|

시장보고서

상품코드

2044217

카톤 보드 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

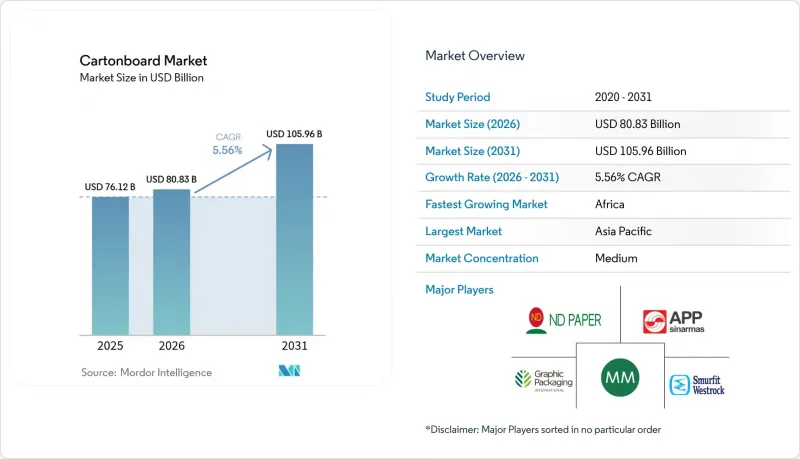

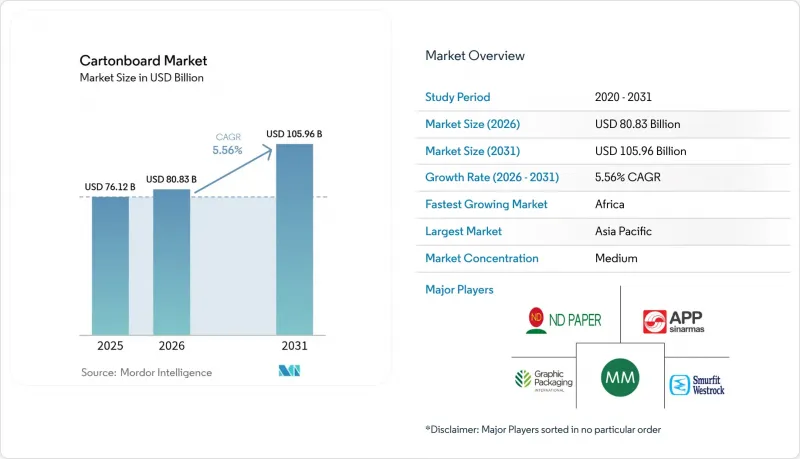

카톤 보드 시장 규모는 2025년에 761억 2,000만 달러, 2026년에 808억 3,000만 달러가 되어, 2031년까지 1,059억 6,000만 달러에 이를 것으로 예측되며, 2026-2031년까지 CAGR 5.56%로 성장할 전망입니다.

완전한 재활용 가능성에 대한 강력한 정책적 압력, 플라스틱을 사용하지 않는 포장에 대한 소비자의 선호도 증가, EC 부문에서의 경량화 확산으로 인해 브랜드 소유자는 섬유 기반 솔루션으로 전환하고 있습니다. 특히 식품, 음료, 화장품 부문에서 배리어 코팅 보드로 만든 접이식 카톤, 슬리브, 액체 포장재는 경질 폴리에틸렌 테레프탈레이트(PET) 및 폴리프로필렌(PP) 포장재를 대체하고 있습니다. 디지털 인쇄기는 소비자 직접 판매(DTC) 브랜드에 수익성 높은 소량 생산을 가능하게 하고, 고수율의 미세섬유화 셀룰로오스는 평량 10-15% 감소를 가능하게 하여 부피 중량에 따른 운임 절감으로 이어집니다. 공급 측면에서는 버진 펄프 공장이 의약품 및 고급 제품 부문에서 고부가가치 수주를 지속하고 있는 반면, 통합 재활용 업체들은 베일의 품질 저하를 상쇄하기 위해 광학 선별 기술에 집중하고 있습니다.

세계 카톤 보드 시장 동향과 인사이트

전자상거래에서 카톤 보드에서 보드로의 대체가 급증하고 있습니다.

