|

시장보고서

상품코드

1996998

방위용 레이더 전원/프로세서 시장(2026-2036년)Global Defense Radar Power Supplies / Processors Market 2026-2036 |

||||||

세계의 방위용 레이더 전원/프로세서 시장

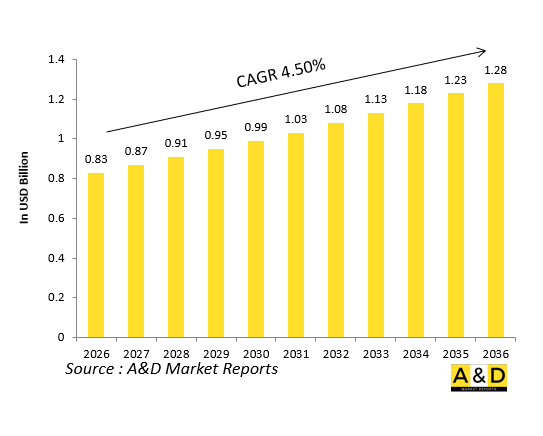

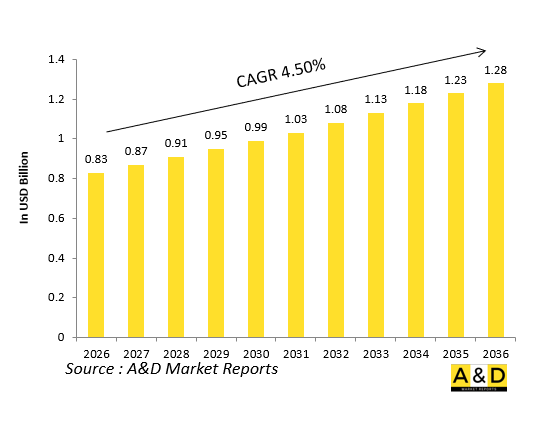

세계의 방위용 레이더 전원/프로세서 시장 규모는 2026년에 8억 3,000만 달러로 추계되고 있으며, 2026-2036년의 예측 기간에 CAGR 4.50%로 성장하며, 2036년에는 12억 8,000만 달러에 달할 것으로 전망되고 있습니다.

1. 소개:

국방용 레이더 전원/프로세서는 항공기, 함정, 지상 플랫폼에 탑재되는 군용 레이더 시스템에 안정적이고 고품질의 전력과 첨단 신호 연산을 제공하는 미션 크리티컬한 서브시스템입니다. 이러한 구성요소를 통해 능동형 전자식 스캐닝 어레이(AESA), 기계식 스캐닝 및 멀티모드 레이더는 장거리 감시, 추적, 사격통제, 전자전 감지 및 무인항공기 시스템(UAS) 대응 기능을 수행할 수 있습니다.

2026-2036년 고밀도 센서 어레이, 더 높은 전송 전력, 실시간 디지털 빔 포밍에 점점 더 의존하는 첨단 레이더 시스템에 대한 세계 수요가 증가함에 따라 시장이 확대될 것으로 예측됩니다. 레이더용 전원 공급 장치는 특히 항공기 및 이동식 플랫폼에서 엄격한 크기, 무게 및 열적 제약 속에서 엄격하게 제어된 고효율의 전력을 공급해야 합니다. 한편, 레이더용 프로세서는 복잡한 신호 처리 알고리즘, 데이터 융합 및 AI 지원 추적을 처리하여 원시 레이더 반사파를 실용적인 상황 인식 및 표적 데이터로 변환합니다. 이러한 하위 시스템들은 통합되어 현대 방공, 해상 감시 및 통합 항공전 관리 아키텍처의 핵심 구현 요소로 자리 잡고 있습니다.

2. 국방용 레이더 전원 공급 장치/프로세서 시장에서 기술의 영향력

기술은 국방용 레이더 전원 공급 장치 및 프로세서를 근본적으로 변화시키고 있으며, 고성능, 소형화 및 에너지 효율적인 레이더 시스템을 실현하고 있습니다. 현대의 레이더 전원 공급 장치는 고효율 토폴로지, 고급 열 관리 기술 및 질화갈륨(GaN)과 같은 광대역 갭 반도체 소자를 점점 더 많이 활용하여 제한된 플랫폼 인클로저 내에서 더 높은 출력의 전송 개구부를 지원합니다. 또한 이 전원 공급 장치는 고급 전력 관리 및 모니터링 기능을 통합하여 레이더 송수신 모듈 전체에서 실시간 부하 분산 및 고장 감지를 가능하게 합니다.

처리 측면에서는 멀티코어 및 매니코어 프로세서, 필드 프로그래머블 게이트 어레이(FPGA) 및 고급 신호 처리 아키텍처를 통해 복잡한 빔 포밍, 클러터 제거, 추적 필터를 실시간으로 구현할 수 있습니다. VPX 및 모듈형 개방형 시스템 접근법(MOSA)과 같은 개방형 표준을 통해 레이더의 라인 리플레이 서브 유닛 전체를 재설계하지 않고도 새로운 프로세서 및 전력 변환 하드웨어를 신속하게 도입할 수 있습니다. 디지털 빔포밍 및 병렬 처리 요구사항으로 인해, 안테나 어레이 근처에 배치할 수 있는 고처리량 및 저지연 상호연결 패브릭과 소형 저전력 레이더 프로세서에 대한 수요가 증가하고 있습니다. 이러한 발전은 우주 공간 및 전력 제약이 있는 플랫폼에 쉽게 통합할 수 있도록 하며, 레이더의 감도, 다중 목표 처리 능력 및 운영상의 내결함성을 종합적으로 향상시킵니다.

3. 국방용 레이더 전원 공급 장치/프로세서 시장의 주요 추진 요인

국방용 레이더 전원 공급 장치 및 프로세서 시장은 장거리 탐색, 추적, 사격 통제 및 전자전 센싱을 동시에 수행해야 하는 다중 임무 및 네트워크 중심 레이더 시스템으로의 세계 전환에 의해 주도되고 있습니다. 공군, 해군, 육군이 첨단 AESA 레이더와 대드론 레이더를 조달함에 따라 SWaP(크기, 무게, 전력 소비) 예산을 초과하지 않으면서도 훨씬 더 많은 양의 데이터를 처리할 수 있는 고효율 전원 솔루션과 고처리량 프로세서에 대한 수요가 증가하고 있습니다.

또 다른 주요 촉진요인은 첨단 전투기, 해군 함정 및 지상 배치형 방공 시스템의 보급입니다. 이러한 레이더 제품군은 열악한 환경과 진동 조건에서도 신뢰할 수 있고 견고한 전원 공급 장치와 실시간 처리가 필요합니다. 또한 함대 현대화 및 수명 연장 프로그램을 통해 전체 시스템을 재설계하지 않고도 소프트웨어 정의 모드, 디지털 빔 포밍, AI 지원 추적을 지원하기 위해 기존 레이더 프로세서 및 전원 조절 장치를 업그레이드하고 있습니다. 개방형 아키텍처 컴퓨팅과 모듈식 전력 변환 블록을 포함한 상호운용성 및 표준화 노력은 플랫폼과 군종 간 공통의 레이더용 전원 공급 장치 및 프로세서 구성 요소의 채택을 더욱 촉진하고 있습니다. 동시에 고밀도 전투 항공 및 해군 환경에서 열 관리 및 EMC(전자기 호환성)의 제약이 강화됨에 따라 통합되고 최적화된 레이더용 전원 및 처리 솔루션에 대한 수요가 증가하고 있습니다.

4. 방산용 레이더 전원공급장치/프로세서 시장의 지역별 동향

지역별로 보면 북미는 고성능 AESA 레이더와 멀티모드 레이더를 중시하는 대규모 전투기, 해군 및 지상 배치형 방공 프로그램에 힘입어 첨단 레이더 전력 및 처리 기술의 주요 거점 역할을 하고 있습니다. 미국과 파트너 국가들은 기능 밀도와 임무 유연성을 극대화하기 위해 GaN 기반 송신 모듈, 첨단 전력 변환 장치 및 고밀도 임베디드 프로세서를 긴밀하게 연계한 차세대 레이더 아키텍처에 투자하고 있습니다.

유럽에서는 공동 전투 항공 및 다목적 프로그램이 각국 함대 간의 상호 운용성과 물류 공유를 지원하는 모듈식 개방형 아키텍처의 레이더 전력 및 처리 솔루션에 대한 수요를 주도하고 있습니다. 아시아태평양에서는 여러 국가들이 방공 및 해상 감시 능력을 현대화하고 국산 레이더 및 반도체 생산을 확대하면서 국산 또는 공동 개발 레이더 전원 공급 장치 및 프로세서 모듈에 대한 수요가 빠르게 증가하고 있습니다. 중동 및 걸프 지역 국가들은 첨단 레이더를 탑재한 플랫폼에 투자하고 있으며, 전원 및 처리 서브시스템은 다목적 모드를 지원하면서 고온 및 고분진 환경에서도 안정적으로 작동할 수 있어야 합니다. 각 지역에서는 고정익, 회전익, 해군 및 지상 기반 플랫폼 간에 재사용 또는 업그레이드가 가능한 소형, 저 SWaP, 열적으로 최적화된 레이더용 전원 공급 장치 및 프로세서 유닛에 대한 수요가 증가하고 있습니다.

5. 주요 방산용 레이더 전원 공급 장치/프로세서 시장 프로그램

2026-2036년 몇 가지 주요 국방 프로그램이 레이더용 전원 공급 장치 및 프로세서 시장을 주도하고 있습니다. 차세대 전투기 계획은 GaN 기반 송수신 모듈을 밀집형 전력 제어 및 디지털 빔포밍 프로세서와 통합한 첨단 레이더 아키텍처를 규정하여 플랫폼 수준의 SWaP 요구 사항을 초과하지 않고 고출력 AESA 레이더를 구현합니다. 레이더를 실현하고 있습니다. 해군의 전투 항공 및 방공 프로그램에서는 장거리 감시, 미사일 추적, 다층 방어 작전을 지원하는 전력 변환 및 신호 처리 체인을 갖춘 강력한 멀티모드 레이더를 함정에 탑재하고 있습니다.

공중 조기경보 및 대(對)드론 레이더 프로그램은 소형, 저시인성 UAV 및 군집형 위협을 감지하고 추적하기 위해 소형, 고처리량 프로세서 카드와 효율적인 전원공급장치를 채택하고 있습니다. 지상 배치형 방공 및 광역 감시 프로그램에서는 다양한 임무와 위협에 따라 신속하게 재구성할 수 있는 모듈식 레이더 처리 및 전력 변환 랙에 대한 투자가 진행되고 있습니다. 다국적 및 연합 차원의 노력으로 레이더의 전원 공급 장치 및 프로세서 인터페이스, 개방형 아키텍처 폼팩터를 표준화하여 파트너 국가 간 물류, 소프트웨어 라이브러리 및 업그레이드 경로를 공유할 수 있도록 하고 있습니다. 이러한 프로그램을 통해 레이더용 전원 공급 장치와 프로세서는 단순한 배경 지원 구성 요소에서 공중, 육상, 해상에서 첨단 감지, 추적 및 전자전 능력의 핵심 추진 요소로 진화하고 있습니다.

목차

방위용 레이더 전원/프로세서 시장 - 목차

방위용 레이더 전원/프로세서 시장 보고서의 정의

방위용 레이더 전원/프로세서 시장 세분화

방위용 레이더 전원/프로세서 시장의 향후 10년간의 분석

세계의 방위용 레이더 전원/프로세서 시장 예측

지역 방위용 레이더 전원/프로세서 시장 동향과 예측

시장 예측과 시나리오 분석

방위용 레이더 전원/프로세서 시장의 국가별 분석

시장 예측과 시나리오 분석

방위용 레이더 전원/프로세서 시장의 기회 매트릭스

결론

KSA 26.04.20Global Defense Radar Power Supplies / Processors Market

The Global Defense Radar Power Supplies / Processors Market is estimated at USD 0.83 billion in 2026, projected to grow to USD 1.28 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.50% over the forecast period 2026-2036.

1. Introduction:

Defense radar power supplies and processors are mission critical subsystems that provide stable, high quality electrical power and advanced signal computation for military radar suites across airborne, naval, and ground platforms. These components enable active electronically scanned array (AESA), mechanically scanned, and multi mode radars to perform long range surveillance, tracking, fire control, electronic warfare sensing, and counter unmanned aircraft system functions.

Over the 2026-2036 horizon, the market is expanding alongside rising global demand for advanced radar systems, which increasingly rely on denser sensor arrays, higher transmit power apertures, and real time digital beamforming. Radar power supplies must deliver tightly regulated, high efficiency power within strict size, weight, and thermal constraints, particularly on aircraft and mobile platforms. Radar processors, meanwhile, handle complex signal processing algorithms, data fusion, and AI assisted tracking, transforming raw radar returns into actionable situational awareness and targeting data. Together, these subsystems are becoming central enablers of modern air defense, maritime surveillance, and integrated air battle management architectures.

2. Technology Impact in Defense Radar Power Supplies / Processors Market

Technology is fundamentally reshaping defense radar power supplies and processors, enabling more capable, compact, and energy efficient radar systems. Modern radar power supplies increasingly leverage high efficiency topologies, advanced thermal management techniques, and wide bandgap semiconductor devices such as gallium nitride (GaN) to support higher power transmit apertures within constrained platform envelopes. These supplies also integrate sophisticated power management and monitoring functions, allowing real time load balancing and fault detection across radar transmit/receive modules.

On the processing side, multi core and many core processors, field programmable gate arrays, and advanced signal processing architectures are enabling real time implementation of complex beamforming, clutter rejection, and tracking filters. Open standards such as VPX and modular open systems approaches (MOSA) allow rapid insertion of new processor and power conversion hardware without redesigning entire radar line replaceable units. Digital beamforming and parallel processing requirements are pushing demand for high throughput, low latency interconnect fabrics and compact, low power radar processors that can sit close to the antenna array. These advances collectively raise radar sensitivity, multi target capacity, and operational resilience while easing integration into space and power constrained platforms.

3. Key Drivers in Defense Radar Power Supplies / Processors Market

The defense radar power supply and processor market is driven by the global shift toward multi mission, network centric radar systems that must perform long range search, tracking, fire control, and electronic warfare sensing simultaneously. As air forces, navies, and armies procure advanced AESA and counter drone radars, demand rises for high efficiency power solutions and high throughput processors that can handle vastly greater data volumes without outstripping SWaP budgets.

Another key driver is the proliferation of advanced fighters, naval vessels, and ground based air defense systems whose radar suites require reliable, ruggedized power and real time processing under harsh environmental and vibration conditions. Fleet modernization and life extension programs are also driving upgrades to legacy radar processors and power regulation units to support software defined modes, digital beamforming, and AI assisted tracking without full system redesigns. Interoperability and standardization efforts, including open architecture computing and modular power conversion blocks, further encourage adoption of common radar power and processor building blocks across platforms and services. At the same time, tougher thermal management and EMC constraints in dense combat air and naval environments are reinforcing demand for integrated, optimized radar power and processing solutions.

4. Regional Trends in Defense Radar Power Supplies / Processors Market

Regionally, North America remains a leading hub for advanced radar power and processing technologies, supported by large scale fighter, naval, and ground based air defense programs that emphasize high performance AESA and multi mode radars. The United States and its partners are investing in next generation radar architectures whose design tightly couples GaN based transmit modules, advanced power conversion units, and high density embedded processors to maximize functional density and mission flexibility.

In Europe, collaborative combat air and multi role programs are driving demand for modular, open architecture radar power and processing solutions that support interoperability and shared logistics across national fleets. The Asia Pacific region is witnessing rapid growth as several nations modernize their air defense and maritime surveillance capabilities and expand indigenous radar and semiconductor production, creating demand for domestic or co developed radar power and processor modules. Middle Eastern and Gulf states are investing in advanced radar equipped platforms whose power and processing subsystems must operate reliably in high temperature and high dust environments while supporting multi mission modes. Across regions, there is a growing preference for compact, low SWaP, thermally optimized radar power and processor units that can be reused or upgraded across fixed wing, rotary wing, naval, and ground based platforms.

5. Key Defense Radar Power Supplies / Processors Market Program

Several flagship defense programs are shaping the radar power supply and processor market over the 2026-2036 horizon. Next generation fighter initiatives are specifying advanced radar architectures that integrate GaN based transmit/receive modules with tightly coupled power regulation and digital beamforming processors, enabling high power aperture AESA radars without exceeding platform level SWaP envelopes. Naval combat air and air defense programs are equipping ships with powerful multi mode radars whose power conversion and signal processing chains support long range surveillance, missile tracking, and layered defense operations.

Airborne early warning and counter drone radar programs are relying on compact, high throughput processor cards and efficient power supply units to detect and track small, low observable UAVs and swarming threats. Ground based air defense and wide area surveillance programs are investing in modular radar processing and power conversion racks that can be rapidly reconfigured for different missions and threats. Multinational and coalition level initiatives are standardizing radar power and processor interfaces and open architecture form factors, enabling shared logistics, software libraries, and upgrade paths across partner nations. Through these programs, radar power supplies and processors are evolving from background support components into central enablers of advanced sensing, tracking, and electronic warfare capabilities across the air, land, and sea domains.

Table of Contents

Defense Radar Power Supplies / Processors Market - Table of Contents

Defense Radar Power Supplies / Processors Market Report Definition

Defense Radar Power Supplies / Processors Market Segmentation

By Region

By Component

By Radar Type

By Platform

By Cooling

Defense Radar Power Supplies / Processors Market Analysis for next 10 Years

The 10-year Defense Radar Power Supplies / Processors Market analysis would give a detailed overview of Defense Radar Power Supplies / Processors Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Radar Power Supplies / Processors Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Radar Power Supplies / Processors Market Forecast

The 10-year Defense Radar Power Supplies / Processors Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Radar Power Supplies / Processors Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Radar Power Supplies / Processors Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Radar Power Supplies / Processors Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Radar Power Supplies / Processors Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports