|

시장보고서

상품코드

1936045

방어 항공기 제동 시스템 시장(2026-2036년)Global Defense Aircraft Braking Systems Market 2026-2036 |

||||||

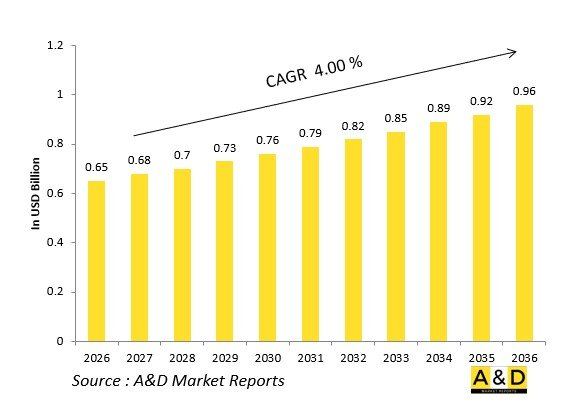

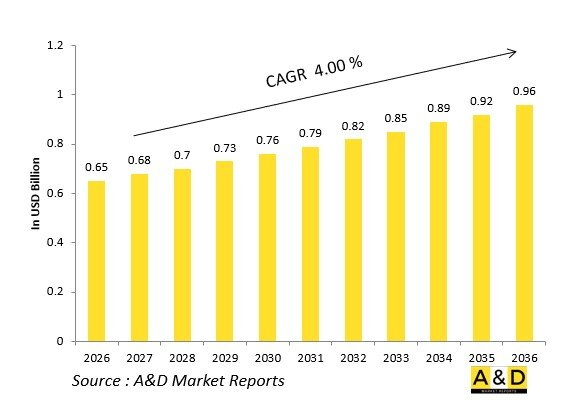

세계 방어 항공기 제동 시스템 시장 규모는 2026년에 6억 5,000만 달러로 추정되며 2026년부터 2036년까지 예측 기간 동안 4.00%의 CAGR로 성장하여 2036년에는 9억 6,000만 달러에 달할 것으로 예상됩니다.

소개

세계 방어 항공기 제동 시스템 시장은 전술 항공기의 성능을 지원하고 항공모함, 전선 활주로, 손상된 활주로에 고에너지 착륙 시 정밀한 제어를 실현합니다. 멀티 디스크 카본 스택, 유압 파워팩, 미끄럼 방지 프로세서로 기체를 과부하로부터 보호하면서 적극적인 기동을 가능하게 합니다.

시장 역학은 5세대 전투기의 유지 관리와 회전익 항공기의 업그레이드를 반영하고 있으며, 브레이크 기술은 강철 로터에서 지속적인 전투 부하에서도 페이드(제동력 감쇠)를 견딜 수 있는 경량 복합재로 진화하고 있습니다. 핵심 기술은 세분화된 탄소 방열판, 전기 신호 작동 시스템, 비행 제어 시스템 및 통합된 예지보전 건강 모니터링 시스템을 포함합니다.

신속한 배치에 대한 지정학적 수요가 조달을 촉진하고 있으며, STOBAR 항공모함 및 사막 기지와 호환되는 시스템이 우선순위를 차지하고 있습니다. 모듈식 설계로 전체 레거시 함대를 쉽게 개조할 수 있습니다. 공급망에서는 고융점 금속 및 세라믹 코팅이 중요시되고 있습니다. 경쟁사로는 하니웰, 사프란, 콜린스 에어로스페이스가 전기식 변종에 대한 선구자 역할을 하고 있습니다.

이 시장은 지상에서의 기동력을 통한 항공 우위를 실현할 수 있는 시장입니다.

방어 항공기 제동 시스템에서 기술의 영향

탄소계 복합재료는 뛰어난 방열성으로 브레이크에 혁명을 가져왔으며, 항공모함 착륙 및 무기 운반에 필수적인 고에너지의 반복적인 정지를 페이드 없이 가능하게 합니다. 분할된 로터를 통해 고온 부분을 개별적으로 교체할 수 있어 임무 간 다운타임을 크게 줄일 수 있습니다.

전기 유압 서보 밸브는 플라이 바이 와이어와 통합되어 전체 기어 트랙의 타이어 마모를 최적화하는 자동 제동 스케줄을 실현하고 정확한 압력 조정을 실현합니다. 미끄럼 방지 알고리즘은 관성 기준에 따라 바퀴의 속도를 처리하고, 펄스 부호 변조를 통해 오염된 활주로에서 잠금 현상을 방지합니다.

스택에 내장된 예지 센서가 탄소 산화 및 유압 오염을 모니터링하여 성능 저하 전에 유지보수를 촉구합니다. 전기 브레이크 액추에이터는 유압 라인을 완전히 제거하여 스텔스 설계의 취약성을 줄이고, 무게 최적화 착륙을 위한 가변 브레이크 토크를 실현합니다.

통합형 브레이크 바이 와이어는 자동 브레이크와 역추력 장치 및 스포일러를 연동하여 착륙 활주 거리를 단축시킵니다. 세라믹 마찰재는 방향성 에너지 열을 견딜 수 있습니다. 디지털 트윈 기술을 통한 마모 프로파일 시뮬레이션으로 수명 연장. 이러한 발전으로 출격률이 향상되고, 미정비 활주로에서 운항이 가능해졌습니다.

방어 항공기 제동 시스템의 주요 촉진요인

5세대 전투기 프로그램에서는 스텔스 코팅과 무기 탑재량을 견딜 수 있는 고사이클 브레이크가 필수적입니다. 원정 작전 교리에서는 반 정비된 활주로에서 단거리 이착륙 능력을 요구하고 있으며, 강철에서 탄소 소재로 업그레이드를 추진하고 있습니다.

항공모함 항공에서는 반복적인 착륙 제동이 요구되며, 페이드 내성 스택이 우선시됩니다. 회전익 항공기의 브라운아웃 시, 시야가 없는 먼지 속에서도 제어를 유지하기 위해서는 변조 브레이크가 필수적입니다.

유지관리의 경제성에서는 예기치 못한 철거를 최소화하는 예지보전 시스템이 유리합니다. 수출 오프셋은 유압 어큐뮬레이터의 현지 생산을 촉진합니다. 상호운용성 표준을 통해 연합군 전체에서 공통의 예비 부품을 사용할 수 있습니다.

지향성 에너지 무기의 보급을 위해서는 내열성 세라믹이 필요합니다. 녹색 조달은 소모성 금속보다 재생 가능한 탄소 소재를 장려합니다. 공급망 탄력성은 원자재 제약에 대응할 수 있습니다.

이러한 요구로 인해 제동 시스템은 전술적 실현 수단으로 자리매김하고 있습니다.

방어 항공기 제동 시스템의 지역별 동향

북미에서는 F-35의 유지관리가 주도하고 있으며, 수직 착륙을 위한 카본스택 기술 혁신이 진행되고 있습니다.

유럽에서는 유로파이터와 라팔의 전동 액추에이터를 업그레이드하여 분산 작전을 가능하게 하고 있습니다.

아시아태평양에서는 국산 전투기(인도의 테자스, 중국의 J-35)가 급성장하면서 항공모함 대응을 우선시하고 있습니다.

중동에서는 사막의 더위에 대응할 수 있는 높은 출격률의 함대를 갖추고 있습니다.

러시아는 미정비 활주로 대응을 위해 MiG-35의 제동 시스템을 개선하고 있습니다.

한국은 지역 억지력 강화를 위해 KF-21과의 통합을 추진하고 있습니다.

모든 전기식 시스템 도입 동향에서는 아시아태평양이 제조 점유율을 확대.

주요 방어 항공기용 제동 시스템 계획

F-35 라이트닝 II는 단거리 이착륙(STOVL) 운용을 위해 카본 스택과 자동 브레이크 바이 와이어를 통합했습니다.

라팔은 항공모함 공격용으로 세분화된 세라믹을 채택했습니다.

유로파이터 트랜쉬 개량형은 제동시스템과 비행 제어 시스템을 통합했습니다.

인도 테자스 Mk2는 국산 카본 로터를 장착했습니다.

KC-46 페가수스 급유기의 제동 시스템은 고부하에 대응합니다.

CVN-78 포드급 항공모함의 투석기 통합에는 정밀한 변조가 필요합니다.

블랙호크 UH-60M은 먼지로 인한 시야 불량 시 착륙에 대응하기 위해 전동 액추에이터를 개선했습니다.

V-22 Osprey의 틸트 로터 기계는 프로프로터(보조 로터) 전환 시 제동을 관리합니다.

목차

방어 항공기 제동 시스템 시장 - 목차

방어 항공기 제동 시스템 필드 보고서의 정의

방어 항공기 제동 시스템 시장 시장 세분화

방어 항공기 제동 시스템 시장 : 향후 10년간의 시장 분석

방어 항공기 제동 시스템 시장 기술 시장

세계 방어 항공기 제동 시스템 시장 예측

지역 방위항공기용 제동시스템 분야 동향 및 전망

시장 예측 및 시나리오 분석

방어 항공기 제동 시스템 시장 국가별 분석

시장 예측 및 시나리오 분석

방어 항공기 제동 시스템 시장의 기회 매트릭스

방어 항공기 제동 시스템 시장에 대한 전문가 의견 시장 보고서

결론

Aviation and Defense Market Reports 소개

KSM 26.03.05The Global Defense Aircraft Braking Systems Market is estimated at USD 0.65 billion in 2026, projected to grow to USD 0.96billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.00% over the forecast period 2026-2036.

Introduction

The global Defense Aircraft Braking Systems market underpins tactical aircraft performance, delivering precise control during high-energy landings on carriers, forward strips, and damaged runways. Multi-disc carbon stacks, hydraulic power packs, and anti-skid processors enable aggressive maneuvers while protecting airframes from overload.

Market dynamics reflect fifth-generation fighter sustainment and rotary-wing upgrades, where braking evolves from steel rotors to lightweight composites resisting fade under sustained combat loads. Core technologies include segmented carbon heat sinks, electrically signaled actuation, and prognostic health monitoring integrated with flight controls.

Geopolitical demands for rapid deployment drive procurement, prioritizing systems compatible with STOBAR carriers and desert bases. Modular designs facilitate retrofits across legacy fleets. Supply chains emphasize refractory metals and ceramic coatings. Competition features Honeywell, Safran, and Collins Aerospace pioneering all-electric variants.

This market enables air dominance through ground agility.

Technology Impact in Defense Aircraft Braking Systems

Carbon-carbon composites revolutionize braking with superior heat dissipation, enabling repeated high-energy arrests without fade-critical for carrier traps and weapons deliveries. Segmented rotors allow hot sections to be swapped independently, slashing downtime between missions.

Electro-hydraulic servo valves deliver precise pressure modulation, integrating with fly-by-wire for auto-brake schedules that optimize tire wear across gear trucks. Anti-skid algorithms process wheel speeds against inertial references, preventing lockup on contaminated runways via pulse-code modulation.

Prognostic sensors embedded in stacks monitor carbon oxidation and hydraulic contamination, cueing maintenance before performance degrades. Electric braking actuators eliminate hydraulic lines entirely, reducing vulnerability in stealth designs and enabling variable brake torque for weight-optimized landings.

Integrated brake-by-wire fuses autobrake with thrust reversers and spoilers, compressing landing rolls. Ceramic friction materials withstand directed-energy heat. Digital twins simulate wear profiles for lifetime extension. These advancements boost sortie rates and enable operations from unprepared strips.

Key Drivers in Defense Aircraft Braking Systems

Fifth-generation fighter programs mandate high-cycle braking resilient to stealth coatings and weapons loads. Expeditionary doctrines require short-field capability on semi-prepared surfaces, driving carbon upgrades over steel.

Carrier aviation demands repeated arrested landings, prioritizing fade-resistant stacks. Rotary-wing brownouts necessitate modulated braking to maintain control in zero-visibility dust.

Sustainment economics favor prognostic systems minimizing unscheduled removals. Export offsets spur localized production of hydraulic accumulators. Interoperability standards enable common spares across coalitions.

Directed-energy proliferation requires heat-resistant ceramics. Green procurement pushes recyclable carbon over expendable metals. Supply chain resilience counters raw material constraints.

These imperatives position braking as tactical enablers.

Regional Trends in Defense Aircraft Braking Systems

North America leads with F-35 sustainment driving carbon stack innovations for vertical landings.

Europe upgrades Eurofighter and Rafale with electric actuators for dispersed ops.

Asia-Pacific surges via indigenous fighters-India's Tejas, China's J-35-prioritizing carrier compatibility.

Middle East equips high-sortie fleets against desert heat.

Russia adapts MiG-35 braking for rough strips.

South Korea integrates with KF-21 for regional deterrence.

Trends favor all-electric systems; Asia-Pacific gains manufacturing share.

Key Defense Aircraft Braking Systems Programs

F-35 Lightning II integrates carbon stacks with autobrake-by-wire for STOVL operations.

Rafale upgrades deploy segmented ceramics for carrier assaults.

Eurofighter Tranche enhancements fuse braking with flight controls.

India's Tejas Mk2 equips indigenous carbon rotors.

KC-46 Pegasus tanker braking handles heavy loads.

CVN-78 Ford-class catapult integration demands precision modulation.

Black Hawk UH-60M upgrades electric actuators for brownout landings.

V-22 Osprey tiltrotor braking manages proprotor transitions.

Table of Contents

Defense Aircraft Braking Systems Market Market - Table of Contents

Defense Aircraft Braking Systems Market Market Report Definition

Defense Aircraft Braking Systems Market Market Segmentation

By Platform

By Brake Type

By Control System

By Function

Defense Aircraft Braking Systems Market Market Analysis for next 10 Years

The 10-year Defense Aircraft Braking Systems Market market analysis would give a detailed overview of Defense Aircraft Braking Systems Market market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Aircraft Braking Systems Market Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Aircraft Braking Systems Market Market Forecast

The 10-year Defense Aircraft Braking Systems Market market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Aircraft Braking Systems Market Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Aircraft Braking Systems Market Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Aircraft Braking Systems Market Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Aircraft Braking Systems Market Market Report

Hear from our experts their opinion of the possible analysis for this market.