|

시장보고서

상품코드

1904995

방위용 케이블 및 하네스 시장(2026-2036년)Global Defense Cables and Harness Market 2026-2036 |

||||||

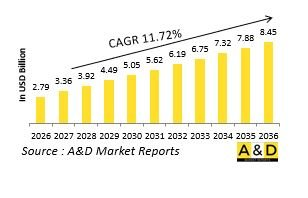

세계의 방위용 케이블 및 하네스 시장 규모는 2026년에 27억 9,000만 달러로 평가되었고, 2036년까지 84억 5,000만 달러에 이를 것으로 보이며, 2026-2036년의 예측 기간 동안 CAGR 11.72%로 성장할 전망입니다.

방위용 케이블 및 하네스 시장 소개

세계의 방위용 케이블 및 하네스 시장은 군사 플랫폼 전반에 걸쳐 전력, 데이터 및 신호를 전송하는 특수 배선 시스템을 포괄하며, 센서, 프로세서, 디스플레이, 제어 장치 및 효과기를 연결하는 신경계 역할을 합니다. 이는 상용 케이블이 아닌 군사 작전에서 발생하는 극한 온도, 진동, 습기, 화학 물질, 전자기 간섭 및 물리적 충격에 견딜 수 있도록 설계된 엔지니어링 시스템입니다. 하네스 어셈블리는 수백 개의 개별 전선을 묶어 보호된 형태로 구성하여 제한된 공간에서도 효율적으로 설치 및 유지보수가 가능하도록 합니다. 항공기, 지상 차량, 함정, 병사 시스템에 이르기까지 모든 방위 부문에 적용되며, 군용 규격 전력 전송부터 센서 네트워크용 고속 데이터 링크에 이르기까지 요구사항이 다양합니다. 플랫폼이 더욱 전기로화되고 네트워크화됨에 따라 케이블 및 하네스 시스템의 복잡성, 밀도, 중요성도 비례하여 증가하여 방위 능력의 필수적이면서도 종종 간과되는 컴포넌트가 되고 있습니다.

방위용 케이블 및 하네스 시장의 기술 영향

방위용 케이블 기술 발전은 경량화, 데이터 처리 능력, 내구성에 중점을 둡니다. 광섬유 케이블은 전자기 간섭에 대한 내성과 경량화 장점을 제공하면서 고대역폭 데이터 전송을 위해 구리 케이블을 보완하거나 대체하는 경우가 점점 더 많아지고 있습니다. 첨단 복합 재료와 나노기술 코팅은 케이블 보호 기능을 강화하면서 질량을 최소화합니다. 커넥터 설계는 밀폐된 공간에서 유지보수를 용이하게 하기 위해 고밀도, 빠른 분리, 블라인드 메이트 기능으로 진화하고 있습니다. 무선 플랫폼 내 통신은 일부 케이블링 요구를 줄이지만 보안 및 신뢰성 측면에서 새로운 과제를 제기합니다. 케이블 내 통합 상태 모니터링 기능은 시스템 장애를 유발하기 전에 초기 결함을 감지합니다. 로봇 공학을 활용한 자동화된 하네스 제작은 복잡한 구성의 일관성을 높이고 생산 시간을 단축합니다. 이러한 혁신은 플랫폼 전기 시스템에서 더 높은 성능, 향상된 신뢰성, 감소된 수명 주기 비용이라는 상충되는 요구를 해결합니다.

방위용 케이블 및 하네스 시장의 주요 촉진요인

플랫폼 전기화 추세(전기 항공기에서 전기 전투 차량에 이르기까지)는 전력 분배 요구 사항을 크게 증가시켜 고용량 케이블링 시스템 개발을 촉진합니다. 현대 플랫폼에서 센서와 이펙터의 확산은 데이터 전송 수요를 기하급수적으로 증가시켜 더 높은 대역폭과 더 강력한 전자기 보호를 모두 필요로 합니다. 모든 이동 플랫폼에 걸친 경량화 요구는 첨단 소재와 하네스 배선 경로 및 구성 최적화를 선호하게 합니다. 유지보수 효율성 요구사항은 플랫폼을 대대적으로 분해하지 않고도 검사, 테스트 및 교체가 용이한 설계를 촉진합니다. 구형 플랫폼의 노후화 관리는 단종된 케이블 유형과 커넥터 설계의 재생산에 대한 지속적인 수요를 창출합니다. 또한 사막의 고온부터 함정의 염분 분무에 이르는 가혹한 환경 운영은 극한 조건 속에서도 장기적 신뢰성을 보장하기 위해 보호 소재와 밀봉 기술의 지속적인 개선을 요구합니다.

방위용 케이블 및 하네스 시장의 지역 동향

지역별 케이블 및 하네스 역량은 종종 자국 플랫폼 제조 능력 및 군산 복합체 생태계와 연계됩니다. 북미는 주요 프로그램의 주계약자 공급망과 통합된 광범위한 전문 공급업체를 유지합니다. 유럽 산업은 민간 및 군용 항공기 시장을 모두 지원하는 다국적 공급업체를 통해 항공우주 응용 부문에서 특히 강점을 보입니다. 아시아태평양 지역은 완전한 공급망 개발이 필요한 자국 플랫폼 프로그램을 개발 중인 국가들을 중심으로 역량이 성장하고 있습니다. 이스라엘 산업은 기존 시스템 업그레이드 및 특수 플랫폼 구성에 특화된 응용 부문에서 탁월합니다. 중동 국가들은 플랫폼 정비 소요 시간 단축을 위해 케이블 시스템의 현지화 유지보수 및 수리 역량을 점차 확대하고 있습니다. 세계의 표준화 노력과 독자적 접근법이 경쟁하는 가운데, 다양한 플랫폼 유형과 고객 선호도가 지역 및 응용 부문별 상이한 도입 패턴을 주도하고 있습니다.

이 보고서는 세계의 방위용 케이블 및 하네스 시장에 대해 조사 분석하여 시장에 영향을 미치는 기술, 향후 10년간의 예측, 각 지역의 동향 등의 정보를 제공합니다.

목차

방위용 케이블 및 하네스 시장 보고서 정의

방위용 케이블 및 하네스 시장 세분화

지역별

플랫폼별

유형별

향후 10년간 방위용 케이블 및 하네스 시장 분석

방위용 케이블 및 하네스 시장 기술

세계의 방위용 케이블 및 하네스 시장 예측

지역 방위용 케이블 및 하네스 시장 동향과 예측

북미

촉진요인, 억제요인, 과제

PEST

시장 예측 및 시나리오 분석

주요 기업

공급자 계층 구조

기업 벤치마킹

유럽

중동

아시아태평양

남미

방위용 케이블 및 하네스 시장 국가 분석

미국

방위 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

시장 예측 및 시나리오 분석

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

방위용 케이블 및 하네스 시장의 기회 매트릭스

방위용 케이블 및 하네스 시장 보고서에 대한 전문가 의견

결론

항공 및 방위 시장 보고서 관련

HBR 26.01.20The Global Defense Cables and Harness market is estimated at USD 2.79 billion in 2026, projected to grow to USD 8.45 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 11.72% over the forecast period 2026-2036.

Introduction to Defense Cables and Harness Market:

The Global Defense Cables and Harness Market encompasses the specialized wiring systems that transmit power, data, and signals throughout military platforms, forming the nervous system that connects sensors, processors, displays, controls, and effectors. These are not commercial cables but engineered systems designed to withstand extreme temperatures, vibration, moisture, chemicals, electromagnetic interference, and physical abuse encountered in military operations. Harness assemblies organize hundreds of individual wires into bundled, protected configurations that can be efficiently installed and maintained in confined spaces. Applications span all defense domains-from aircraft and ground vehicles to ships and soldier systems-with requirements varying from mil-spec power transmission to high-speed data links for sensor networks. As platforms become more electrified and networked, the complexity, density, and criticality of cable and harness systems increase correspondingly, making them essential yet often overlooked components of defense capability.

Technology Impact in Defense Cables and Harness Market:

Technological advancement in defense cabling focuses on weight reduction, data capability, and durability. Fiber optic cables increasingly supplement or replace copper for high-bandwidth data transmission while offering immunity to electromagnetic interference and reduced weight. Advanced composite materials and nanotechnology coatings enhance cable protection while minimizing mass. Connector designs evolve toward higher density, quick-disconnect, and blind-mate capabilities for easier maintenance in confined spaces. Wireless intra-platform communication reduces some cabling requirements but introduces new challenges in security and reliability. Integrated health monitoring capabilities within cables detect incipient faults before they cause system failures. Automated harness fabrication using robotics improves consistency and reduces production time for complex configurations. These innovations address the competing demands for higher performance, increased reliability, and reduced lifecycle costs in platform electrical systems.

Key Drivers in Defense Cables and Harness Market:

Platform electrification trends-from more electric aircraft to electric combat vehicles-substantially increase power distribution requirements, driving development of higher-capacity cabling systems. The proliferation of sensors and effectors on modern platforms creates exponential growth in data transmission needs, necessitating both higher bandwidth and more robust electromagnetic protection. Weight reduction imperatives across all mobile platforms favor advanced materials and optimization of harness routing and configuration. Maintenance efficiency requirements drive designs that facilitate easier inspection, testing, and replacement without extensive platform disassembly. Obsolescence management for legacy platforms creates sustained demand for reproduction of discontinued cable types and connector designs. Additionally, harsh environment operation-from desert heat to shipboard salt spray-mandates continuous improvement in protective materials and sealing technologies to ensure long-term reliability despite extreme conditions.

Regional Trends in Defense Cables and Harness Market:

Regional cable and harness capabilities often align with indigenous platform manufacturing capacity and military-industrial ecosystems. North America maintains extensive specialized suppliers integrated with prime contractor supply chains for major programs. European industry shows particular strength in aerospace applications, with multinational suppliers serving both civil and military aircraft markets. The Asia-Pacific region demonstrates growing capability, particularly in countries with developing indigenous platform programs that require complete supply chain development. Israeli industry excels in specialized applications for upgraded legacy systems and unique platform configurations. Middle Eastern nations increasingly seek localized maintenance and repair capabilities for cable systems to reduce turnaround times for platform servicing. Global standardization initiatives compete with proprietary approaches, with different platform types and customer preferences driving varied adoption patterns across regions and applications.

Key Defense Cables and Harness Program:

Reliance Defence & Engineering's June 2025 joint venture with U.S.-based Coastal Mechanics Inc. at MIHAN, Nagpur, secures MRO and upgrade contracts for land systems wiring harnesses and cables, starting with L-70 40mm air defense guns. The 10-year deal, worth multi-crore annually, modernizes electrical harnesses for reliability in harsh terrains, reducing downtime by 30%. It includes indigenous cable production using MIL-SPEC standards, integrating with Army's 100k+ vehicle fleet predictive maintenance AI pilots. This offsets import dependency, creates 500 jobs, and extends to BMP-II infantry vehicles. Phased rollout covers 500+ L-70 units by 2027, boosting layered air defense amid LAC tensions.

Table of Contents

Defense Cables and Harness Market Report Definition

Defense Cables and Harness Market Segmentation

By Region

By Platform

By Type

Defense Cables and Harness Market Analysis for next 10 Years

The 10-year defense cables and harness market analysis would give a detailed overview of defense cables and harness market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Cables and Harness Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Cables and Harness Market Forecast

The 10-year defense cables and harness market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Cables and Harness Market Trends & Forecast

The regional defense cables and harness market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Cables and Harness Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Cables and Harness Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Cables and Harness Market Report

Hear from our experts their opinion of the possible analysis for this market.