|

시장보고서

상품코드

1936040

방위 분야 5G 시장(2026-2036년)Global 5G in Defense Market 2026-2036 |

||||||

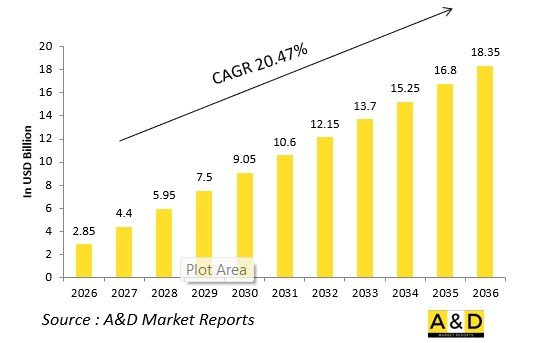

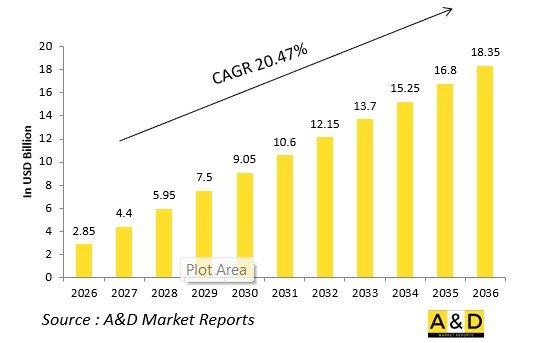

세계 방위 분야 5G 시장 규모는 2026년 28억 5,000만 달러로 추정되며, 2026년부터 2036년까지 예측 기간 동안 CAGR 20.47%로 성장하여 2036년까지 183억 5,000만 달러에 달할 것으로 예상됩니다.

소개

세계 방위 분야 5G 시장은 군용 통신에 혁명을 가져와 전 영역 공동 작전에 필수적인 고대역폭, 저지연 통신 링크를 실현할 것입니다. 항공기, 육상, 해군 플랫폼에 구축되는 5G는 ISR(정보, 감시, 정찰), 자율 시스템, 분산형 지휘 노드를 위한 실시간 데이터 공유를 지원합니다. 방해에 대한 내성이 기존 네트워크에 대한 우위를 결정짓고 있습니다.

AI, IoT, 엣지 컴퓨팅과의 융합으로 시장 모멘텀이 가속화되고, 스펙트럼 효율화를 위한 대규모 MIMO와 지향성 신호를 위한 빔포밍을 실현합니다. 프라이빗 5G 네트워크는 전술적 엣지를 보호하고, 위성을 통한 비지상 확장은 원격 전장을 커버합니다. 각 벤더들은 소프트웨어 정의 무선 및 가상화 기술로 협력하여 민첩한 배포를 추진하고 있습니다.

지정학적 요청이 도입을 촉진하고, 대등한 위협에 대한 C4ISR(지휘-통제-통신-통신-컴퓨터-정보-감시-정찰)을 강화합니다. 상호운용성 표준은 민수용과 군용 주파수 대역을 연결합니다. 사이버 위험 속에서 공급망은 견고한 하드웨어를 우선시합니다. 에릭슨, 탈레스 등 주요 기업들이 방위용 핵심 기술을 선도하는 가운데, 경쟁은 더욱 치열해지고 있습니다.

5G가 국방 분야에 미치는 기술적 영향

5G는 지연시간을 밀리초 단위로 줄이고, 실전 환경에서의 실시간 영상 전송, AR 오버레이, 원격 조종 드론의 운용을 가능하게함으로써 국방 분야에 큰 영향을 미칠 것입니다. Massive MIMO는 처리량을 획기적으로 향상시키고, 빔포밍 기술을 통한 정밀한 빔으로 다수의 UAV와 지상 로봇의 센서 융합을 지원합니다.

기지국에서의 엣지 컴퓨팅은 ISR 데이터를 로컬에서 처리하여 클라우드 의존도를 최소화하고 생존성을 향상시킵니다. 네트워크 슬라이싱은 대역폭을 미션 크리티컬 트래픽을 위해 대역폭을 분할하고, 지휘계통과 후방 지원 스트림을 분리합니다. 소프트웨어 정의 네트워크(SDN)와 가상화(NFV)를 통해 작전 수행 중 동적 재구성이 가능합니다.

위성 백홀은 지상 5G를 열악한 지역으로 확장하고, NTN을 통합하여 보편적 커버리지를 실현합니다. AI 최적화 스펙트럼 공유는 인지 무선 기술을 통해 간섭을 방지합니다. 보안 파형은 전자전을 견딜 수 있고, 양자 안전 암호화가 데이터 링크를 보호합니다.

증강현실 인터페이스는 높은 대역폭을 활용하여 몰입형 훈련과 원격 유지보수를 실현합니다. 자율주행 차량 행렬은 차량 행렬 작전을 위한 고해상도 영상을 스트리밍합니다. 이러한 능력은 OODA 루프를 단축하고, 유인/무인 연계를 강화하며, 스마트 창고를 통한 물류 확장을 가능하게함으로써 전술적 기동성을 재정의합니다.

방위 분야 5G의 주요 촉진요인

전 영역 통합 지휘에 대한 수요가 5G 도입을 촉진하고, 군종 간 원활한 데이터 융합을 필요로 합니다. 드론의 보급과 자율화는 시야 밖 제어를 위한 초신뢰성 연결을 필수로 합니다.

현대화 계획에서는 전자전에 견딜 수 있는 강력한 네트워크가 우선시됩니다. 긴장 상태에서의 고도의 방어 태세는 일선 기지에 대한 민간 5G 배치를 가속화할 것입니다. 웨어러블 기기에서 무기에 이르기까지 IoT의 보급은 방대한 디바이스 처리 능력을 요구합니다.

상용 생태계와의 상호운용성을 통해 COTS 하드웨어로 인한 비용 절감을 실현할 수 있습니다. 엣지 AI의 통합은 전술적 엣지에서 데이터 기반 의사결정을 가능하게 합니다. 주파수 경매에서는 경쟁 대역의 동적 할당에 중점을 둡니다.

사이버 보안 요구사항은 제로 트러스트 아키텍처로 강화된 5G 코어를 촉진합니다. VR/AR 시뮬레이션을 통한 훈련 혁명은 대역폭을 활용합니다. 동맹국 표준을 통한 수출 가능성이 확대됩니다.

예측 유지보수 및 자동 보충과 같은 물류 혁신은 저지연 통신에 의존합니다. 이러한 촉진요인으로 인해 5G는 C4ISR 기반에 포함됩니다.

방위 분야 5G 지역별 동향

북미는 JADC2를 위한 전술적 5G에 대한 대규모 투자를 주도하고 있으며, MIMO 테스트 환경과 NTN 통합의 선구자적 역할을 하고 있습니다.

유럽은 NATO 프레임워크에 따른 조정을 통해 연합 네트워크용 SDN과 항공모함 작전을 위한 해군 5G를 구축하고 있습니다.

아시아태평양에서는 중국이 섬 방어를 위한 주권 5G를 추진하고, 인도가 코어의 현지화를 추진하는 등 인도 태평양 지역의 경쟁이 심화되는 가운데 빠른 진전을 보이고 있습니다.

중동 지역에서는 비대칭 위협 대책으로 빔포밍 ISR 네트워크를 통한 기지 강화가 진행되고 있습니다.

러시아는 최전방 작전을 위해 방해 전파에 강한 파형을 개발 중입니다.

인도 태평양 지역 동맹국들은 해상 영역 인식을 위한 위성 보완형 5G를 중시하고 있습니다.

라틴아메리카에서는 대(對)드론 네트워크의 시범 운영이 시작되고 있습니다. 아프리카에서는 평화유지활동 통신의 통합이 진행되고 있습니다.

하이브리드형 지상/우주 아키텍처가 주류가 되고, 아시아가 공급 점유율을 차지할 것으로 예상됩니다.

국방 프로그램의 주요 5G 기술

미 국방부의 'Innovate Beyond 5G(IB5G)'는 MHz에서 GHz 대역의 Massive MIMO 기술을 선구적으로 추진하고 있으며, Nokia Bell Lab과의 협력을 통해 전술적 처리량을 향상시키고 있습니다.

JADC2 이니셔티브는 실시간 화력 지원을 위해 5G를 멀티 도메인 네트워크에 통합합니다.

골든 돔 미사일 방어 시스템은 경보 발령과 요격에 5G를 활용하고 있습니다.

해군의 5G에서 차세대 통신(NextG)으로의 전환 실증을 통해 함정 네트워크의 견고화를 도모하고 있습니다.

유럽의 5G 군사 네트워크는 육상, 공중, 해상 영역을 융합합니다.

인도 태평양 훈련에서는 드론 군단을 위한 빔포밍 기술을 시험하고 있습니다.

프라이빗 5G 베이스캠프가 스마트 물류를 실현합니다.

오리온 계획은 5G와 AI를 통합하여 엣지 ISR을 실현합니다.

전술 에지 노드 프로토타입이 최전방 기지에서 강력한 5G를 제공합니다.

이러한 프로그램은 미래의 전투원을 위한 안전하고 확장 가능한 네트워크를 구축합니다.

목차

방위 분야 5G 시장 - 목차

방위 분야 5G 시장 보고서의 정의

방산 시장 세분화

향후 10년간의 방위 분야 5G 시장 분석

방위 분야 5G 시장 기술

세계 방위 분야 5G 시장 전망

방산 시장에서의 지역 5G 동향 및 전망

시장 예측 및 시나리오 분석

방위 분야 5G 시장 국가별 분석

시장 예측 및 시나리오 분석

방위 분야 5G 시장 기회 매트릭스

방위 분야 5G 시장 관련 전문가 의견 보고서

결론

Aviation and Defense Market Reports 소개

KSM 26.03.05The Global 5G in Defense Market is estimated at USD 2.85 billion in 2026, projected to grow to USD 18.35 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 20.47% over the forecast period 2026-2036.

Introduction

The global 5G in defense market revolutionizes military communications, delivering high-bandwidth, low-latency links essential for joint all-domain operations. Deployed across airborne, land, and naval platforms, 5G supports real-time data sharing for ISR, autonomous systems, and distributed command nodes. Resilience against jamming defines its edge over legacy networks.

Market momentum builds on convergence with AI, IoT, and edge computing, enabling massive MIMO for spectrum efficiency and beamforming for directed signals. Private 5G networks secure tactical edges, while non-terrestrial extensions via satellites cover remote theaters. Vendors collaborate on software-defined radios and virtualization for agile deployments.

Geopolitical imperatives drive adoption, fortifying C4ISR against peer threats. Interoperability standards bridge commercial and military spectra. Supply chains prioritize hardened hardware amid cyber risks. Competition intensifies with primes like Ericsson and Thales pioneering defense-grade cores.

Technology Impact in 5G in Defense

5G profoundly impacts defense by slashing latencies to milliseconds, enabling real-time video feeds, AR overlays, and teleoperated drones in contested environments. Massive MIMO multiplies throughput, supporting sensor fusion from swarms of UAVs and ground robots via beamformed precision beams.

Edge computing at base stations processes ISR data locally, minimizing cloud dependency and enhancing survivability. Network slicing partitions bandwidth for mission-critical traffic, isolating command from logistics streams. Software-defined networking (SDN) and virtualization (NFV) allow dynamic reconfiguration mid-operation.

Satellite backhaul extends terrestrial 5G to austere zones, integrating NTNs for ubiquitous coverage. AI-optimized spectrum sharing evades jamming through cognitive radios. Secure waveforms resist electronic warfare, while quantum-safe encryption safeguards data links.

Augmented reality interfaces leverage high bandwidth for immersive training and remote maintenance. Autonomous convoys stream HD feeds for convoy ops. These capabilities compress OODA loops, empower manned-unmanned teaming, and scale logistics via smart warehouses, redefining tactical agility.

Key Drivers in 5G in Defense

Demand for joint all-domain command drives 5G adoption, requiring seamless data fusion across services. Proliferating drones and autonomy necessitate ultra-reliable connectivity for beyond-line-of-sight control.

Modernization programs prioritize resilient networks against peer electronic warfare. High defense postures amid tensions accelerate private 5G deployments for forward bases. IoT proliferation-from wearables to munitions-demands massive device handling.

Interoperability with commercial ecosystems cuts costs via COTS hardware. Edge AI integration enables data-driven decisions at the tactical edge. Spectrum auctions favor dynamic allocation for contested bands.

Cybersecurity mandates spur hardened 5G cores with zero-trust architectures. Training revolutions via VR/AR simulations leverage bandwidth. Export potentials expand through allied standards.

Logistics transformation-predictive maintenance, automated resupply-relies on low-latency links. These drivers embed 5G as C4ISR backbone.

Regional Trends in 5G in Defense

North America leads with massive investments in tactical 5G for JADC2, pioneering MIMO testbeds and NTN integrations.

Europe harmonizes via NATO frameworks, deploying SDN for coalition networks and naval 5G for carrier ops.

Asia-Pacific surges amid Indo-Pacific rivalries, with China advancing sovereign 5G for island defenses and India localizing cores.

Middle East fortifies bases with beamformed ISR nets against asymmetric threats.

Russia develops jamming-resistant waveforms for frontline use.

Indo-Pacific allies emphasize satellite-augmented 5G for maritime domain awareness.

Latin America pilots counter-drone networks. Africa integrates for peacekeeping comms.

Trends favor hybrid terrestrial-space architectures, with Asia capturing supply shares.

Key 5G in Defense Programs

DoD's Innovate Beyond 5G (IB5G) pioneers Massive MIMO from MHz to GHz, boosting tactical throughput with Nokia Bell Labs.

JADC2 initiatives weave 5G into multi-domain webs for real-time fires.

Golden Dome missile defense leverages 5G for alerts and intercepts.

Naval 5G-to-NextG demos harden shipboard networks.

European 5G military networks fuse land-air-sea slices.

Indo-Pacific exercises test beamforming for drone swarms.

Private 5G base camps enable smart logistics.

ORION program integrates 5G with AI for edge ISR.

Tactical Edge Node prototypes deliver resilient 5G at forward positions.

These programs forge secure, scalable nets for future warfighters.

Table of Contents

5G in Defense Market - Table of Contents

5G in Defense Market Report Definition

5G in Defense Market Segmentation

By Platform

By Region

By Chipset

5G in Defense Market Analysis for next 10 Years

The 10-year 5G in Defense Market analysis would give a detailed overview of 5G in Defense Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of 5G in Defense Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global 5G in Defense Market Forecast

The 10-year 5G in defense market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional 5G in Defense Market Trends & Forecast

The regional 5G in Defense Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of 5G in Defense Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for 5G in Defense Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on 5G in Defense Market Report

Hear from our experts their opinion of the possible analysis for this market.