D2C(소비자 직접 판매) 네트워크는 이중벽 판지 상자에서 단층 보드 슬리브로 전환하여 소포의 무게를 20 - 30% 감소시켜 운송 업체의 부피 중량 요금을 줄였습니다. 아마존과 알리바바는 현재 플라스틱 에어필로우 대신 종이 완충재를 채택하고 있으며, 이로 인해 완충재에 대한 수요가 연간 3.9%의 성장률을 보이고 있습니다. 나이키와 애플은 의류와 전자제품의 포장을 재설계하고 판지 보드를 완전히 없앴다. 이에 따라 충분한 적층 강도를 갖춘 200-250g/m2의 접이식 보드에 대한 수요가 발생하고 있습니다. 이러한 변화는 당일 배송이 보편화된 북미와 유럽 도시 지역에서 고부피, 경량 보드를 공급할 수 있는 제지업체에게 새로운 수익원을 가져다주고 있습니다.

FMCG 산업에서 플라스틱이 없는 1차 포장으로 전환하기

세계 소비재 대기업들은 폴리에틸렌 층을 사용하지 않고 유분, 습기, 산소 차단성을 유지하는 분산 코팅 보드를 채택하여 SKU의 리뉴얼을 진행하고 있습니다. 2026년 1월에 출시된 스트라 엔소의 'Performa Lumi'는 화장품 브랜드에 맞게 조정된 광물성 안료에 의한 불투명도를 기재하고 있습니다. 헨켈은 2025년 10월에 접착제용 종이 카트리지를 도입하여 연간 120톤의 플라스틱을 줄였습니다. 유럽의 포장 및 포장 폐기물 규제에 따라 2030년까지 모든 포장은 재활용이 가능해야 하며, 폴리올레핀에 비해 단가가 4-5배 높지만 보드의 채택이 가속화되고 있습니다.

에너지 가격 변동으로 제지 공장 수익률 압박

전력과 가스는 제지 공장 지출의 10-15%를 차지합니다. 2025년 1월 미국 천연가스 가격은 MMBtu당 평균 3.30달러로 2022년 8월의 최고치인 9.50달러를 크게 밑돌고 있지만, 유럽의 전력 가격은 여전히 높은 수준을 유지하고 있습니다. 자가발전 및 재생에너지 전력구매계약(PPA)을 맺은 통합 제조업체는 수익률을 지키고 있지만, 현물가격의 영향을 받는 독립 재활용업체는 스프레드 축소에 직면해 있습니다.

부문 분석

버진 펄프는 액체 포장 보드와 고체 표백 보드에 대한 수요 증가를 포착하고 음료 및 제약 산업 구매자가 백색도와 인장 강도를 중요시하는 가운데 CAGR 5.93%로 확대될 것으로 예측됩니다. 빌레루드의 FSC 인증을 획득한 'Enviro-FBB'는 진열 효과를 높이기 위해 불투명도를 중시하는 화장품 업계와 계약을 맺었습니다. 사피(Sappi)가 2024년 서머셋 공장에 52만 쇼트톤의 생산능력을 증설함에 따라 FDA 기준에 부합하는 기판의 미국 공급량이 증가했습니다. 2025년 생산량 중 재생 등급이 57.82%를 차지하지만, 높은 오염도와 섬유의 피로로 인해 고휘도 응용에 대한 적합성이 제한되어 있습니다. DS Smith가 컨테이너 보드에 100% 재생섬유를 사용한다는 점은 DS Smith의 원가 우위를 뒷받침하고 있지만, 여전히 버진 펄프를 사용한 접이식 카톤 보드 시장은 톤당 수익에서 재생재 시장을 능가하고 있습니다.

재활용 섬유는 단위당 경제성이 중시되는 접이식 박스보드에서 선도적인 위치를 유지하고 있으며, 그래픽 패키징은 고도의 탈묵 기술을 통해 ISO 80 이상의 백색도를 유지하면서 원재료의 80%를 회수 스트림에서 조달하고 있습니다. 나인드래곤즈 페이퍼는 아시아에 160개 거점을 두고 국내 및 북미의 중고 판지 베일을 처리하고 있습니다. 재생 중핵판 판지 시장 점유율은 견조하게 유지될 것으로 예상되지만, FDA와 EU의 엄격한 식품 접촉 규제가 적용되는 프리미엄 틈새 시장에서는 버진 소재의 생산 능력이 추가적인 가치를 창출할 가능성이 높을 것으로 보입니다.

순백의 미학을 중시하는 고급 화장품 및 의약품 포장에 힘입어 솔리드 표백 보드(SBB)는 2031년까지 연평균 복합 성장률(CAGR) 6.72%로 가장 높은 성장률을 나타낼 것으로 예측됩니다. 사피의 서머셋 공장 확장은 이러한 급증에 직접적으로 기여하고 있으며, 강성과 FDA 승인이 필요한 블리스터 카드와 식품 트레이를 공급하고 있습니다. 접이식 보드(FBB)는 시리얼, 과자, 냉동식품 등 다양한 용도로 사용할 수 있는 범용성으로 인해 2025년 카톤 보드 시장 규모의 38.13%를 차지했습니다. Stora Enso의 FiberLight를 기반으로 한 'Performa Nova'는 굽힘 강성을 유지하면서 가공업체가 재료 사용량을 10-15% 절감하는 데 기여했습니다.

액체 포장 보드는 Elopak의 "Natural White Board"로 인해 호황을 누리고 있으며, 이는 PET 병과 비교하여 단위당 온실가스를 14% 감소시킵니다. 화이트 라이닝 마분지는 비용에 민감한 식품 부문에 기여하고 있으며, 푸드서비스 보드는 아프리카 및 아시아의 플라스틱 금지 조치에 따라 폴리스티렌 클램쉘 용기의 대안으로 활용되고 있습니다. SBB의 성장세에도 불구하고, 컨버터가 강성, 인쇄적합성, 그래픽 표현력의 절묘한 균형을 활용하기 때문에 FBB는 계속해서 물량의 주축이 될 것으로 보입니다.

지역별 분석

아시아태평양은 중국의 8% 생산능력 증가와 인도의 2,400만 톤의 포장재 소비에 힘입어 2025년 매출의 43.62%를 차지했습니다. 현지 제지업체들은 에너지 효율이 높은 기계에 대한 정부의 우대 조치의 혜택을 받고 있으며, 지역 재활용 업체들은 사용한 판지 용기의 수입 제한을 상쇄하기 위해 탈묵 처리를 확대되고 있습니다. 일본, 한국, 호주에서는 재활용률이 70%를 넘어 FBB 등급에서 재생 펄프의 높은 대체가 가능하여 지역 내 카톤 보드 시장을 견인하고 있습니다.

아프리카는 2031년까지 연평균 6.57%로 가장 빠르게 성장할 것으로 예측됩니다. 케냐의 플라스틱 제품 금지 조치로 인해 접이식 판지 수요가 증가하고 있으며, 남아공의 25억 달러 규모의 제지 부문에는 몬디와 사피의 투자가 유입되고 있습니다. 나이지리아, 이집트, 에티오피아에서는 FMCG(일용소비재) 출하량이 두 자릿수 성장을 기록하며 콜드체인 물류를 견딜 수 있는 2차 포장에 대한 수요를 자극하고 있습니다. 사우디아라비아와 아랍에미리트 등 중동 시장은 소매 체인 확대와 전자상거래 가속화에 따라 5.8%의 성장이 예상됩니다.

북미와 유럽에서는 생산능력의 재편이 진행되는 한편, 디지털 인쇄기 및 배리어 코팅 라인에 대한 자본투입이 이루어지고 있습니다. 국제제지(International Paper)는 2024년 100만 톤의 구식 컨테이너 보드 생산능력을 감축하고, 미국 패킹코퍼레이션(Packing Corporation of America)은 공급 부족을 해소하기 위해 18억 달러에 그레이프의 사업부문을 인수했습니다. 유럽의 종이 재활용률은 72%에 달하며, 2030년까지 재활용이 가능하도록 의무화하는 '포장폐기물 규제'를 보완하는 형태로 진행되고 있습니다. 남미에서는 2027년 가동 예정인 클라빈사의 90만 톤 규모의 PUMA II 라인이 호재로 작용하고 있으며, 브라질은 북미 바이어를 대상으로 한 수출 거점으로서의 입지를 다져가고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The cartonboard market size is projected to be USD 76.12 billion in 2025, USD 80.83 billion in 2026, and reach USD 105.96 billion by 2031, growing at a CAGR of 5.56% from 2026 to 2031.

Strong policy pressure for full recyclability, mounting consumer preference for plastic-free packs, and widespread e-commerce lightweighting are steering brand owners toward fiber-based solutions. Folding cartons, sleeves, and liquid packs made from barrier-coated board are displacing rigid polyethylene terephthalate and polypropylene formats, especially in food, beverage, and cosmetics channels. Digital printing presses are unlocking profitable micro-runs for direct-to-consumer brands, while high-yield microfibrillated cellulose enables 10%-15% basis-weight cuts that translate into lower dimensional-weight freight charges. On the supply side, virgin-fiber mills continue to win premium orders in pharmaceuticals and luxury goods, whereas integrated recyclers bank on optical sorting to offset declining bale quality.

Global Cartonboard Market Trends and Insights

E-commerce Corrugated-to-Cartonboard Substitution Surge

Direct-to-consumer networks are trading double-wall corrugated boxes for single-wall cartonboard sleeves that trim parcel mass by 20%-30%, lowering carrier dimensional-weight fees. Amazon and Alibaba now deploy paper void fill in lieu of plastic air pillows, driving 3.9% annual growth in cushioning grades. Nike and Apple redesigned apparel and electronics packs to remove corrugated altogether, opening demand pockets for 200-250 g-per-m2 folding boxboard with adequate stacking strength. The shift is creating fresh revenue for mills able to supply high-bulk, lightweight board in North American and European metro zones where same-day delivery dominates.

FMCG Pivot to Plastic-Free Primary Packaging

Global consumer-goods groups are retrofitting SKUs with dispersion-coated board that preserves grease, moisture, and oxygen barriers without polyethylene layers. Stora Enso's Performa Lumi, released January 2026, offers mineral pigment opacity tailored to beauty labels. Henkel rolled out paper cartridges for adhesives in October 2025, eliminating 120 tons of plastic per year. The European Packaging and Packaging Waste Regulation obliges all packs to be recyclable by 2030, accelerating board uptake despite a 4-5 x unit-cost premium relative to polyolefins.

Energy-Price Volatility Squeezing Mill Margins

Electricity and gas form 10%-15% of mill outlays. U.S. natural gas averaged USD 3.30 per MMBtu in January 2025, far below the USD 9.50 August 2022 peak, yet European power prices remain elevated. Integrated producers with captive generation or renewables PPAs shield margins, whereas stand-alone recyclers exposed to spot rates face compressed spreads.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Drives Logistics Cost Savings

- Regional Single-Use-Plastic Bans

- Chronic Recycled-Fiber Supply Imbalance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Virgin fiber captured rising demand for liquid packaging board and solid bleached board, expanding at a forecast 5.93% CAGR as beverage and pharmaceutical buyers insist on brightness and tensile integrity. Billerud's FSC-certified Enviro-FBB has secured cosmetics contracts that emphasize opacity for shelf appeal. Sappi's 520,000-short-ton Somerset mill addition in 2024 widened U.S. supply of FDA-compliant substrates. Although recycled grades hold 57.82% of 2025 volume, elevated contamination and fiber fatigue hamper their suitability for high-brightness applications. DS Smith's commitment to 100% recycled fiber in containerboard underscores its cost edge, yet the cartonboard market size attached to virgin folds still outpaces recycled in profit per ton.

Recycled fiber maintains leadership in folding boxboard where unit economics dominate, and Graphic Packaging extracts 80% of input from recovered streams while sustaining brightness above 80 ISO through advanced de-inking. Nine Dragons Paper operates 160 Asian sites processing domestic and North American post-consumer bales. The cartonboard market share of recycled medium will stay resilient, but virgin capacity is likely to win incremental value in premium niches subject to stringent FDA or EU food-contact rules.

Solid bleached board (SBB) is projected to clock the fastest 6.72% CAGR to 2031, driven by luxury cosmetics and pharma packs that prize pure-white aesthetics. Sappi's Somerset expansion directly feeds this surge, supplying blister cards and food trays that demand rigidity and FDA clearance. Folding boxboard (FBB) retained a 38.13% slice of the 2025 cartonboard market size owing to its versatility across cereal, confectionery, and frozen meals. Stora Enso's FiberLight-based Performa Nova helped converters shave 10%-15% material use without sacrificing bend stiffness.

Liquid packaging board thrives on Elopak's Natural White Board that trims greenhouse gases by 14% per unit relative to PET bottles. White-lined chipboard services cost-sensitive food sectors, while food service board steps in for polystyrene clamshells under African and Asian plastic bans. Despite SBB's growth momentum, FBB will remain the volume backbone as converters exploit its fine balance of stiffness, runnability, and graphic punch.

The Cartonboard Market Report is Segmented by Material (Virgin Fiber, and Recycled Fiber), Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, and More), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Beverage, Food, Pharmaceutical and Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 43.62% of 2025 revenue, underpinned by China's 8% capacity additions and India's 24 million-t packaging consumption. Local mills benefit from government incentives for energy-efficient machines, and regional recyclers are expanding de-inking to offset import restrictions on old corrugated containers. Japan, South Korea, and Australia post recycling rates above 70%, enabling high substitution of recycled fiber in FBB grades, thereby bolstering the regional cartonboard market.

Africa is projected to expand fastest at 6.57% through 2031. Kenya's plastics ban catalyzes folding carton demand, and South Africa's USD 2.5 billion paper sector attracts Mondi and Sappi investments. Nigeria, Egypt, and Ethiopia record double-digit FMCG volume growth, stimulating need for secondary packs that withstand hot-chain logistics. Middle East markets such as Saudi Arabia and the United Arab Emirates will grow 5.8% as retail chains proliferate and e-commerce accelerates.

North America and Europe are consolidating capacity while funneling capital into digital presses and barrier-coat lines. International Paper removed 1 million t of legacy containerboard in 2024 and Packaging Corporation of America acquired Greif's unit for USD 1.8 billion to tighten supply. Europe's 72% paper recycling rate complements its Packaging Waste Regulation, which obliges recyclability by 2030. South America is buoyed by Klabin's 900,000-t PUMA II line due in 2027, positioning Brazil as an export platform to North Atlantic buyers.

- Asia Pulp & Paper Company Ltd.

- Mayr-Melnhof Karton AG

- Nine Dragons Paper (Holdings) Limited

- Smurfit WestRock

- Graphic Packaging Holding Company

- Stora Enso Oyj

- International Paper Company

- Metsa Board Corporation

- Pankaboard Oyj

- Klabin S.A.

- Oji Holdings Corporation

- Mondi plc

- Rengo Co., Ltd.

- Lee & Man Paper Manufacturing Ltd.

- Georgia-Pacific LLC

- Clearwater Paper Corporation

- Sappi Limited

- Holmen AB

- DS Smith plc

- Huhtamaki Oyj

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Corrugated-to-Cartonboard Substitution Surge

- 4.2.2 FMCG Pivot to Plastic-Free Primary Packaging

- 4.2.3 Lightweighting Drives Logistics Cost Savings

- 4.2.4 Regional Single-Use-Plastic Bans

- 4.2.5 High-Speed Digital Printing Unlocks SKU Proliferation

- 4.2.6 Luxury Goods' Demand for Premium Folding Cartons

- 4.3 Market Restraints

- 4.3.1 Energy-Price Volatility Squeezing Mill Margins

- 4.3.2 Chronic Recycled-Fiber Supply Imbalance

- 4.3.3 Capital-Intensive Barrier Coatings Compliance

- 4.3.4 Converters' Shift to Molded-Fiber Alternatives

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Investment Analysis

- 4.7 Industry Value / Supply-Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fiber

- 5.1.2 Recycled Fiber

- 5.2 By Product Grade

- 5.2.1 Solid Bleached Board

- 5.2.2 Solid Unbleached Board

- 5.2.3 Folding Boxboard

- 5.2.4 White-Lined Chipboard

- 5.2.5 Liquid Packaging Board

- 5.2.6 Food Service Board

- 5.3 By Packaging Format

- 5.3.1 Folding Cartons

- 5.3.2 Liquid Packaging

- 5.3.3 Sleeve and Tray

- 5.3.4 Other Packaging Format

- 5.4 By End-User Industry

- 5.4.1 Beverage

- 5.4.2 Food

- 5.4.3 Pharmaceutical and Healthcare

- 5.4.4 Cosmetics and Toiletries

- 5.4.5 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Asia Pulp & Paper Company Ltd.

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Nine Dragons Paper (Holdings) Limited

- 6.4.4 Smurfit WestRock

- 6.4.5 Graphic Packaging Holding Company

- 6.4.6 Stora Enso Oyj

- 6.4.7 International Paper Company

- 6.4.8 Metsa Board Corporation

- 6.4.9 Pankaboard Oyj

- 6.4.10 Klabin S.A.

- 6.4.11 Oji Holdings Corporation

- 6.4.12 Mondi plc

- 6.4.13 Rengo Co., Ltd.

- 6.4.14 Lee & Man Paper Manufacturing Ltd.

- 6.4.15 Georgia-Pacific LLC

- 6.4.16 Clearwater Paper Corporation

- 6.4.17 Sappi Limited

- 6.4.18 Holmen AB

- 6.4.19 DS Smith plc

- 6.4.20 Huhtamaki Oyj

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment