrene/polycarbonate (ABS/PC) blends with in-mold paint films reduce the need for downstream finishing labor. However, when annual volumes exceed 100,000 units, the economics of injection-molding tooling become more favorable, limiting the addressable share for heavy-gauge applications.

The Heavy Gauge and Thin Gauge Thermoformed Plastics Market Report is Segmented by Gauge Type (Heavy Gauge and Thin Gauge), End-Use Industry (Automotive and Transportation, Food and Beverage Packaging, Medical and Pharmaceutical, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 44.45% of global revenues in 2025 and is set to post a 4.46% CAGR during the forecast period of 2026-2031, driven by rising disposable income, stringent food-safety codes, and escalating pharmaceutical output. In a move to meet its recycled-content law, India inaugurated a PET recycling facility in Egypt to satisfy domestic tray demand. China's enhanced cold-chain standards, coupled with the rise of e-commerce meal kits, are fueling a surge in thin-gauge consumption. Meanwhile, the ASEAN region is attracting foreign direct investment (FDI) in contract processing.

North America, supported by established foodservice networks, remains the second-largest player. Novolex is strategically integrating on a large scale, focusing on closed-loop rPET sourcing and PFAS-free coatings to maintain its market share. California's SB 54 is accelerating thermoform bale separation. However, with a recycling rate that lags behind Europe, North America is drawing increased attention from policymakers.

Europe faces stringent regulations. By 2030, PPWR mandates recycled content in contact-sensitive PET, with recyclability standards set for 2035. Investments in decontamination processes, exemplified by BACHMANN's line in Switzerland, are ensuring compliance. While tray collections exceed significant annual volumes, only a fraction is recycled, largely due to challenges with multilayer formats. Meanwhile, South America and the Middle-East and Africa are emerging as regions with potential, as urban retail and pharmaceutical fill-finish capacities expand.

- Amcor plc

- Anchor Packaging Inc.

- Brentwood Industries, Inc.

- D&W Fine Pack

- Dart Container Corporation

- Dordan Manufacturing Company, Incorporated.

- Fabri-Kal

- Genpak, LLC

- Greiner AG

- Novolex

- Peninsula Plastics Company Inc.

- Placon

- Sealed Air

- Silgan Plastics

- Sonoco Products Company

- SPENCER INDUSTRIES INCORPORATED

- Tekni-Plex, Inc.

- Universal Plastics

- Winpak

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand spike from fresh and frozen food packaging

- 4.2.2 Expanding pharma-grade blister and tray usage

- 4.2.3 Closed-loop rPET thermoforming initiatives

- 4.2.4 Autonomous mobile-robot (AMR) housings require large thermoformed enclosures

- 4.2.5 Digital in-mold-labeling (IML) adoption for short SKU cycles

- 4.3 Market Restraints

- 4.3.1 Molded-fiber tray substitution risk

- 4.3.2 Tightening PFAS barrier-coating regulations on food trays

- 4.3.3 Shortage of high-clarity rPET flake for recycled-content mandates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Gauge Type

- 5.1.1 Heavy Gauge

- 5.1.2 Thin Gauge

- 5.2 By End-Use Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Food and Beverage Packaging

- 5.2.3 Medical and Pharmaceutical

- 5.2.4 Electrical and Electronics

- 5.2.5 Industrial Equipment

- 5.2.6 Consumer Goods

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 United Kingdom

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Turkey

- 5.3.5.4 South Africa

- 5.3.5.5 Nigeria

- 5.3.5.6 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Anchor Packaging Inc.

- 6.4.3 Brentwood Industries, Inc.

- 6.4.4 D&W Fine Pack

- 6.4.5 Dart Container Corporation

- 6.4.6 Dordan Manufacturing Company, Incorporated.

- 6.4.7 Fabri-Kal

- 6.4.8 Genpak, LLC

- 6.4.9 Greiner AG

- 6.4.10 Novolex

- 6.4.11 Peninsula Plastics Company Inc.

- 6.4.12 Placon

- 6.4.13 Sealed Air

- 6.4.14 Silgan Plastics

- 6.4.15 Sonoco Products Company

- 6.4.16 SPENCER INDUSTRIES INCORPORATED

- 6.4.17 Tekni-Plex, Inc.

- 6.4.18 Universal Plastics

- 6.4.19 Winpak

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment