|

시장보고서

상품코드

1680166

방위용 육상 플랫폼 엔진 시장(2025-2035년)Global Defense Land Platforms Engine Market 2025-2035 |

||||||

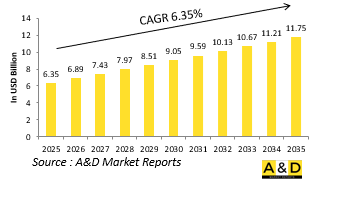

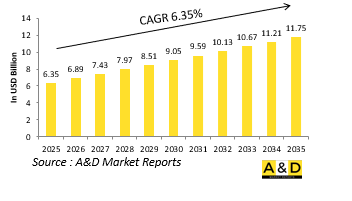

전 세계 방위용 육상 플랫폼 엔진 시장 규모는 2025년에 63억 5,000만 달러에서 2035년에는 117억 5,000만 달러로 성장할 것으로 예상되며, 예측 기간인 2025년부터 2035년까지 6.35%의 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다.

세계 방위용 육상 플랫폼 엔진 시장은 전투, 병참, 정찰, 정찰, 인력 수송에 사용되는 다양한 장갑 및 비장갑 지상 차량의 동력원으로서 군사 작전에서 중요한 역할을 담당하고 있습니다. 지상전이 여전히 군사 전략의 핵심이기 때문에 강력하고 신뢰할 수 있으며 연료 효율이 높은 엔진의 필요성이 크게 증가하고 있습니다. 주전차, 보병전차, 자주포, 전술 수송 트럭과 같은 방위용 육상 플랫폼은 사막 환경부터 극한의 추위까지 가혹한 조건에서도 작동할 수 있는 엔진이 필요합니다. 이러한 엔진은 장시간 임무를 지원하고 전투 시나리오에서 작전 효과를 보장하기 위해 높은 토크, 향상된 기동성, 우수한 연료 효율을 제공해야 합니다. 지속적인 군사 현대화 노력, 지정학적 긴장, 새로운 위협에 따라 육상 방어 플랫폼의 첨단 추진 기술에 대한 투자가 전 세계적으로 증가하고 있습니다. 엔진 제조업체와 방위 산업체들은 성능 향상, 유지보수 요구사항 감소, 하이브리드 전기 및 대체 연료에 대한 적응성 향상을 위한 차세대 파워트레인에 집중하고 있습니다.

기술, 출력 효율성, 내구성, 디지털 통합의 상당한 발전으로 방위용 육상 플랫폼 엔진의 진화를 주도하고 있습니다. 하이브리드 전기 추진으로의 전환은 연료 소비 감소, 열 시그니처 감소, 스텔스 능력 강화의 필요성으로 인해 가장 혁신적인 트렌드 중 하나입니다. 하이브리드 전기 추진 시스템 및 완전 전기 추진 시스템은 장갑차, 특히 정찰 및 지원 임무용으로 검토되고 있습니다. 첨단 디젤 엔진 기술은 터보 과급, 커먼레일 직분사, 배기 후처리 시스템의 개선으로 연비를 개선하고 배기가스를 감소시키며 여전히 시장을 지배하고 있습니다. 모듈식 엔진 설계를 채택하여 업그레이드가 용이하고 다양한 차량 플랫폼에 적응할 수 있는 모듈식 엔진 설계를 채택했습니다. 디지털 엔진 관리 시스템은 실시간 진단과 인공지능(AI) 기반 성능 최적화를 통한 예지보전 기능을 통합한 디지털 엔진 관리 시스템도 표준이 되어가고 있습니다. 적층 가공은 엔진 부품 생산에 혁명을 일으켜 경량화 설계, 신속한 프로토타이핑, 엔진의 수명과 성능을 향상시킬 수 있는 탄력적인 소재를 가능하게 하고 있습니다. 또한, 미래 전투 차량에 지속가능하고 물류 효율이 높은 추진 솔루션을 원하는 군부에서는 방위용 육상 플랫폼용 수소 연료전지 기술에 대한 연구도 진행 중입니다.

군사 현대화 프로그램을 필두로 몇 가지 주요 촉진요인이 방위용 육상 플랫폼 엔진 시장의 성장을 주도하고 있습니다. 전 세계 각국은 진화하는 전장의 요구 사항을 충족하기 위해 더 강력하고 효율적인 엔진을 장착한 장갑차 부대를 업그레이드하고 있습니다. 도시전, 비대칭 위협, 다중 도메인 작전을 특징으로 하는 지상전투의 복잡성으로 인해 더 빠르고 기동성이 뛰어나며 회복력이 뛰어난 고성능 추진 시스템 개발이 요구되고 있습니다. 자율 및 원격 조종 지상 차량에 대한 수요 증가도 엔진 기술 혁신을 촉진하는 주요 요인 중 하나입니다. 전략적인 기동성은 방위군에게 중요한 고려사항이 되고 있으며, 다양한 지형에서의 전개성을 높이는 경량 및 고출력 엔진이 중요시되고 있습니다. 장기화되는 분쟁에서 물류 및 공급망의 취약성으로 인해 연료 의존도를 낮추는 것이 중요해지면서 연료 효율성 향상도 중요한 동력이 되고 있습니다. 또한, 하이브리드 전기 및 대체 연료 기술의 통합은 광범위한 군의 지속가능성 이니셔티브에 부합하며, 미래의 육상 플랫폼이 작전적으로 효과적이면서도 환경 친화적일 수 있도록 보장합니다.

방위용 육상 플랫폼 엔진 시장의 지역별 동향은 국방 우선순위, 산업 역량, 조달 전략의 차이를 반영합니다. 북미, 특히 미국은 주요 국방 계획이 차세대 엔진 기술에 대한 수요를 주도하고 있기 때문에 여전히 시장을 지배하고 있습니다. 미 육군의 차세대 전투차량(NGCV) 프로그램은 브래들리 전투차량과 같은 노후화된 장갑 플랫폼을 대체하기 위한 것으로, 기동성과 생존성을 향상시키는 혁신적인 추진 시스템을 요구하고 있습니다. 가스 터빈 엔진을 탑재한 에이브럼스 주력 전차는 연료 효율과 전장 내구성을 향상시키기 위해 업그레이드가 진행되고 있으며, General Dynamics, Cummins, Honeywell을 포함한 주요 방산업체들은 육상 플랫폼 엔진의 발전을 주도하고 있습니다. 하이브리드 전기 파워트레인 및 AI 기반 진단을 통합하여 차량 성능을 향상시키고 있습니다. 캐나다도 장갑차 업그레이드와 향후 인수에 첨단 파워트레인 솔루션의 통합에 중점을 두고 이 시장에서 중요한 역할을 하고 있습니다.

세계의 방위용 육상 플랫폼 엔진 시장에 대해 조사했으며, 향후 10년간의 분야별 시장 예측, 기술 동향, 기회 분석, 기업 프로파일, 국가별 데이터 등의 정보를 정리하여 전해드립니다.

목차

방위용 육상 플랫폼 엔진 시장 보고서의 정의

방위용 육상 플랫폼 엔진 시장 세분화

- HP별

- 플랫폼별

- 지역별

향후 10년간 방위용 육상 플랫폼 엔진 시장 분석

방위용 육상 플랫폼 엔진 시장의 시장 기술

세계의 방위용 육상 플랫폼 엔진 시장 예측

방위용 육상 플랫폼 엔진 시장 동향과 예측, 지역별

- 북미

- 성장 촉진요인, 억제요인, 과제

- PEST

- 시장 예측과 시나리오 분석

- 주요 기업

- 공급업체 계층 상황

- 기업 벤치마크

- 유럽

- 중동

- 아시아태평양

- 남미

방위용 육상 플랫폼 엔진 시장 국가별 분석

- 미국

- 방위 프로그램

- 최신 뉴스

- 특허

- 이 시장의 현재 기술 성숙도

- 시장 예측과 시나리오 분석

- 캐나다

- 이탈리아

- 프랑스

- 독일

- 네덜란드

- 벨기에

- 스페인

- 스웨덴

- 그리스

- 호주

- 남아프리카공화국

- 인도

- 중국

- 러시아

- 한국

- 일본

- 말레이시아

- 싱가포르

- 브라질

방위용 육상 플랫폼 엔진 시장 기회 매트릭스

방위용 육상 플랫폼 엔진 시장 보고서에 관한 전문가의 의견

결론

항공·방위 시장 보고서에 대해

ksm 25.03.25The Global defense land platforms engine market is estimated at USD 6.35 billion in 2025, projected to grow to USD 11.75 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 6.35% over the forecast period 2025-2035.

Introduction to Defense Land Platforms Engine Market:

The global defense land platforms engine market plays a vital role in military operations, powering a range of armored and unarmored ground vehicles used for combat, logistics, reconnaissance, and personnel transport. As land-based warfare remains a cornerstone of military strategy, the need for powerful, reliable, and fuel-efficient engines has grown significantly. Defense land platforms, including main battle tanks, infantry fighting vehicles, self-propelled artillery, and tactical transport trucks, require engines that can operate in extreme conditions, from desert environments to arctic terrains. These engines must deliver high torque, enhanced mobility, and superior fuel efficiency to support extended missions and ensure operational effectiveness in combat scenarios. With ongoing military modernization efforts, geopolitical tensions, and emerging threats, investments in advanced propulsion technologies for land-based defense platforms are increasing worldwide. Engine manufacturers and defense contractors are focusing on next-generation powertrains that offer improved performance, reduced maintenance requirements, and greater adaptability for hybrid-electric and alternative fuel applications.

Technology Impact in Defense Land Platforms Engine Market:

Technology is shaping the evolution of defense land platform engines, with significant advancements in power efficiency, durability, and digital integration. The shift towards hybrid-electric propulsion is one of the most transformative trends, driven by the need for reduced fuel consumption, lower thermal signatures, and enhanced stealth capabilities. Hybrid-electric and fully electric propulsion systems are being explored for armored vehicles, particularly for reconnaissance and support roles, where silent operations provide a tactical advantage. Advanced diesel engine technologies remain dominant in the market, with improvements in turbocharging, common rail direct injection, and exhaust after-treatment systems enhancing fuel efficiency and reducing emissions. The use of modular engine designs has gained traction, allowing for easier upgrades and adaptability across different vehicle platforms. Digital engine management systems are also becoming standard, incorporating predictive maintenance capabilities through real-time diagnostics and artificial intelligence (AI)-driven performance optimization. Additive manufacturing is revolutionizing the production of engine components, enabling lightweight designs, faster prototyping, and more resilient materials that enhance engine longevity and performance. Additionally, research into hydrogen fuel cell technology for defense land platforms is ongoing, as military forces seek sustainable and logistically efficient propulsion solutions for future combat vehicles.

Key Drivers in Defense Land Platforms Engine Market:

Several key drivers are fueling the growth of the defense land platforms engine market, with military modernization programs at the forefront. Nations worldwide are upgrading their armored vehicle fleets with more powerful and efficient engines to meet evolving battlefield requirements. The increasing complexity of ground combat, characterized by urban warfare, asymmetric threats, and multi-domain operations, has necessitated the development of high-performance propulsion systems that offer greater speed, maneuverability, and resilience. The rise in demand for autonomous and remotely operated ground vehicles is another major factor driving engine innovation, as these platforms require power solutions that maximize endurance and operational flexibility. Strategic mobility has become a critical consideration for defense forces, leading to a greater emphasis on lightweight yet high-output engines that enhance deployability across diverse terrains. The push for improved fuel efficiency is also a significant driver, as logistics and supply chain vulnerabilities in extended conflicts highlight the importance of reducing fuel dependence. Additionally, the integration of hybrid-electric and alternative fuel technologies aligns with broader military sustainability initiatives, ensuring that future land-based platforms remain both operationally effective and environmentally conscious.

Regional Trends in Defense Land Platforms Engine Market:

Regional trends in the defense land platforms engine market reflect varying defense priorities, industrial capabilities, and procurement strategies. North America, particularly the United States, remains a dominant force in the market, with major defense programs driving demand for next-generation engine technologies. The U.S. Army's Next-Generation Combat Vehicle (NGCV) program, aimed at replacing aging armored platforms such as the Bradley Fighting Vehicle, is pushing for innovative propulsion systems that enhance mobility and survivability. The Abrams Main Battle Tank, powered by a gas turbine engine, is undergoing upgrades to improve fuel efficiency and battlefield endurance. Major defense contractors, including General Dynamics, Cummins, and Honeywell, are leading advancements in land platform engines, incorporating hybrid-electric powertrains and AI-driven diagnostics to enhance vehicle performance. Canada also plays a role in the market, focusing on upgrading its armored vehicle fleets and integrating advanced powertrain solutions into future acquisitions.

In Europe, the defense land platforms engine market is characterized by multinational collaboration and a strong emphasis on indigenous defense manufacturing. Countries such as Germany, France, and the United Kingdom are at the forefront of armored vehicle engine development, with companies like MTU Friedrichshafen, Renault Trucks Defense, and Rolls-Royce contributing to cutting-edge propulsion technologies. The European Main Battle Tank (EMBT) program, a joint effort between France's Nexter and Germany's KMW, is driving research into next-generation tank engines with improved efficiency and modularity. The UK's Challenger 3 program, which focuses on upgrading the British Army's main battle tanks, includes enhancements to powertrain systems for better speed and fuel economy. Europe's emphasis on interoperability within NATO forces has also led to standardization efforts in engine technologies, ensuring seamless integration across allied armored vehicle fleets.

The Asia-Pacific region is experiencing significant growth in the defense land platforms engine market, fueled by increasing military expenditures, regional security concerns, and indigenous defense production initiatives. China has made substantial investments in developing advanced land-based propulsion systems, with its Type 99 main battle tank featuring high-performance diesel engines designed for enhanced speed and endurance. The country is also exploring hybrid-electric technologies for future armored vehicle platforms. India's defense industry is making strides in indigenous tank engine development, with the Defence Research and Development Organisation (DRDO) working on next-generation powertrains for the Arjun main battle tank and other armored vehicles. Japan and South Korea are similarly advancing their land platform capabilities, with South Korea's K2 Black Panther tank incorporating a powerful and efficient engine system that enhances battlefield mobility. The region's focus on self-reliance in defense manufacturing is driving investments in domestic engine production capabilities, reducing reliance on foreign suppliers.

The Middle East presents a strong market for defense land platform engines, with nations such as Saudi Arabia, the United Arab Emirates, and Israel investing heavily in armored vehicle modernization. These countries rely on a mix of Western and locally produced defense technologies, with ongoing procurement of advanced main battle tanks, infantry fighting vehicles, and tactical transport platforms. Harsh desert environments necessitate engines that can withstand extreme temperatures and operate efficiently under high dust and sand exposure. The region's defense programs emphasize both new acquisitions and engine upgrades for existing fleets, ensuring that military ground forces maintain operational readiness and strategic mobility.

Africa's defense land platforms engine market is relatively smaller but growing steadily as regional security challenges drive military procurement and modernization efforts. Many African nations operate legacy armored vehicles that require engine upgrades or replacements to remain viable in contemporary combat scenarios. Countries such as Egypt, Algeria, and South Africa are leading players in the region's defense sector, investing in both Western and Russian-made land platforms. Additionally, the demand for light tactical vehicles with high-performance engines is increasing due to counterterrorism operations and border security initiatives. Maintenance, repair, and overhaul (MRO) services are crucial in Africa, as many defense forces seek cost-effective solutions to extend the lifespan of their existing vehicle fleets.

Key Defense Land Platforms Engine Program:

Russia will supply new engines for the Indian Army's T-72 Soviet-era battle tanks under a $248-million contract awarded by the Indian Ministry of Defence to Rosoboronexport. As part of the agreement, the Russian state-owned defense exporter will deliver modern 1,000-horsepower engines to upgrade India's aging T-72 Ural main battle tanks. The Indian military currently operates around 2,500 T-72 tanks, which have been equipped with legacy 780-horsepower engines since their production began in the 1970s.

The Australian Department of Defence has signed a contract with Penske Australia to provide local industry support for diesel engine sustainment, ensuring the Australian Defence Force (ADF) remains operationally ready for deployment whenever required. Acting Deputy Secretary for Naval Shipbuilding and Sustainment, Rear Admiral Wendy Malcolm, stated that the five-year, $190 million agreement builds on the benefits of the previous contract while introducing greater cost transparency, improved risk management, and enhanced opportunities to strengthen sovereign capability.

Table of Contents

Defense Land Platform Engines Market Report Definition

Defense Land Platform Engines Market Segmentation

By HP

By Platform

By Region

Defense Land Platform Engines Market Analysis for next 10 Years

The 10-year defense land platform engines market analysis would give a detailed overview of defense land platform engines market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Land Platform Engines Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Land Platform Engines Market Forecast

The 10-year defense land platform engines market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Land Platform Engines Market Trends & Forecast

The regional defense land platform engines market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Land Platform Engines Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Land Platform Engines Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Land Platform Engines Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports