|

시장보고서

상품코드

2023796

항공우주 및 방위 산업 구리 수요(2026-2036년)Global Copper demand in Aerospace & Defense Industry 2026-2036 |

||||||

세계의 항공우주 및 방위 산업 구리 수요

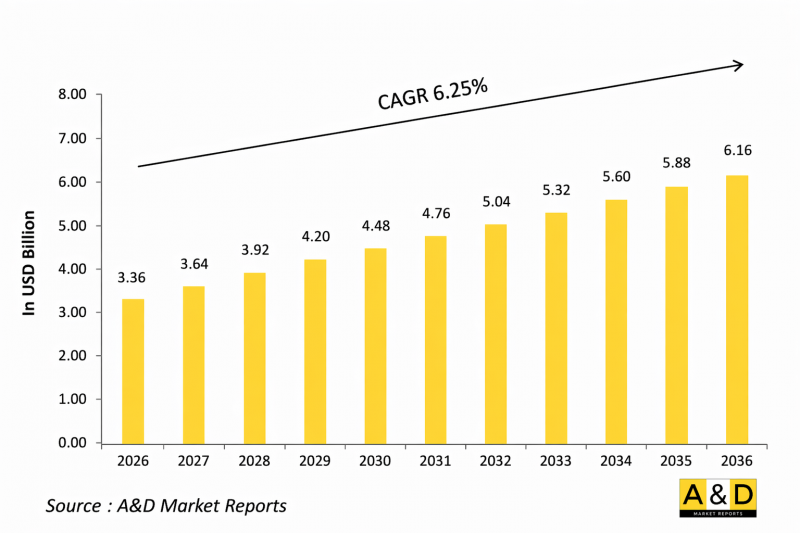

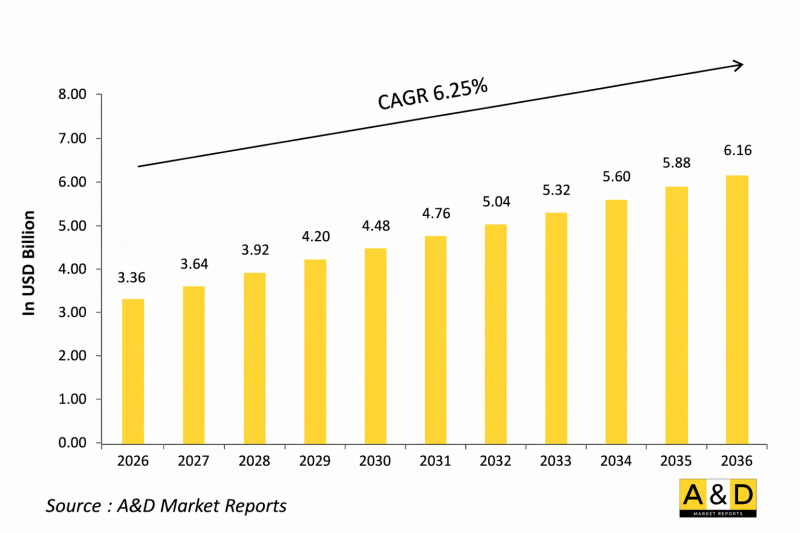

세계의 항공우주 및 방위 산업 구리 수요는 2026년 33억 6,000만 달러로 추정되며, 2026년부터 2036년까지 CAGR 6.25%로 성장하여 2036년에는 61억 6,000만 달러에 달할 것으로 예상됩니다.

1. 소개

항공우주 및 방위 산업에서 구리에 대한 세계 수요는 현대의 군사 및 항공 시스템에서 필수적인 요소로 자리 잡았습니다. 구리는 우수한 전기 전도성, 열효율, 내식성으로 인해 항공기, 선박, 지상 시스템 및 첨단 국방용 전자 장비에 필수적인 소재로 널리 평가받고 있습니다. 항공우주 플랫폼의 전동화 및 디지털 통합이 진행됨에 따라 구리 기반 부품에 대한 의존도가 계속 증가하고 있습니다. 와이어링 하니스 및 항공 전자기기에서 레이더 시스템, 통신 네트워크에 이르기까지 구리는 신뢰성과 성능을 보장하는 데 있어 기본적인 역할을 합니다. 또한, 첨단 소재 및 차세대 국방 기술로의 전환으로 고품질 전도성 소재의 중요성이 더욱 커지고 있습니다. 에너지 효율, 경량화 및 운영 능력 향상에 대한 관심이 높아지면서 구리의 활용이 더욱 촉진되고 있습니다. 전 세계 국방 현대화와 항공우주 분야의 혁신이 가속화됨에 따라, 구리에 대한 수요는 고성능 군사 및 항공 시스템의 진화를 뒷받침하는 중요한 요소로 남을 것으로 예상됩니다.

2. 세계의 항공우주 및 방위 산업 구리 수요에 미치는 기술적 영향

항공우주 및 방위 시스템 분야의 기술 발전은 다양한 응용 분야에서 구리에 대한 수요에 큰 영향을 미치고 있습니다. 전기화(more-electric) 및 완전 전기화(all-electric) 항공기의 개념이 채택됨에 따라 고성능 배선 및 배전 시스템에 대한 수요가 급증하고 있으며, 우수한 전기 전도성을 가진 구리가 여전히 선호되는 재료가 되고 있습니다. 첨단 항공전자, 레이더 시스템, 통신 기술은 안정적인 신호 전송과 시스템 효율을 보장하기 위해 구리 기반 부품에 크게 의존하고 있습니다. 또한 인공지능, 센서 네트워크, 전자전 시스템의 통합으로 인해 강력한 전기 인프라의 필요성이 증가하여 구리 소비를 더욱 촉진하고 있습니다.

또한, 지향성 에너지 무기, 고출력 컴퓨팅 시스템, 차세대 추진 기술의 등장으로 효율적인 열 관리 솔루션이 요구되고 있으며, 구리의 방열 특성이 매우 중요합니다. 경량 구리 합금 및 복합재료의 혁신으로 제조업체는 성능과 경량화의 균형을 맞출 수 있게 되었으며, 이는 항공우주 설계에서 중요한 고려 사항입니다. 국방 플랫폼의 기술이 고도화되고 상호연결성이 높아짐에 따라 구리는 현대 군사 생태계 전반에서 신뢰할 수 있고, 빠르고, 에너지 효율적인 운영을 실현하는 데 있어 핵심적인 역할을 계속하고 있습니다.

3. 세계의 항공우주 및 방위 산업 구리 수요의 주요 촉진요인

항공우주 및 방위 분야의 구리 수요를 견인하는 몇 가지 주요 요인이 있습니다. 주요 요인 중 하나는 항공기 및 방위 플랫폼의 전기화가 진행되고 있으며, 이를 위해서는 대규모 배선 시스템과 전기 부품이 필요합니다. 항공전자, 통신 시스템 및 미션 크리티컬한 전자기기의 복잡성이 증가함에 따라 신뢰할 수 있는 전도성 소재에 대한 수요는 더욱 증가하고 있습니다. 또한, 각국의 국방 현대화 프로그램은 기존 플랫폼을 첨단 전자 시스템으로 업그레이드하는 데 중점을 두고 있으며, 이로 인해 구리 소비가 증가하고 있습니다.

우주 탐사 계획과 위성 배치의 확대도 또 다른 중요한 요소입니다. 이러한 시스템은 전력 전송 및 열 관리에서 구리 기반 부품에 크게 의존하고 있기 때문입니다. 또한, 드론과 자율주행 차량을 포함한 무인 시스템의 부상으로 인해 컴팩트하고 효율적인 전기 시스템에 대한 수요가 증가하고 있습니다. 항공우주 설계에서 에너지 효율과 지속가능성에 대한 관심은 구리의 재활용 가능성과 성능상의 이점으로 인해 구리의 사용을 촉진하고 있습니다. 이러한 요인들이 복합적으로 작용하여, 항공우주 및 방위 산업 분야에서 구리에 대한 견조한 수요가 유지될 것으로 예상됩니다.

4. 세계의 항공우주 및 방위 산업 구리 수요 지역별 동향

항공우주 및 방위 산업의 지역별 구리 수요 동향은 기술 발전 정도, 방위비 지출, 산업 능력의 차이에 따라 달라집니다. 북미는 탄탄한 항공우주 제조 기반과 첨단 방위 기술에 대한 지속적인 투자로 인해 여전히 주요 지역으로 남아 있습니다. 유럽도 중요한 기여를 하는 지역으로, 잘 구축된 항공우주 산업과 공동 방위 이니셔티브가 구리 기반 시스템에 대한 꾸준한 수요를 견인하고 있습니다.

아시아태평양은 항공우주 역량 확대, 국방 예산 증가, 국내 제조 프로그램에 대한 투자 확대에 힘입어 급속한 성장세를 보이고 있습니다. 인도, 중국 등 국가들은 첨단 군사 플랫폼 개발 및 항공 분야 확대에 주력하고 있으며, 이는 구리 수요를 증가시키고 있습니다. 중동 지역도 국방 및 항공우주 인프라에 대한 투자를 점차 늘리고 있으며, 이는 지역 수요 확대에 기여하고 있습니다. 한편, 라틴아메리카와 아프리카는 신흥 시장으로, 첨단 기술의 점진적인 도입과 현대화 노력으로 항공우주 및 방위 산업 분야에서 구리에 대한 수요가 점차 증가하고 있습니다.

5. 세계의 항공우주 및 방위 산업 분야 주요 구리 수요 동향

항공우주 및 방위 산업의 구리 수요에 영향을 미치는 주요 프로그램은 현대화 이니셔티브, 첨단 항공기 개발 및 차세대 방위 시스템과 밀접한 관련이 있습니다. 전 세계 정부 및 방위 기관은 효율적인 전력 분배를 위해 구리 기반 전기 시스템에 크게 의존하는 '모어 일렉트릭' 항공기 개발에 투자하고 있습니다. 또한, 구형 플랫폼에 첨단 항공전자, 통신 시스템, 전자전 능력을 추가하는 군용 항공기의 업그레이드 프로그램도 수요를 견인하고 있습니다.

첨단 군함 및 잠수함 개발을 포함한 해군 현대화 프로그램도 전기 시스템 및 전력 관리 기술을 광범위하게 활용하기 때문에 구리에 대한 수요를 더욱 증가시키고 있습니다. 또한, 우주 탐사 프로그램 및 위성 배치 노력은 고성능 환경에서 구리를 사용할 수 있는 새로운 기회를 창출하고 있습니다. 무인 항공 시스템 및 자율 방위 플랫폼 개발도 구리에 대한 수요가 증가하고 있는 또 다른 중요한 분야입니다. 이 프로그램들은 모두 구리가 차세대 항공우주 및 국방 역량을 실현하는 데 있어 전략적으로 중요한 역할을 하고 있음을 강조하고 있습니다.

목차

항공우주 및 방산 시장에서의 구리 부품 - 목차

항공우주 및 방위 시장 보고서의 구리 부품 정의

항공우주 및 방위 산업 시장 세분화

향후 10년간의 항공우주 및 방위 산업 시장에서의 구리 부품 분석

세계 출입통제 시장 전망

지역별 출입통제 시장 동향 및 전망

시장 예측 및 시나리오 분석

출입통제 시장 국가별 분석

시장 예측 및 시나리오 분석

출입통제 시장 기회 매트릭스

결론

KSM 26.05.14Global Copper Demand in Aerospace & Defense Industry

The Global Copper demand in Aerospace & Defense Industry is estimated at USD 3.36 billion in 2026, projected to grow to USD 6.16 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 6.25% over the forecast period 2026-2036.

1. Introduction

The global copper demand in the aerospace and defense industry represents a vital component of modern military and aviation systems. Copper is widely valued for its excellent electrical conductivity, thermal efficiency, and corrosion resistance, making it indispensable in aircraft, naval vessels, ground systems, and advanced defense electronics. As aerospace platforms become increasingly electrified and digitally integrated, the reliance on copper-based components continues to expand. From wiring harnesses and avionics to radar systems and communication networks, copper plays a foundational role in ensuring reliability and performance. Additionally, the shift toward advanced materials and next-generation defense technologies has reinforced the importance of high-quality conductive materials. The growing emphasis on energy efficiency, lightweight systems, and enhanced operational capabilities further drives copper utilization. As global defense modernization and aerospace innovation accelerate, copper demand is expected to remain a critical factor in supporting the evolution of high-performance military and aviation systems.

2. Technology Impact in Global Copper Demand in Aerospace & Defense Industry

Technological advancements in aerospace and defense systems are significantly influencing the demand for copper across various applications. The increasing adoption of more-electric and all-electric aircraft concepts has led to a surge in demand for high-performance wiring and power distribution systems, where copper remains a preferred material due to its superior conductivity. Advanced avionics, radar systems, and communication technologies rely heavily on copper-based components to ensure stable signal transmission and system efficiency. Furthermore, the integration of artificial intelligence, sensor networks, and electronic warfare systems has expanded the need for robust electrical infrastructure, further strengthening copper consumption.

In addition, the emergence of directed energy weapons, high-power computing systems, and next-generation propulsion technologies requires efficient thermal management solutions, where copper's heat dissipation properties are critical. Innovations in lightweight copper alloys and composite materials are also enabling manufacturers to balance performance with weight reduction, a key consideration in aerospace design. As defense platforms become more technologically sophisticated and interconnected, copper continues to play a central role in enabling reliable, high-speed, and energy-efficient operations across modern military ecosystems.

3. Key Drivers in Global Copper Demand in Aerospace & Defense Industry

Several key factors are driving the demand for copper in the aerospace and defense sector. One of the primary drivers is the increasing electrification of aircraft and defense platforms, which requires extensive wiring systems and electrical components. The growing complexity of avionics, communication systems, and mission-critical electronics has further amplified the need for reliable conductive materials. Additionally, defense modernization programs across various countries are focusing on upgrading existing platforms with advanced electronic systems, thereby boosting copper consumption.

The expansion of space exploration initiatives and satellite deployment is another significant driver, as these systems depend heavily on copper-based components for power transmission and thermal management. Furthermore, the rise of unmanned systems, including drones and autonomous vehicles, has increased the demand for compact and efficient electrical systems. The emphasis on energy efficiency and sustainability in aerospace design is also encouraging the use of copper due to its recyclability and performance advantages. These combined factors are expected to sustain strong demand for copper in the evolving aerospace and defense landscape.

4. Regional Trends in Global Copper Demand in Aerospace & Defense Industry

Regional trends in copper demand within the aerospace and defense industry are shaped by varying levels of technological advancement, defense spending, and industrial capabilities. North America remains a leading region due to its strong aerospace manufacturing base and continuous investment in advanced defense technologies. Europe is also a significant contributor, with established aerospace industries and collaborative defense initiatives driving steady demand for copper-based systems.

The Asia-Pacific region is experiencing rapid growth, fueled by expanding aerospace capabilities, increasing defense budgets, and rising investments in indigenous manufacturing programs. Countries such as India and China are focusing on developing advanced military platforms and expanding their aviation sectors, which in turn boosts copper demand. The Middle East is gradually increasing its investments in defense and aerospace infrastructure, contributing to regional demand growth. Meanwhile, Latin America and Africa are emerging markets, with gradual adoption of advanced technologies and modernization efforts supporting incremental demand for copper in aerospace and defense applications.

5. Key Global Copper Demand in Aerospace & Defense Industry Program

Key programs influencing copper demand in the aerospace and defense industry are closely tied to modernization initiatives, advanced aircraft development, and next-generation defense systems. Governments and defense organizations worldwide are investing in the development of more-electric aircraft, which rely heavily on copper-based electrical systems for efficient power distribution. Military aircraft upgrade programs are also driving demand, as older platforms are retrofitted with advanced avionics, communication systems, and electronic warfare capabilities.

Naval modernization programs, including the development of advanced warships and submarines, further contribute to copper demand due to the extensive use of electrical systems and power management technologies. Additionally, space exploration programs and satellite deployment initiatives are creating new opportunities for copper utilization in high-performance environments. The development of unmanned aerial systems and autonomous defense platforms is another key area where copper demand is increasing. These programs collectively highlight the strategic importance of copper in enabling the next generation of aerospace and defense capabilities.

Table of Contents

Copper Component In The Aerospace And Defense Market - Table of Contents

Copper Component In The Aerospace And Defense Market Report Definition

Copper Component In The Aerospace And Defense Market Segmentation

By Component

By Process

By Region

By Alloy

Copper Component In The Aerospace And Defense Market Analysis for next 10 Years

The 10-year Copper Component In The Aerospace And Defense market analysis would give a detailed overview of Copper Component In The Aerospace And Defense market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Access Control Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Access Control Market Forecast

The 10-year access control market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Access Control Market Trends & Forecast

The regional access control market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Access Control Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Access Control Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Access Control Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports