|

시장보고서

상품코드

1998802

동물 건강 관리 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Animal Healthcare Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

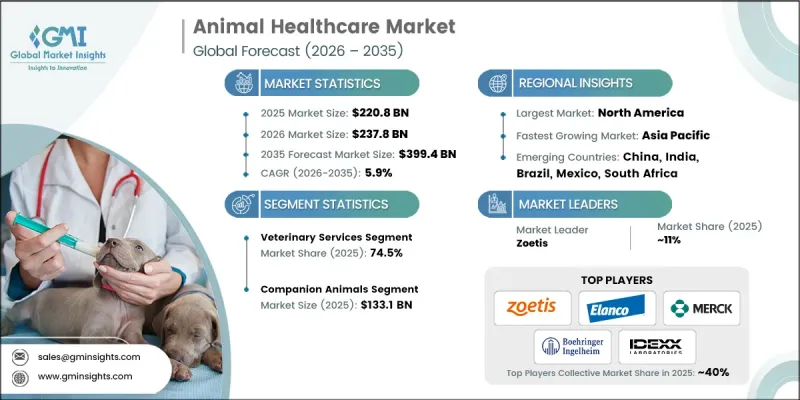

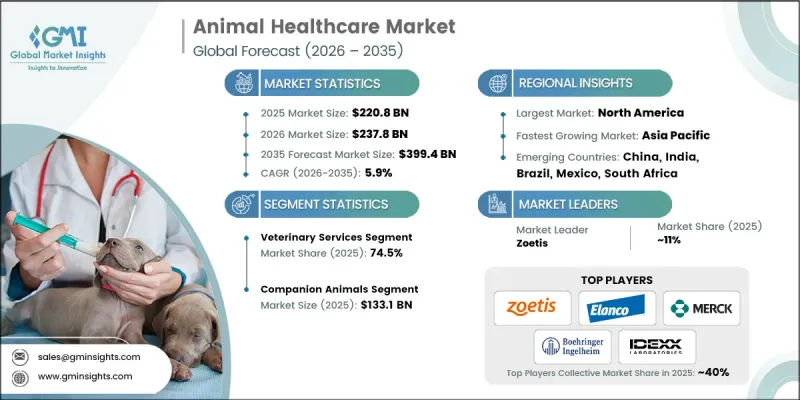

세계의 동물 건강 관리 시장은 2025년에 2,208억 달러로 평가되었고, CAGR 5.9%로 성장하여 2035년까지 3,994억 달러에 달할 것으로 예측됩니다.

시장의 성장은 고도의 수의학적 치료가 필요한 만성질환 및 감염성 질환을 포함한 동물 질병의 발생 증가에 영향을 받고 있습니다. 또한, 농업 현장, 주거 환경, 도시 생태계에서 인간과 동물의 접촉이 증가함에 따라 효과적인 동물 건강 관리의 중요성이 높아지고 있습니다. 동물 건강 관리 시장은 반려동물과 가축의 건강에 영향을 미치는 질병의 예방, 진단, 치료를 전문으로 하는 광범위한 세계 산업을 포괄합니다. 여기에는 동물의 건강을 보호하고 가축의 생산성을 지원하기 위해 고안된 동물용 의약품, 백신, 진단 솔루션, 약용 사료 첨가제, 의료기기 및 일회용품이 포함됩니다. 또한, 질병 관리의 개선은 인수공통전염병의 전파 위험을 감소시켜 공중보건 보호에도 기여합니다. 이 산업은 일반적인 치료법에서 보다 진보된 예방적이고 표적화된 헬스케어 솔루션으로 점차 전환하고 있습니다. 반려동물을 위한 생물학적 제제 및 특수 단일 클론 항체의 채택이 증가하는 한편, 가축의 건강 관리는 최신 백신 기술과 무리 단위의 질병 예방 전략에 의해 점점 더 많이 뒷받침되고 있습니다. 또한, 진단 능력과 바이오마커를 기반으로 한 검사가 더 광범위하게 사용 가능해짐에 따라, 수의사가 동물의 종 특성이나 특정 건강 상태에 따라 맞춤형 치료를 할 수 있는 개인 맞춤형 수의학도 주목받고 있습니다. 또한, 환자 친화적인 치료 옵션의 개발로 기존 투약 방법을 넘어선 치료의 가능성이 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 시점 시장 규모 | 2,208억 달러 |

| 예측액 | 3,994억 달러 |

| CAGR | 5.9% |

수의학 서비스 부문은 2025년 74.5%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 6%로 성장할 것으로 전망됩니다. 이러한 견고한 시장 동향은 주로 가처분 소득 증가와 전문 수의학에 대한 수요 증가에 의해 주도되고 있습니다. 동물의 건강과 복지에 대한 인식이 높아짐에 따라 더 많은 사람들이 반려동물을 위한 종합적인 수의학 서비스를 요구하고 있습니다. 또한, 수의학 기술의 발전으로 이 분야에서 이용할 수 있는 서비스의 범위가 확대되고 있습니다. 반려동물에 특화된 다양한 서비스를 보다 쉽게 이용할 수 있게 되어 동물병원 이용률 향상에 기여하고 있습니다. 현대 의료 기술의 통합과 서비스 제공의 개선은 전체 수의학 서비스 부문을 강화하고 시장의 지속적인 확장을 뒷받침하고 있습니다.

2025년 반려동물 부문은 1,331억 달러 시장 규모를 기록했습니다. 이 부문은 넓은 의미의 반려동물 인구 중 몇 가지 그룹으로 분류됩니다. 전 세계적으로 동물을 반려동물로 키우는 인구가 증가하고 있는 것이 이 부문의 성장을 뒷받침하는 주요 요인입니다. 현재 전 세계 많은 가정에서 동물을 반려동물로 키우고 있으며, 이는 수의학, 의료 제품 및 전문 의료 서비스에 대한 수요 증가에 기여하고 있습니다. 반려동물의 건강과 웰빙에 대한 지출 증가는 혁신적인 동물 건강 관리 솔루션의 개발 및 도입을 촉진하고 있습니다. 또한, 신흥국의 가처분 소득 증가로 인해 더 많은 반려동물 소유주들이 고급 건강관리 제품 및 수의학 서비스에 투자할 수 있게 되면서 반려동물 부문이 더욱 확대되고 있습니다.

2025년 기준, 북미 동물 건강 관리 시장은 38.5%의 점유율을 차지했습니다. 이 지역은 잘 구축된 수의학 인프라와 동수처리를 위한 첨단 의료 솔루션을 광범위하게 도입하여 선도적인 지위를 유지하고 있습니다. 반려동물과 가축 모두에서 혁신적인 치료제, 백신, 기생충 구제 제품이 적극적으로 활용되고 있는 것이 이 지역 시장 성장에 기여하고 있습니다. 북미는 또한 첨단 진단 기술과 정밀한 수의학적 접근법을 조기에 도입하여 혜택을 누리고 있습니다. 강력한 R&D 역량을 갖춘 주요 업계 참여자들이 존재함에 따라 이 지역의 혁신은 더욱 가속화되고 있습니다. 예방적 동물 건강관리에 대한 인식이 높아지고, 동물에게 영향을 미치는 만성질환과 인수공통전염병에 대한 우려가 커지면서 고급 수의학 서비스와 프리미엄 동물 건강 제품에 대한 수요가 지속적으로 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 제품별, 2022-2035

제6장 시장 추산 및 예측 : 동물 유형별, 2022-2035

제7장 시장 추산 및 예측 : 지역별, 2022-2035

제8장 기업 개요

LSH 26.04.23The Global Animal Healthcare Market was valued at USD 220.8 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 399.4 billion by 2035.

Market growth is influenced by the increasing occurrence of animal diseases, including both long-term health conditions and infectious illnesses that require advanced veterinary care. The rising interaction between humans and animals across agricultural settings, residential environments, and urban ecosystems has also elevated the importance of effective animal health management. The animal healthcare market encompasses a broad global industry dedicated to preventing, diagnosing, and treating medical conditions affecting both companion animals and livestock populations. It includes veterinary pharmaceuticals, vaccines, diagnostic solutions, medicated feed additives, medical equipment, and disposable supplies designed to protect animal health and support livestock productivity. In addition, improved disease control helps safeguard public health by reducing the risk of zoonotic disease transmission. The industry is gradually shifting away from generalized treatment methods toward more advanced preventive and targeted healthcare solutions. Increased adoption of biologics and specialized monoclonal antibodies for companion animals is becoming more common, while livestock healthcare is increasingly supported by modern vaccine technologies and herd-level disease prevention strategies. Personalized veterinary medicine is also gaining traction as diagnostic capabilities and biomarker-based testing become more widely available, allowing veterinarians to customize treatments based on species characteristics and specific health conditions. Furthermore, the development of patient-friendly therapeutic options is expanding treatment possibilities beyond conventional medication methods.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $220.8 Billion |

| Forecast Value | $399.4 Billion |

| CAGR | 5.9% |

The veterinary services segment held a 74.5% share in 2025 and is projected to grow at a CAGR of 6% throughout 2035. This strong market performance is largely driven by increasing disposable income levels and rising demand for professional veterinary care. Growing awareness about animal health and well-being has encouraged more individuals to seek comprehensive veterinary services for their animals. In addition, advancements in veterinary medical technologies have expanded the scope of services available within the sector. A wide range of pet-focused services has become more accessible, supporting higher utilization of veterinary facilities. The integration of modern healthcare technologies and improved service offerings is strengthening the overall veterinary services segment and supporting continued market expansion.

The companion animals segment generated USD 133.1 billion in 2025. This segment is categorized into several groups within the broader companion animal population. Rising global adoption of animals as household companions is a major factor supporting the growth of this segment. A significant portion of households worldwide currently care for animals as companions, contributing to increased demand for veterinary care, medical products, and specialized healthcare services. Higher spending on pet health and wellness is also encouraging the development and introduction of innovative animal healthcare solutions. In addition, growing disposable income levels in emerging economies are enabling more pet owners to invest in advanced healthcare products and veterinary services, further supporting the expansion of the companion animals segment.

North America Animal Healthcare Market held a 38.5% share in 2025. The region maintains a leading position due to its well-established veterinary healthcare infrastructure and widespread adoption of advanced medical solutions for animal care. Strong utilization of innovative therapeutics, vaccines, and parasite control products across both companion animal and livestock populations contributes to regional market growth. North America also benefits from the early implementation of advanced diagnostic technologies and precision veterinary healthcare approaches. The presence of major industry participants with strong research and development capabilities further accelerates innovation within the region. Growing awareness of preventive animal healthcare, along with increasing concern regarding chronic and zoonotic diseases affecting animals, continues to drive demand for advanced veterinary services and premium animal health products.

Key companies operating in the Global Animal Healthcare Market include Zoetis, Merck, Boehringer Ingelheim, Elanco Animal Health, Virbac, Vetoquinol, Ceva Sante Animale, Dechra Pharmaceuticals, IDEXX Laboratories, Phibro Animal Health, Neogen, HIPRA, B. Braun Vet Care (B Braun Melsungen), Symrise, Sklar Surgical Instruments, Medtronic, Endovac Animal Health, Indian Immunologicals, Kyoritsu Seiyaku, and Ourofino Saude Animal. Companies active in the Animal Healthcare Market are implementing several strategic approaches to strengthen their competitive position and expand their global footprint. A key focus area is investment in research and development aimed at introducing innovative veterinary pharmaceuticals, vaccines, and diagnostic technologies. Many organizations are also expanding their product portfolios through strategic partnerships, acquisitions, and collaborations with biotechnology firms and veterinary research institutions. Geographic expansion into emerging markets is another important strategy, as companies seek to capture rising demand for animal health products in developing regions. In addition, firms are enhancing digital capabilities by integrating data-driven diagnostics, tele-veterinary services, and advanced monitoring technologies into their offerings. Companies are also prioritizing sustainable production practices and regulatory compliance to maintain product credibility while supporting long-term growth in the animal healthcare market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Animal type trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing population of pet animals

- 3.2.1.2 Increasing support offered by government and public organizations for animal care

- 3.2.1.3 Growing demand for online veterinary pharmacies

- 3.2.1.4 Increase in animal healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with animal health drugs

- 3.2.2.2 Limited access in rural areas

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of telemedicine and remote veterinary consultation

- 3.2.3.2 Rising adoption of preventive and wellness-focused animal health solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape (Driven by Primary Research)

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory landscape (Driven by Primary Research)

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East and Africa

- 3.6 Reimbursement scenario (Driven by Primary Research)

- 3.7 Venture capitalist scenario in animal health industry

- 3.8 Economic impacts of the animal health industry

- 3.9 Consumer behaviour trends (Driven by Primary Research)

- 3.10 Future market trends (Driven by Primary Research)

- 3.11 Impact of AI and generative AI on the market

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Pharmaceuticals

- 5.2.1 Type

- 5.2.1.1 Drugs

- 5.2.1.1.1 Antiparasitic

- 5.2.1.1.2 Anti-inflammatory

- 5.2.1.1.3 Anti-infectives

- 5.2.1.1.4 Corticosteroids

- 5.2.1.1.5 Tranquilizers

- 5.2.1.1.6 Cardiovascular drugs

- 5.2.1.1.7 Gastrointestinal drugs

- 5.2.1.1.8 Other drugs

- 5.2.1.2 Vaccines

- 5.2.1.2.1 Modified live vaccines (MLV)

- 5.2.1.2.2 Killed inactivated vaccines

- 5.2.1.2.3 Other vaccines

- 5.2.1.3 Medicated feed additives

- 5.2.1.3.1 Antibiotics

- 5.2.1.3.2 Vitamins

- 5.2.1.3.3 Amino acids

- 5.2.1.3.4 Enzymes

- 5.2.1.3.5 Antioxidants

- 5.2.1.3.6 Prebiotics and probiotics

- 5.2.1.3.7 Minerals

- 5.2.1.3.8 Other medicated feed additives

- 5.2.1.1 Drugs

- 5.2.2 Indication

- 5.2.2.1 Dermatology

- 5.2.2.2 Cardiovascular diseases

- 5.2.2.3 Gastrointestinal diseases

- 5.2.2.4 Respiratory diseases

- 5.2.2.5 Other indications

- 5.2.3 Distribution channel

- 5.2.3.1 Veterinary hospital pharmacies

- 5.2.3.2 E-commerce

- 5.2.3.3 Retail pharmacies

- 5.2.1 Type

- 5.3 Medical devices

- 5.3.1 Veterinary diagnostic equipment

- 5.3.2 Anesthesia equipment

- 5.3.3 Patient monitoring equipment

- 5.3.4 Veterinary surgical equipment

- 5.3.5 Veterinary consumables

- 5.3.6 Other medical devices

- 5.4 Veterinary services

Chapter 6 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Companion animals

- 6.2.1 Dogs

- 6.2.2 Cats

- 6.2.3 Horses

- 6.2.4 Other companion animals

- 6.3 Livestock animals

- 6.3.1 Poultry

- 6.3.2 Swine

- 6.3.3 Cattle

- 6.3.4 Fish

- 6.3.5 Other livestock animals

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 GCC Countries

- 7.6.3 Israel

Chapter 8 Company Profiles

- 8.1 B. Braun Vet Care (B Braun Melsungen)

- 8.2 Boehringer Ingelheim

- 8.3 Ceva Sante Animale

- 8.4 Dechra Pharmaceuticals

- 8.5 Elanco Animal Health

- 8.6 Endovac Animal Health

- 8.7 HIPRA

- 8.8 IDEXX Laboratories

- 8.9 Merck

- 8.10 Medtronic

- 8.11 Neogen

- 8.12 Sklar Surgical Instruments

- 8.13 Symrise

- 8.14 Vetoquinol

- 8.15 Virbac

- 8.16 Zoetis

- 8.17 Phibro Animal Health

- 8.18 Indian Immunologicals

- 8.19 Kyoritsu Seiyaku

- 8.20 Ourofino Saude Animal