|

시장보고서

상품코드

1664195

전자전 시장(2025-2035년)Global Electronic Warfare Market 2025-2035 |

||||||

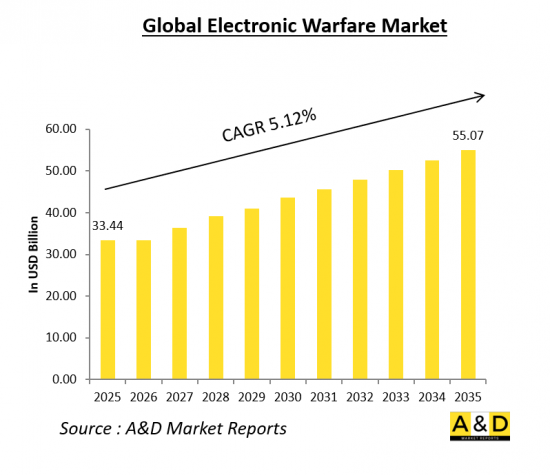

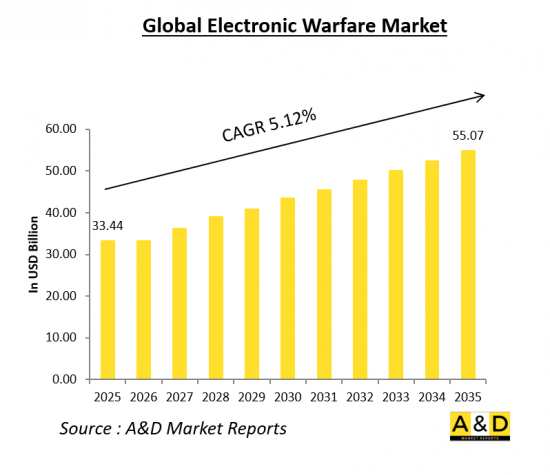

전 세계 전자전 시장 규모는 2025년에 334억 4,000만 달러, 2035년에는 550억 7,000만 달러에 달할 것으로 예상되며, 예측 기간 동안 연평균 5.12%의 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다.

전자전(EW) 시장은 현대 국방 전략의 핵심 요소로 부상하고 있으며, 세계 각국은 전자기 스펙트럼 작전에서 우위를 점하기 위해 첨단 역량에 대한 투자를 늘리고 있습니다. 전자전은 적의 통신, 레이더 및 기타 전자 시스템을 교란, 기만, 무력화하기 위해 고안된 광범위한 기술과 전술을 포괄합니다. 전자전은 전자 공격(EA), 전자 방어(EP), 전자 지원(ES)의 세 가지 주요 범주로 나뉘는데, EA는 교란과 기만과 같은 공격적 수단을 포함하며, EP는 전자적 위협으로부터 아군을 보호하는 데 중점을 두고, ES는 상황 인식을 높이기 위한 정보 수집을 포함합니다. 세계 분쟁이 진화함에 따라 정교한 EW 솔루션에 대한 수요가 증가하고 있습니다. 전자 및 사이버 위협의 확산은 네트워크 중심 전쟁에 대한 의존도 증가와 함께 전자전 시장의 성장을 촉진하고 있습니다. 방위 산업체 및 기술업체를 포함한 업계의 주요 업체들은 위협 탐지 및 대응 시간을 개선하기 위해 신호 처리, 인공지능(AI), 머신러닝(ML) 기능을 강화한 차세대 EW 시스템을 개발하고 있습니다.

AI와 ML은 실시간 데이터 분석과 자동화된 의사결정 과정을 가능하게함으로써 전자전 시스템에 혁명을 일으키고 있으며, AI와 ML은 위협 식별을 강화하고 신속한 대응을 가능하게함으로써 군사 작전에 대한 대응 시간을 단축하고 있습니다. 이러한 기술은 위협 식별을 강화하고 신속한 대응을 가능하게 하여 군사 작전의 대응 시간을 단축하고, AI 기반 알고리즘은 전자 신호를 보다 정확하게 감지하고 분류할 수 있어 방어군이 아군과 적군의 통신을 효과적으로 구분할 수 있게 해줍니다.

전자전 시스템에 사이버전을 통합하는 것은 또 다른 중요한 기술 동향입니다. 사이버와 전자전의 융합을 통해 군대는 적의 네트워크에 사이버 공격을 가하고 동시에 적의 레이더와 통신 시스템을 방해하거나 속일 수 있습니다. 이러한 시너지 효과는 전자 공격 작전의 효율성을 높이고 현대 전장에서 멀티 도메인 우위를 가져다 줄 것입니다.

또한, 전자부품의 소형화로 인해 무인항공기(UAV), 지상 차량, 함정, 우주 기반 자산 등 다양한 플랫폼에 배치할 수 있는 소형 휴대용 EW 시스템이 개발되고 있습니다. 이러한 시스템은 실시간 상황 인식을 제공하고 새로운 위협에 빠르게 적응할 수 있도록 지원합니다. 소프트웨어 정의 라디오(SDR)와 인지 EW 시스템의 등장은 적의 전술 변화에 따라 EW 자산을 재구성할 수 있도록함으로써 유연성과 복원력을 더욱 향상시킬 수 있습니다.

전자전 시장의 성장을 촉진하는 몇 가지 요인이 있습니다. 주요 촉진요인 중 하나는 현대 군사 작전에서 전자 시스템에 대한 의존도가 높아지고 있다는 점입니다. 군대의 네트워크 의존도가 높아짐에 따라 통신, 항법 및 감시 시스템을 전자적 위협으로부터 보호해야 할 필요성이 가장 중요해졌습니다. 이에 따라 고도의 전자 공격에 대응하고 작전 연속성을 보장할 수 있는 EW 솔루션에 대한 수요가 급증하고 있습니다.

다양한 지역의 지정학적 긴장과 분쟁이 고조되고 있는 것도 EW 시장 확대에 박차를 가하고 있습니다. 각국은 잠재적 적대 세력에 대응하기 위해 방어 능력을 적극적으로 강화하고 있으며, 이는 EW 기술에 대한 투자 확대로 이어지고 있습니다. 전 세계 군사 현대화 계획은 전투기, 함정, 미사일 방어 시스템 등 차세대 플랫폼에 첨단 EW 기능을 탑재하고 있습니다.

또한, 전자 재밍과 사이버 전쟁을 포함한 비대칭 전쟁 전술의 확산은 강력한 전자전 방어의 필요성을 강조하고 있습니다. 비국가 주체와 적대적 주체가 저비용 전자 교란 도구를 점점 더 많이 활용하고 있어, 군사 및 민간 인프라를 보호하기 위한 대응 수단의 개발이 필요합니다.

우주 기반 전자전 능력을 중시하는 경향이 강화되고 있는 것도 시장 촉진요인 중 하나입니다. 우주의 군사화로 인해 국방 기관은 적의 신호를 탐지, 감청, 무력화할 수 있는 위성 기반 전자전 시스템에 투자하고 있습니다. 우주 기반 전자정보(ELINT) 및 통신정보(COMINT) 자산은 세계 상황 인식과 전략적 억제력 강화에 중요한 역할을 하고 있습니다.

세계의 전자전 시장에 대해 조사했으며, 기술 동향, 시장 동향과 예측, 지역별, 국가별 동향, 시장 기회 등의 정보를 정리하여 전해드립니다.

목차

전자전 시장 보고서의 정의

전자전 시장 세분화

- 유형별

- 지역별

향후 10년간 전자전 시장 분석

세계의 전자전 시장 예측

전자전 시장 동향과 예측, 지역별

- 북미

- 유럽

- 중동

- 아시아태평양

- 남미

전자전 시장 국가별 분석

- 미국

- 캐나다

- 이탈리아

- 프랑스

- 독일

- 네덜란드

- 벨기에

- 스페인

- 스웨덴

- 그리스

- 호주

- 남아프리카공화국

- 인도

- 중국

- 러시아

- 한국

- 일본

- 말레이시아

- 싱가포르

- 브라질

전자전 시장 기회 매트릭스

결론

조사 회사에 대해

ksm 25.03.13The global electronic warfare market is valued at an estimated USD 33.44 billion in 2025 and is projected to reach USD 55.07 billion by 2035, growing at a Compound Annual Growth Rate (CAGR) of 5.12% over the forecast period.

Introduction to Electronic Warfare Market

The electronic warfare (EW) market has emerged as a critical component of modern defense strategies, with nations worldwide increasingly investing in advanced capabilities to gain superiority in electromagnetic spectrum operations. Electronic warfare encompasses a broad range of technologies and tactics designed to disrupt, deceive, or disable enemy communications, radar, and other electronic systems. It is divided into three primary categories: electronic attack (EA), electronic protection (EP), and electronic support (ES). EA includes offensive measures such as jamming and deception, EP focuses on safeguarding friendly forces from electronic threats, and ES involves intelligence gathering to enhance situational awareness. As global conflicts evolve, the demand for sophisticated EW solutions is rising. The proliferation of electronic and cyber threats, coupled with the increasing reliance on network-centric warfare, is driving the growth of the electronic warfare market. Key players in the industry, including defense contractors and technology firms, are developing next-generation EW systems with enhanced capabilities in signal processing, artificial intelligence (AI), and machine learning (ML) to improve threat detection and response times.

Technology Impact in Electronic Warfare Market

Advancements in technology are significantly transforming the landscape of electronic warfare. AI and ML are revolutionizing EW systems by enabling real-time data analysis and automated decision-making processes. These technologies enhance threat identification and enable rapid countermeasures, reducing the response time for military operations. AI-driven algorithms can detect and classify electronic signals more accurately, allowing defense forces to differentiate between friendly and hostile communications effectively.

The integration of cyber warfare into electronic warfare systems is another key technological trend. Cyber-EW fusion enables military forces to launch cyber-attacks on adversary networks while simultaneously jamming or deceiving their radar and communication systems. This synergy enhances the effectiveness of electronic attack operations and provides a multi-domain advantage in modern battlefields.

Additionally, the miniaturization of electronic components has led to the development of compact and portable EW systems that can be deployed on a variety of platforms, including unmanned aerial vehicles (UAVs), ground vehicles, naval vessels, and space-based assets. These systems provide real-time situational awareness and enable rapid adaptation to emerging threats. The advent of software-defined radios (SDRs) and cognitive EW systems further improves flexibility and resilience by allowing forces to reconfigure EW assets in response to changing enemy tactics.

Key Drivers in Electronic Warfare Market

Several factors are driving the growth of the electronic warfare market. One of the primary drivers is the increasing reliance on electronic systems in modern military operations. As armed forces become more network-dependent, the need to protect communication, navigation, and surveillance systems from electronic threats becomes paramount. This has led to a surge in demand for EW solutions that can counter sophisticated electronic attacks and ensure operational continuity.

The rising geopolitical tensions and conflicts across various regions are also fueling the expansion of the EW market. Nations are actively strengthening their defense capabilities to counter potential adversaries, leading to higher investments in EW technologies. Military modernization programs worldwide are incorporating advanced EW capabilities into next-generation platforms, including fighter jets, naval vessels, and missile defense systems.

Furthermore, the proliferation of asymmetric warfare tactics, including electronic jamming and cyber warfare, has underscored the need for robust EW defenses. Non-state actors and hostile entities are increasingly leveraging low-cost electronic disruption tools, necessitating the development of countermeasures to safeguard military and civilian infrastructure.

The growing emphasis on space-based electronic warfare capabilities is another major market driver. The militarization of space has prompted defense agencies to invest in satellite-based EW systems that can detect, intercept, and neutralize adversary signals. Space-based electronic intelligence (ELINT) and communications intelligence (COMINT) assets are playing a crucial role in enhancing global situational awareness and strategic deterrence.

Regional Trends in Electronic Warfare Market

The electronic warfare market exhibits significant regional variations, with major defense-spending nations leading in technological advancements and deployment.

In North America, the United States remains the dominant player in the EW market, driven by extensive defense budgets and continuous technological innovation. The U.S. Department of Defense (DoD) is heavily investing in next-generation EW capabilities through programs such as the Army's Electronic Warfare Planning and Management Tool (EWPMT) and the Navy's Surface Electronic Warfare Improvement Program (SEWIP). The emphasis on countering peer adversaries, such as China and Russia, has led to increased funding for EW research and development.

Europe is also witnessing substantial growth in the EW market, with NATO member states enhancing their EW capabilities to address emerging threats. Countries like the United Kingdom, Germany, and France are integrating EW solutions into their defense strategies to counter potential electronic threats from state and non-state actors. The European Defence Agency (EDA) is actively supporting collaborative EW projects, fostering innovation across the region.

The Asia-Pacific region is experiencing a rapid expansion in the EW sector, driven by rising defense expenditures in China, India, Japan, and South Korea. China is aggressively developing advanced EW capabilities as part of its broader military modernization strategy, including space-based EW assets and cyber-electronic warfare integration. India is also strengthening its EW infrastructure through indigenous programs such as the Defence Research and Development Organisation's (DRDO) Samyukta electronic warfare system.

In the Middle East, increasing geopolitical instability and military conflicts are driving investments in electronic warfare technologies. Countries like Israel, Saudi Arabia, and the United Arab Emirates (UAE) are procuring advanced EW systems to enhance their defense capabilities. Israel, in particular, is a global leader in EW innovation, with companies like Elbit Systems and Rafael Advanced Defense Systems developing cutting-edge electronic warfare solutions.

Africa and Latin America are gradually adopting EW technologies, though at a slower pace compared to other regions. These regions are focusing on strengthening border security and countering asymmetric threats, leading to increased interest in electronic surveillance and jamming systems.

Key Electronic Warfare Programs

V2X Inc. has secured a $21 million firm-fixed-price contract to continue supporting the sustainment of critical avionics and electronic warfare systems for the U.S. Air Force. This contract covers the repair and maintenance of AN/ALQ-172 and AN/ALQ-161 components, ensuring the operational readiness of the B-52 Stratofortress, B-1B, and C-130 aircraft. As global adversaries enhance their electronic warfare capabilities, V2X's work helps U.S. aircraft remain protected in contested environments. The AN/ALQ-172 self-protection RF subsystem provides multi-threat countermeasures against pulse, continuous wave, pulse Doppler, and monopulse radar threats. Likewise, the AN/ALQ-161 system has undergone continuous upgrades since its initial deployment in the 1980s, improving its ability to detect and counter evolving electronic threats. With its expertise in sustaining and enhancing complex avionics, V2X plays a vital role in extending the lifespan and operational effectiveness of these legacy aircraft and their mission-critical systems.

The Ministry of Defence signed a contract with Bharat Electronics Limited (BEL), Hyderabad, for the procurement of two Integrated Electronic Warfare Systems under 'Project Himshakti' at a total cost of approximately ₹3,000 crore. The project falls under the Buy {Indian - IDMM (Indigenously Designed, Developed, and Manufactured)} category and incorporates advanced and specialized technologies. 'Project Himshakti' is expected to boost the participation of Indian electronics and related industries, including MSMEs that serve as sub-vendors to BEL. It will also create approximately three lakh man-days of employment over the next two years. This initiative represents a significant step in strengthening indigenous defense capabilities, aligning with the government's Make-in-India initiative and furthering the vision of 'Aatmanirbhar Bharat' (self-reliant India).

Table of Contents

Electronic Warfare Market Report Definition

Electronic Warfare Market Segmentation

By Type

By Region

Electronic Warfare Market Analysis for next 10 Years

The 10-year electronic warfare market analysis would give a detailed overview of electronic warfare market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Electronic Warfare Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Electronic Warfare Market Forecast

The 10-year electronic warfare market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Electronic Warfare Market Trends & Forecast

The regional electronic warfare market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Electronic Warfare Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Electronic Warfare Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Electronic Warfare Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports