|

시장보고서

상품코드

1904988

군용 항공기 정비(MR0) 플랫폼 시장(2026-2035년)Global Defense MRO - Air Platforms Market 2026-2036 |

||||||

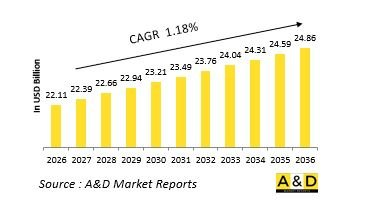

세계의 군용 항공기 정비(MR0) 플랫폼 시장 규모는 2026년 221억 1,000만 달러로 평가되었고, 2026-2036년의 예측 기간 동안 CAGR은 1.18%를 나타낼 것으로 보이며, 2036년에는 248억 6,000만 달러에 이를 것으로 전망됩니다.

군용 항공기 정비(MR0) 플랫폼 개요 :

세계의 군용 항공기 정비(MR0) 플랫폼(유지보수, 수리 및 정비) 시장은 군사 항공기 함대의 운용 가용성, 안전성 및 수명을 보장하는 군사 준비 태세의 핵심 축입니다. 항공 플랫폼에는 전투기, 수송기, 공중 조기경보 시스템, 공중 급유기, 특수 임무 항공기 및 군용 헬리콥터가 포함됩니다. 조달 중심 시장과 달리 국방 항공 MRO는 수명 주기 중심이며, 정기 정비, 중정비(정비소 수준), 구조적 수명 연장, 엔진 정비, 항공전자 장비 업그레이드 및 현대화 프로그램을 포괄합니다.

지정학적 긴장 고조, 공중 작전 빈도 증가, 다국적 훈련 확대는 항공기 운용률을 더욱 가속화하여 정비 주기를 단축시키고 있습니다. 동시에 네트워크 중심전(network-centric warfare)과 센서 집약형 플랫폼으로의 전환은 MRO 범위를 기계적 유지보수를 넘어 소프트웨어 유지관리, 사이버 보안, 전자 시스템 정비까지 확장시켰습니다. 그 결과 군용 항공기 정비(MR0) 플랫폼 시장은 비용 중심에서 공중 전력 우위를 위한 전략적 지원 체계로 진화하고 있습니다.

지정학적 긴장 증가, 항공 작전의 빈도 증가, 다국적 연습의 확대에 의해 항공기의 가동률이 더욱 향상되어, 유지관리 사이클의 단축화가 진행되고 있습니다. 동시에 네트워크 중심전과 센서 집약형 플랫폼으로의 전환에 따라 MRO의 범위는 기계적 유지보수에서 소프트웨어 유지, 사이버 보안, 전자 시스템 유지보수로 확대되고 있습니다. 그 결과, 군용 항공기 정비(MR0) 플랫폼 시장은 비용 센터에서 항공 전력 우위를 지원하는 전략적 기반으로 진화하고 있습니다.

군용 항공기 정비(MR0) 플랫폼 시장의 기술적 영향 :

기술은 군용 항공기 정비(MR0) 플랫폼 환경을 근본적으로 재편하며 효율성, 예측 가능성 및 항공기 가용성을 향상시키고 있습니다. 가장 중요한 발전 중 하나는 센서, 건강 및 사용 모니터링 시스템(HUMS), 데이터 분석을 통해 가능해진 예측 정비의 도입입니다. 항공기에서 생성된 데이터를 통해 정비 담당자는 잠재적 고장이 발생하기 전에 이를 식별할 수 있어 예정되지 않은 가동 중단 시간을 줄이고 예비 부품 재고를 최적화할 수 있습니다.

디지털 트윈은 운영 시나리오 전반에 걸친 항공기 성능 및 부품 열화 시뮬레이션에 점점 더 활용되고 있습니다. 이러한 가상 복제본은 특히 노후화된 전투기 및 수송기 함대를 대상으로 상태 기반 정비, 구조적 수명 평가, 업그레이드 계획 수립을 지원합니다. 초음파 검사, 열화상 촬영, 방사선 촬영 기술과 같은 첨단 비파괴 검사(NDT) 기술은 분해 요구 사항을 최소화하면서 결함 탐지 능력을 향상시켰습니다.

적층 제조는 또 다른 혁신 기술로, 작전 기지 내 또는 인근에서 소량 생산되거나 단종된 예비 부품을 신속하게 생산할 수 있게 합니다. 이 능력은 특히 구형 플랫폼의 경우 리드 타임을 크게 단축하고 긴 글로벌 공급망에 대한 의존도를 낮춥니다. 또한 증강 현실(AR) 및 가상 현실(VR) 도구는 정비 교육, 원격 기술 지원 및 복잡한 수리 절차에 채택되고 있습니다.

현대 군용 항공기가 임무 시스템, 항공 전자 소프트웨어, 전자전 장비에 크게 의존함에 따라 소프트웨어 유지보수는 핵심 MRO 기능으로 부상했습니다. 사이버 복원력 유지보수 관행과 안전한 소프트웨어 업데이트 메커니즘은 항공 MRO 운영의 필수 요소가 되고 있습니다. 이러한 기술들은 종합적으로 군용 항공기 정비(MR0) 플랫폼을 데이터 기반의 디지털화 된 생태계로 전환시키고 있습니다.

이 보고서는 세계의 군용 항공기 정비(MR0) 플랫폼 시장을 조사했으며, 시장 배경, 시장 영향요인 분석, 시장 규모 추이와 예측, 각종 구분, 지역별 상세 분석 등을 정리했습니다.

목차

군용 항공기 정비(MR0) 플랫폼 시장 : 보고서 정의

군용 항공기 정비(MR0) 플랫폼 시장 : 세분화

지역별

컴포넌트별

항공기 유형별

군용 항공기 정비(MR0) 플랫폼 시장 : 분석

군용 항공기 정비(MR0) 플랫폼 시장 : 기술

군용 항공기 정비(MR0) 플랫폼 시장 : 예측

군용 항공기 정비(MR0) 플랫폼 시장 : 지역별 동향 및 예측

조사 내용 : 시장 동향, 촉진요인, 억제요인, 과제, PEST 분석, 시장 예측, 시나리오 분석, 주요 기업프로파일, 공급자 상황, 기업 벤치마킹, 지역별 시장 예측 및 시나리오 분석, 주요 기업프로파일링 등을 정리했습니다.

북미

촉진요인, 억제요인, 과제

PEST

시장 예측 및 시나리오 분석

주요 기업

공급자 계층 구조 상태

기업 벤치마킹

유럽

중동

아시아태평양

남미

군용 항공기 정비(MR0) 플랫폼 시장 : 국가별 분석

미국

방위 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

시장 예측 및 시나리오 분석

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

군용 항공기 정비(MR0) 플랫폼 시장 : 기회 매트릭스

군용 항공기 정비(MR0) 플랫폼 시장 : 전문가 의견

결론

항공 및 방위 시장 보고서에 대해서

HBR 26.01.20The Global MRO - Air Platforms market is estimated at USD 22.11 billion in 2026, projected to grow to USD 24.86 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 1.18% over the forecast period 2026-2036.

Introduction to MRO - Air Platforms Market:

The Global Defense Maintenance, Repair, and Overhaul (MRO) - Air Platforms market is a critical pillar of military readiness, ensuring the operational availability, safety, and longevity of military aircraft fleets. Air platforms include fighter jets, transport aircraft, airborne early warning systems, aerial refueling tankers, special mission aircraft, and military helicopters. Unlike procurement-driven markets, defense air MRO is lifecycle-oriented, spanning routine maintenance, heavy depot-level overhauls, structural life extension, engine servicing, avionics upgrades, and modernization programs.

As global air forces operate increasingly complex and aging fleets, MRO activities have become strategically important. Many nations continue to fly legacy aircraft well beyond their original design life due to budget constraints, delayed next-generation programs, or force structure requirements. This has elevated the role of advanced MRO solutions in sustaining fleet performance while meeting modern mission demands. The market is characterized by a mix of government-owned depots, original equipment manufacturers (OEMs), and private MRO providers operating under long-term performance-based logistics (PBL) contracts.

Geopolitical tensions, increased air operations tempo, and expanding multinational exercises have further intensified aircraft utilization rates, driving higher maintenance cycles. At the same time, the shift toward network-centric warfare and sensor-heavy platforms has expanded MRO scope beyond mechanical upkeep to include software sustainment, cybersecurity, and electronic systems maintenance. As a result, the defense air MRO market is evolving from a cost center into a strategic enabler of air power dominance.

Technology Impact in MRO - Air Platforms Market:

Technology is fundamentally reshaping the defense air platforms MRO landscape, improving efficiency, predictability, and aircraft availability. One of the most significant developments is the adoption of predictive maintenance enabled by sensors, health and usage monitoring systems (HUMS), and data analytics. Aircraft-generated data allows maintainers to identify potential failures before they occur, reducing unscheduled downtime and optimizing spare parts inventory.

Digital twins are increasingly used to simulate aircraft performance and component degradation across operational scenarios. These virtual replicas support condition-based maintenance, structural life assessment, and upgrade planning, particularly for aging fighter and transport fleets. Advanced non-destructive testing (NDT) technologies-such as ultrasonic inspection, thermography, and radiographic techniques-have improved fault detection while minimizing disassembly requirements.

Additive manufacturing is another disruptive technology, enabling rapid production of low-volume or obsolete spare parts at or near operational bases. This capability significantly reduces lead times and dependence on long global supply chains, especially for legacy platforms. Additionally, augmented reality (AR) and virtual reality (VR) tools are being adopted for maintenance training, remote technical assistance, and complex repair procedures.

Software sustainment has emerged as a critical MRO function as modern military aircraft rely heavily on mission systems, avionics software, and electronic warfare suites. Cyber-resilient maintenance practices and secure software update mechanisms are becoming integral to air MRO operations. Collectively, these technologies are transforming defense air MRO into a data-driven, digitally enabled ecosystem.

Key Drivers in MRO - Air Platforms Market:

A primary driver of the defense air platforms MRO market is the aging global military aircraft fleet. Many air forces operate aircraft that are 30-40 years old, requiring extensive structural reinforcement, avionics modernization, and engine refurbishment to remain operationally relevant. Life extension programs have become more cost-effective alternatives to immediate fleet replacement.

Rising operational tempo is another key factor. Increased air patrols, intelligence-surveillance-reconnaissance (ISR) missions, and expeditionary deployments accelerate wear and tear, leading to higher maintenance demand. The growing emphasis on readiness and availability metrics has pushed defense ministries toward outcome-based MRO contracts that prioritize aircraft mission-capable rates.

Budget optimization also drives outsourcing trends. Governments increasingly partner with OEMs and private MRO providers to leverage specialized expertise, reduce lifecycle costs, and improve turnaround times. OEM-led sustainment models are particularly prominent for advanced platforms where proprietary technologies and software dominate. Additionally, fleet modernization programs stimulate MRO demand by integrating new sensors, weapons, and communication systems into existing aircraft. Regulatory compliance, airworthiness mandates, and safety upgrades further sustain long-term MRO spending. Together, these drivers ensure stable, recurring demand for defense air platform MRO across global markets.

Regional Trends in MRO - Air Platforms Market:

North America dominates the defense air MRO market, driven by the world's largest military aviation fleet and significant sustainment budgets. The region emphasizes advanced analytics, performance-based logistics, and public-private partnerships, with strong OEM involvement in sustainment activities.

Europe shows robust demand due to multinational aircraft programs, legacy fleet sustainment, and increased defense spending. Collaborative MRO frameworks and regional sustainment hubs are gaining traction, particularly for fighter and transport aircraft. The Asia-Pacific region is experiencing the fastest growth, fueled by expanding air forces, high aircraft utilization, and increasing focus on indigenous MRO capabilities. Countries are investing in domestic depot-level maintenance to reduce foreign dependence and enhance operational autonomy. In the Middle East, harsh operating environments drive intensive maintenance requirements, while strong defense budgets support advanced MRO infrastructure. Latin America and Africa focus primarily on sustaining aging fleets, with gradual movement toward localized MRO capabilities through international partnerships.

Key MRO - Air Platforms Program:

Adani Defence Systems & Technologies Ltd. (ADSTL) has entered into a share purchase agreement to acquire an 85.8% equity stake in Air Works, the largest privately owned aviation maintenance, repair, and overhaul (MRO) provider in India, recognized for its extensive nationwide presence. Air Works delivers a comprehensive range of aviation support services covering line maintenance, heavy maintenance checks, aircraft interiors, painting, redelivery inspections, avionics support, and asset management. The company provides base maintenance services for narrow-body, turboprop, and rotary-wing aircraft through its operational facilities located in Hosur, Mumbai, and Kochi. Its operations are supported by regulatory certifications from civil aviation authorities across more than 20 countries, enabling it to serve both domestic and international customers. Beyond its strong position in civil aviation services, Air Works has established substantial expertise in defense-focused MRO. The company has successfully executed maintenance and sustainment programs for several critical platforms operated by the Indian Navy and the Indian Air Force, demonstrating its capability to support complex military aviation requirements. The acquisition aligns with ADSTL's broader strategy to expand its footprint in the aerospace and defense sustainment ecosystem. By integrating Air Works' technical capabilities and infrastructure, ADSTL aims to strengthen indigenous MRO capacity and enhance long-term support solutions for both civil and defense aviation platforms.

Table of Contents

Defense MRO - Air Platforms Market Report Definition

Defense MRO - Air Platforms Market Segmentation

By Region

By Component

By Aircraft Type

Defense MRO - Air Platforms Market Analysis for next 10 Years

The 10-year Defense MRO - Air Platforms Market analysis would give a detailed overview of Defense MRO - Air Platforms Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense MRO - Air Platforms Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense MRO - Air Platforms Market Forecast

The 10-year Defense MRO - Air Platforms Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense MRO - Air Platforms Market Trends & Forecast

The regional Defense MRO - Air Platforms Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense MRO - Air Platforms Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense MRO - Air Platforms Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense MRO - Air Platforms Market Report

Hear from our experts their opinion of the possible analysis for this market.