|

시장보고서

상품코드

1996990

방위용 레이더 고도계 시장(2026-2036년)Global Defense Radar Altimeters Market 2026-2036 |

||||||

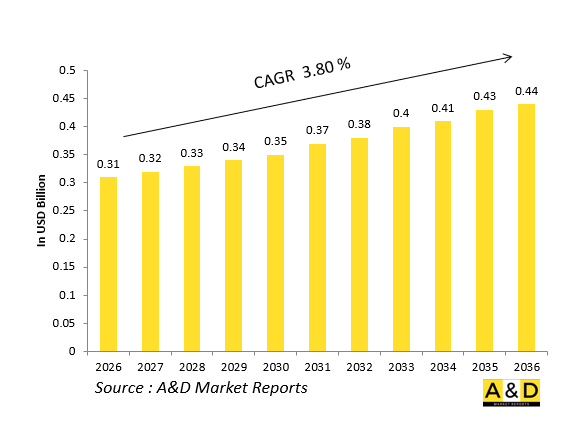

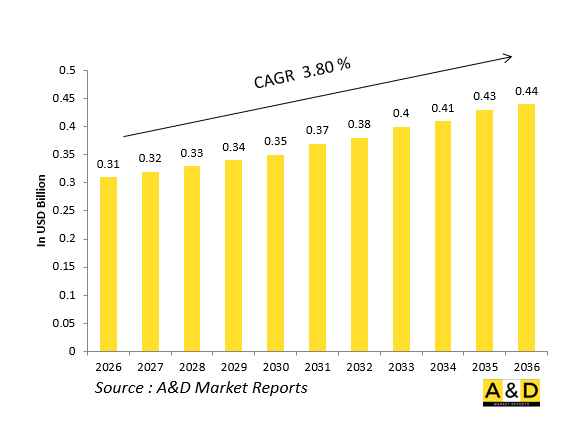

세계의 방위용 레이더 고도계 시장 규모는 2026년에 3억 1,000만 달러로 추계되고 있으며, 2026-2036년의 예측 기간 중 CAGR 3.80%로 성장하며, 2036년에는 4억 4,000만 달러에 달할 것으로 전망되고 있습니다.

소개:

국방용 레이더 고도계는 무선 주파수 신호를 이용하여 항공기나 플랫폼의 지상 또는 해수면으로부터의 고도를 측정하는 특수한 무선 고도계 시스템으로, 비행 안전과 임무 수행에 필수적인 저고도 클리어런스 데이터를 제공합니다. 이 고도계는 전투기, 공격기, 해상초계기, 특수임무기, 헬리콥터, 무인시스템에 탑재되어 지표면 통과 비행, 지형추적 비행, 정밀한 진입 및 착륙 작전을 지원하고 있습니다. 2026-2036년 공군이 저시야 및 저고도 침투 임무와 점점 더 복잡해지는 다중 도메인 비행 프로파일을 우선시함에 따라 국방용 레이더 고도계 시장은 확대되고 있습니다.

현대의 레이더 고도계는 단순한 아날로그 고도계에서 비행 제어 시스템, 항법 시스템 및 미션 컴퓨터에 직접 데이터를 공급하는 통합형 디지털 노드로 진화하고 있습니다. 특히 시야가 좋지 않은 상황이나 선상 환경에서 고급 저고도 진입 모드, 자동 지형 추종 및 자동 착륙 시퀀싱를 지원합니다. 전자전 환경이 심화됨에 따라 고간섭 환경에서도 안정적으로 작동할 수 있는 견고하고 간섭에 강한 레이더 고도계에 대한 수요가 증가하고 있습니다. 이러한 시스템은 차세대 전투기, 훈련기, 무인항공 플랫폼의 필수 구성 요소로 점점 더 많이 지정되고 있으며, 가혹한 작전 환경에서의 생존성과 작전 효율성을 모두 지원하고 있습니다.

국방용 레이더 고도계 시장에서 기술의 영향력

기술의 발전으로 국방용 레이더 고도계는 비교적 단순한 고도 측정 기기에서 정교한 멀티모드 소프트웨어 정의 센서로 변모하고 있습니다. 최신 장비는 솔리드 스테이트 송신기, 고급 디지털 신호 처리 및 협대역 또는 주파수 변조 파형을 활용하여 정확도 향상, 간섭에 대한 내성 강화, 다른 탑재 시스템과의 간섭을 최소화합니다. 이러한 기능 강화로 레이더 고도계는 강력한 레이더나 통신 발신기 근처 등 전자파가 밀집된 환경에서도 안정적으로 작동할 수 있게 되었습니다.

디지털 비행 제어 시스템과의 통합을 통해 레이더 고도계는 자동 저고도 비행 프로파일, 지형 추적 비행 및 정밀한 진입 및 착륙 모드를 지원하여 시야가 좋지 않을 때 조종사의 작업 부하를 줄이고 안전성을 향상시킬 수 있습니다. 개방형 아키텍처와 모듈식 설계를 통해 소프트웨어 업데이트 및 구성 변경이 가능하며, 동일한 기본 하드웨어를 여러 플랫폼 및 미션 프로파일에서 활용할 수 있습니다. 강화된 사이버 보안과 안전한 데이터 버스를 통해 네트워크화된 전투 환경에서 고도 관련 데이터 스트림이 변조되는 것을 방지합니다. 또한 소형화 및 저소비전력화를 통해 더 작은 무인 플랫폼이나 특수 임무용 포드에 탑재가 가능해져 호스트 플랫폼에 직접적인 위협을 가하지 않고 고도에 기반한 정밀 기동 및 스탠드오프 작전을 수행할 수 있습니다. 이러한 혁신은 종합적으로 플랫폼의 생존성, 임무의 유연성, 저고도에서의 작전 효과를 향상시킵니다.

국방용 레이더 고도계 시장의 주요 추진 요인

국방용 레이더 고도계 시장은 분쟁 영공에서 핵심 생존 전술로서 저고도 비행과 지표면 통과 비행의 중요성이 지속되고 있는 것에 힘입어 성장하고 있습니다. 현대의 전투기, 공격기 및 특수 임무 플랫폼은 지상의 정확한 실시간 고도 데이터에 의존하여 험준한 지형과 장애물이 많은 지형 상공에서 안전 여유를 유지하면서 적의 레이더 감지 범위 아래로 비행합니다. 이러한 요구사항은 첨단 통합 방공 시스템의 보급으로 더욱 강화되고 있으며, 공군은 강력한 레이더 고도계로 지원되는 보다 복잡한 지형 마스킹 비행 프로파일을 채택해야 합니다.

또 다른 주요 요인은 해상 및 선상 작전의 확대입니다. 레이더 고도계는 회전익 항공기 및 특수 임무 항공기의 정밀한 저고도 접근, 항공모함 착륙, 호버링 및 착륙 시퀀싱를 가능하게 합니다. 또한 무인 전투기 및 장시간 체류형 UAV 프로그램의 확대는 자율 지형 추적 및 장애물 회피 기능을 지원하는 소형의 견고한 레이더 고도계에 대한 수요를 창출하고 있습니다. 함대 현대화 및 수명 연장 프로그램을 통해 구형 플랫폼을 디지털 항공전자, 비행제어법칙, 전자전 시스템과 호환되는 개선된 레이더 고도계 시스템으로 개조하는 작업이 가속화되고 있습니다. 동시에 동맹국 간의 상호 운용성 및 표준화 요구 사항은 공통 레이더 고도계 인터페이스 및 데이터 형식의 채택을 촉진하고 물류 지원 및 훈련 공유를 가능하게 합니다. 안전 및 인증 기준은 저고도에서의 사고 위험을 최소화하고, 신뢰성과 내결함성이 뛰어난 설계의 필요성을 더욱 강조하고 있습니다.

방산용 레이더 고도계 시장의 지역별 동향

지역별로 보면 북미는 여전히 첨단 레이더 고도계 개발의 주요 거점이며, 저고도 침투 및 함상 운용을 중시하는 대규모 전투기, 공격기, 해상 초계기 및 무인 항공기 프로그램에 의해 지원되고 있습니다. 미국과 파트너 국가들은 차세대 플랫폼에 투자하고 있으며, 조달 계약에는 일반적으로 자동 저고도 비행, 해상 진입 및 전자전에 대한 내성을 갖춘 통합 레이더 고도계가 포함되어 있습니다.

유럽에서는 공동 전투 항공 및 다목적 프로그램에서 각국 공군 간의 상호 운용성과 공통 인증 기반을 지원하는 표준화된 레이더 고도계 아키텍처가 채택되고 있습니다. 아시아태평양에서는 여러 국가들이 공군 현대화를 추진하면서 국산 해상 공격 능력과 특수 임무 능력을 확대함에 따라 국내 조달 또는 공동 개발을 통한 레이더 고도계 솔루션에 대한 수요가 빠르게 증가하고 있습니다. 중동 및 걸프 지역 국가들은 사막과 해상에서 저고도 작전을 지원하고 전자전 방해에 대응할 수 있는 레이더 고도계를 장착한 현대화 또는 신규 항공기 군단에 투자하고 있습니다. 이 지역에서는 고정익 항공기, 회전익 항공기, 선박 및 무인 플랫폼 간에 재사용 및 업그레이드가 가능한 소형, 모듈식, 개방형 아키텍처의 레이더 고도계에 대한 선호도가 높아지고 있습니다. 국내 공급 및 기술 주권 정책도 지역내 설계 및 생산을 촉진하는 한편, 수출 관리 및 보안 체제가 고급 고도계 변형의 배치에 영향을 미치고 있습니다.

세계의 국방용 레이더 고도계(Defense Radar Altimeter) 시장을 조사했으며, 주요 동향, 시장 영향요인, 주요 기술 및 그 영향, 주요 지역 및 국가별 동향, 시장 기회 분석 등의 정보를 정리하여 전해드립니다.

목차

방위용 레이더 고도계 시장 : 목차

방위용 레이더 고도계 시장 : 리포트의 정의

방위용 레이더 고도계 시장 : 세분화

향후 10년간 방위용 레이더 고도계 시장의 분석

세계의 방위용 레이더 고도계 시장 예측

방위용 레이더 고도계 시장 : 지역별 동향과 예측

시장 예측·시나리오 분석

방위용 레이더 고도계 시장 : 국가별 분석

시장 예측·시나리오 분석

방위용 레이더 고도계 시장 : 시장 기회 매트릭스

결론

KSA 26.04.20Global Defense Radar Altimeters Market

The Global Defense Radar Altimeters Market is estimated at USD 0.31 billion in 2026, projected to grow to USD 0.44 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.80% over the forecast period 2026-2036.

1. Introduction:

Defense radar altimeters are specialized radio altimeter systems that measure the height of an aircraft or platform above the ground or sea surface using radio frequency signals, providing critical low altitude clearance data for flight safety and mission execution. These altimeters are embedded in fighters, attack aircraft, maritime patrol platforms, special mission aircraft, helicopters, and unmanned systems, supporting nap of the earth flying, terrain following, and precise approach and landing operations. Over the 2026-2036 horizon, the defense radar altimeter market is expanding as air forces prioritize low observable, low level penetration missions and increasingly complex, multi domain flight profiles.

Modern radar altimeters are evolving from simple analog based height meters into integrated digital nodes that feed data directly into flight control systems, navigation suites, and mission computers. They support advanced low level penetration modes, automatic terrain following, and automated landing sequences, especially in poor visibility and shipboard environments. As electronic warfare environments grow more contested, demand is rising for hardened, jam resistant radar altimeters that can operate reliably in high interference scenarios. These systems are increasingly specified as essential components in next generation combat, training, and unmanned air platforms, underpinning both survivability and operational effectiveness in demanding operational conditions.

2. Technology Impact in Defense Radar Altimeters Market

Technology is transforming defense radar altimeters from relatively basic height sensing instruments into sophisticated, multi mode, software defined sensors. Modern units leverage solid state transmitters, advanced digital signal processing, and narrow band or frequency modulated waveforms to improve accuracy, reduce susceptibility to jamming, and minimize interference with other onboard systems. These enhancements allow radar altimeters to operate reliably in dense electromagnetic environments, including near powerful radar and communications emitters.

Integration with digital flight control systems enables radar altimeters to support automated low level flight profiles, terrain following, and precise approach and landing modes, reducing pilot workload and improving safety in degraded visual conditions. Open architecture and modular designs support software updates and configuration changes, enabling the same basic hardware to be used across multiple platforms and mission profiles. Cybersecurity enhancements and secure data buses protect height related data streams from manipulation in networked combat environments. Miniaturization and reduced power consumption are also enabling deployment on smaller unmanned platforms and special mission pods, allowing precise altitude based maneuvers and standoff operations without exposing the host platform to direct threat. Collectively, these innovations enhance platform survivability, mission flexibility, and low level operational effectiveness.

3. Key Drivers in Defense Radar Altimeters Market

The defense radar altimeter market is driven by the continued importance of low level and nap of the earth flight as a core survivability tactic in contested airspaces. Modern fighters, attack aircraft, and special mission platforms rely on accurate, real time height above terrain data to fly beneath enemy radar coverage while maintaining safety margins over undulating or cluttered terrain. This requirement is further amplified by the proliferation of advanced integrated air defense systems, which push air forces to adopt more complex, terrain masking flight profiles supported by robust radar altimeters.

Another key driver is the growth of maritime and shipboard operations, where radar altimeters enable precise, low altitude approaches, carrier based landings, and hover and land sequences for rotary wing and special mission aircraft. The expansion of unmanned combat air and long endurance UAV programs also creates demand for compact, rugged radar altimeters that support autonomous terrain following and obstacle avoidance capabilities. Fleet modernization and life extension programs are accelerating the retrofit of legacy platforms with upgraded radar altimeter systems compatible with digital avionics, flight control laws, and electronic warfare suites. At the same time, interoperability and standardization requirements across allied forces are encouraging adoption of common radar altimeter interfaces and data formats, enabling shared logistics and training. Safety and certification standards reinforce the need for reliable, fault tolerant designs that minimize the risk of low altitude mishaps.

4. Regional Trends in Defense Radar Altimeters Market

Regionally, North America remains a leading hub for advanced radar altimeter development, supported by large scale fighter, attack, maritime patrol, and unmanned air programs that emphasize low level penetration and shipboard operations. The United States and its partners are investing in next generation platforms whose procurement contracts typically include integrated radar altimeters that support automated low level flight, maritime approaches, and electronic warfare resilient operation.

In Europe, collaborative combat air and multi role programs are favoring standardized radar altimeter architectures that support interoperability and shared certification bases across national fleets. The Asia Pacific region is witnessing rapid growth as several nations modernize their air forces and expand indigenous maritime strike and special mission capabilities, creating demand for domestically sourced or co developed radar altimeter solutions. Middle Eastern and Gulf states are investing in modernized or new build fleets whose radar altimeters must support low level over desert and maritime operations while resisting electronic warfare interference. Across these regions, there is a growing preference for compact, modular, open architecture radar altimeters that can be reused or upgraded across fixed wing, rotary wing, naval, and unmanned platforms. Domestic supply and technology sovereignty policies are also encouraging regional design and production, while export control and security regimes shape the deployment of high end altimeter variants.

5. Key Defense Radar Altimeters Market Program

Several flagship defense programs are shaping the evolution of the radar altimeter market over the 2026-2036 period. Next generation fighter and multi role combat air programs are specifying advanced radar altimeters that integrate tightly with digital flight control systems and mission computers, enabling automated low level penetration and terrain following capabilities in heavily defended airspace. Naval aviation and maritime strike programs are equipping carrier based and long range maritime platforms with radar altimeters that support precise over water flight profiles, automated approach sequences, and shipboard landing operations under adverse conditions.

Unmanned combat air and long endurance UAV programs are adopting radar altimeters to enable autonomous low level navigation, obstacle avoidance, and standoff orbiting, reducing exposure to integrated air defense systems. Rotary wing and special mission programs are relying on radar altimeters for nap of the earth insertions, mountainous terrain operations, and hover and land maneuvers in cluttered or maritime environments. Multinational and coalition level programs are standardizing radar altimeter interfaces and data formats, enabling shared software libraries, certification packages, and sustainment arrangements across partner nations. Through these programs, radar altimeters are evolving from simple height sensors into integrated, mission critical subsystems that underpin low level survivability, multi domain operations, and autonomous platform behavior.

Table of Contents

Defense Radar Altimeters Market - Table of Contents

Defense Radar Altimeters Market Report Definition

Defense Radar Altimeters Market Segmentation

By Region

By Platform

By Altitude Range

By Frequency Band

By Application

Defense Radar Altimeters Market Analysis for next 10 Years

The 10-year Defense Radar Altimeters Market analysis would give a detailed overview of Defense Radar Altimeters Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Radar Altimeters Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Radar Altimeters Market Forecast

The 10-year Defense Radar Altimeters Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Radar Altimeters Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Radar Altimeters Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Radar Altimeters Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Radar Altimeters Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports