|

시장보고서

상품코드

1699329

해상 풍력에너지 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Offshore Wind Energy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

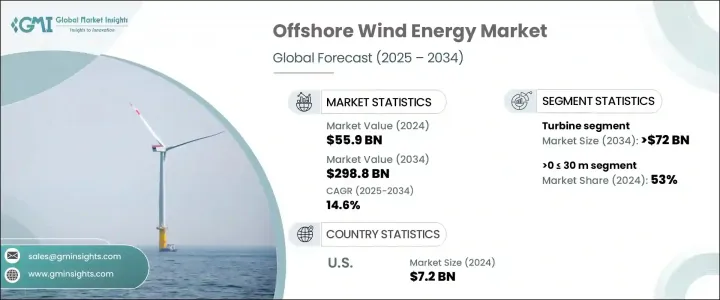

세계의 해상 풍력에너지 시장은 2024년에 559억 달러에 이르렀고, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 14.6%를 나타낼 것으로 예측됩니다.

급속한 산업화, 전력 수요의 급증, 이산화탄소 배출량의 억제라는 임박한 요구에 의해 해상 풍력에너지는 세계의 재생 가능 에너지의 중요한 구성 요소가 되고 있습니다. 우리는 고정 관세, 기술별 할당, 경쟁 경매 등 적극적인 정책과 인센티브를 실시했습니다.

터빈 기술의 진보, 송전망 인프라의 개선, 설치 비용의 저하는 시장의 기세를 더욱 가속화하고 있습니다. 고압직류(HVDC) 시스템과 하이브리드 변전소를 포함한 트랜스미션 인프라에 대한 투자는 에너지배급 효율을 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 559억 달러 |

| 예측 금액 | 2,988억 달러 |

| CAGR | 14.6% |

터빈 부문은 여전히 해상 풍력에너지 도입의 주요 추진력으로 2034년까지 720억 달러의 평가액이 예측되고 있습니다. 특히 풍속이 안정된 높은 고도로 바람의 섭취를 극대화하고 있습니다. 업계 전체가 발전전력량 1메가와트시당 비용 절감에 중점을 두고 있기 때문에 현재 진행 중인 R&D 이니셔티브에 의해 더욱 효율 향상이 예상됩니다.

해상 풍력 발전 프로젝트는 수심을 기준으로 0-30m, 30-50m, 50 m 초과의 세 가지 범주로 분류됩니다. 얕은 바다 부문은 비용면의 우위성과 설치 절차의 간소화로 2024년 시장 점유율 53%를 차지했습니다. 전소에 의한 교류(AC)와 직류(DC) 트랜스미션의 통합은 에너지 배급을 합리화하고 운용 효율을 한층 더 높입니다.

미국의 해상 풍력에너지 시장은 2024년에는 72억 달러에 이르렀으며, 북미가 세계의 16% 점유율을 차지했습니다. 기술 혁신으로 효율성이 향상되고 비용이 절감됨에 따라 해상 풍력은 실행 가능하고 확장 가능한 에너지 솔루션으로 부상하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장의 정의

- 기본 추정과 계산

- 예측 모델

- 1차 조사와 검증

- 시장 정의

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 전략 대시보드

- 혁신과 지속가능성의 전망

제5장 시장 규모와 예측 : 성분별(2021-2034년)

- 주요 동향

- 터빈

- 정격

- 2 MW 이하

- 2-5 MW

- 5-8 MW

- 8-10 MW

- 10-12 MW

- 12 MW 이상

- 설치

- 플로팅

- 축

- 수평

- 상풍

- 하풍

- 수직

- 수평

- 구성 요소

- 블레이드

- 타워

- 기타

- 축

- 고정

- 축

- 수평

- 상풍

- 하풍

- 수직

- 수평

- 구성 요소

- 블레이드

- 타워

- 기타

- 축

- 플로팅

- 정격

- 지지 구조물

- 하부 구조물(철골)

- 기초

- 모노 파일

- 자켓

- 기타

- 전기 인프라

- 전선 및 케이블

- 변전소

- 기타

- 기타

제6장 시장 규모와 예측 : 깊이별(2021-2034년)

- 주요 동향

- 0-30m

- 30-50m

- 50m 초과

제7장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 스페인

- 영국

- 프랑스

- 이탈리아

- 스웨덴

- 폴란드

- 덴마크

- 포르투갈

- 네덜란드

- 아일랜드

- 벨기에

- 아시아태평양

- 중국

- 인도

- 호주

- 일본

- 한국

- 베트남

- 필리핀

- 대만

- 세계 기타 지역

제8장 기업 프로파일

- Enessere

- Furukawa Electric

- General Electric

- Global Energy(Group)Limited

- Goldwind

- IMPSA

- LS Cable &System

- Nexans

- Nordex SE

- Prysmian Group

- Siemens Gamesa Renewable Energy

- Sumitomo Electric Industries

- Southwire Company

- Suzlon Energy Limited

- Vestas

- WEG

The Global Offshore Wind Energy Market reached USD 55.9 billion in 2024 and is projected to expand at a CAGR of 14.6% between 2025 and 2034. Rapid industrialization, surging electricity demand, and the pressing need to curb carbon emissions have positioned offshore wind energy as a critical component of the global renewable energy landscape. Governments worldwide are implementing aggressive policies and incentives to accelerate clean energy investments, including fixed tariffs, technology-specific quotas, and competitive auctions. These measures are driving industry expansion, reinforcing the role of offshore wind as a primary solution for sustainable energy generation.

Advancements in turbine technology, improvements in grid infrastructure, and declining installation costs are further fueling market momentum. Larger and more efficient wind turbines, enhanced by longer blades and taller towers, are optimizing energy capture and generation. These innovations not only improve operational efficiency but also reduce the levelized cost of energy (LCOE), making offshore wind increasingly competitive with traditional fossil fuels. Investments in transmission infrastructure, including high-voltage direct current (HVDC) systems and hybrid substations, are enhancing energy distribution efficiency. As governments ramp up their commitment to achieving net-zero carbon goals, the offshore wind sector is set to play a pivotal role in global energy transformation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $55.9 Billion |

| Forecast Value | $298.8 Billion |

| CAGR | 14.6% |

The turbine segment remains a key driver of offshore wind energy adoption, with projections indicating a valuation of USD 72 billion by 2034. The relentless push for renewable energy solutions is accelerating the development of high-capacity wind turbines capable of generating greater power output. Offshore installations with extended rotor diameters and optimized aerodynamic designs are maximizing wind capture, especially at higher altitudes where wind speeds are more consistent. With an industry-wide focus on reducing costs per megawatt-hour of electricity generated, ongoing research and development initiatives are expected to unlock further efficiency gains. As offshore wind farms continue to scale up in size and capacity, turbine technology will remain at the forefront of market expansion.

Offshore wind projects are classified based on depth into three categories: >0 <= 30 m, >30 <= 50 m, and >50 m. The shallow-water segment, covering depths of >0 <= 30 m, accounted for a 53% market share in 2024, driven by cost advantages and simplified installation procedures. Wind farms in shallow waters require less complex foundation engineering, enabling faster deployment and reduced capital expenditure. The integration of alternating current (AC) and direct current (DC) transmission systems through hybrid substations is streamlining energy distribution, further enhancing operational efficiencies. Given the financial and logistical benefits, developers are prioritizing shallow-water locations for offshore wind projects, ensuring sustained market expansion in the coming years.

The US offshore wind energy market reached USD 7.2 billion in 2024, with North America capturing a 16% share of the global industry. The region's growth trajectory is fueled by supportive regulatory frameworks, significant investments in offshore wind infrastructure, and a growing commitment to decarbonization. As technological innovations drive efficiency improvements and cost reductions, offshore wind is emerging as a viable and scalable energy solution. With increasing project approvals and ongoing infrastructure development, North America is set to become a key player in the global offshore wind energy sector over the next decade.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Component, 2021 – 2034 (MW & USD Million)

- 5.1 Key trends

- 5.2 Turbine

- 5.2.1 Rating

- 5.2.1.1 ≤ 2 MW

- 5.2.1.2 >2≤ 5 MW

- 5.2.1.3 >5≤ 8 MW

- 5.2.1.4 >8≤10 MW

- 5.2.1.5 >10≤ 12 MW

- 5.2.1.6 > 12 MW

- 5.2.2 Installation

- 5.2.2.1 Floating

- 5.2.2.1.1 Axis

- 5.2.2.1.1.1 Horizontal

- 5.2.2.1.1.1.1 Up wind

- 5.2.2.1.1.1.2 Down wind

- 5.2.2.1.1.2 Vertical

- 5.2.2.1.1.1 Horizontal

- 5.2.2.1.2 Component

- 5.2.2.1.2.1 Blades

- 5.2.2.1.2.2 Towers

- 5.2.2.1.2.3 Others

- 5.2.2.1.1 Axis

- 5.2.2.2 Fixed

- 5.2.2.2.1 Axis

- 5.2.2.2.1.1 Horizontal

- 5.2.2.2.1.1.1 Up wind

- 5.2.2.2.1.1.2 Down wind

- 5.2.2.2.1.2 Vertical

- 5.2.2.2.1.1 Horizontal

- 5.2.2.2.2 Component

- 5.2.2.2.2.1 Blades

- 5.2.2.2.2.2 Towers

- 5.2.2.2.2.3 Others

- 5.2.2.2.1 Axis

- 5.2.2.1 Floating

- 5.2.1 Rating

- 5.3 Support Structure

- 5.3.1 Substructure (Steel)

- 5.3.2 Foundation

- 5.3.2.1 Monopile

- 5.3.2.2 Jacket

- 5.3.3 Others

- 5.4 Electrical Infrastructure

- 5.4.1.1 Wires & cables

- 5.4.1.2 Substation

- 5.4.1.3 Others

- 5.5 Others

Chapter 6 Market Size and Forecast, By Depth, 2021 – 2034 (MW & USD Million)

- 6.1 Key trends

- 6.2 > 0 to ≤ 30 m

- 6.3 > 30 to ≤ 50 m

- 6.4 > 50 m

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (MW & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Spain

- 7.3.3 UK

- 7.3.4 France

- 7.3.5 Italy

- 7.3.6 Sweden

- 7.3.7 Poland

- 7.3.8 Denmark

- 7.3.9 Portugal

- 7.3.10 Netherlands

- 7.3.11 Ireland

- 7.3.12 Belgium

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Australia

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Vietnam

- 7.4.7 Philippines

- 7.4.8 Taiwan

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 Enessere

- 8.2 Furukawa Electric

- 8.3 General Electric

- 8.4 Global Energy (Group) Limited

- 8.5 Goldwind

- 8.6 IMPSA

- 8.7 LS Cable & System

- 8.8 Nexans

- 8.9 Nordex SE

- 8.10 Prysmian Group

- 8.11 Siemens Gamesa Renewable Energy

- 8.12 Sumitomo Electric Industries

- 8.13 Southwire Company

- 8.14 Suzlon Energy Limited

- 8.15 Vestas

- 8.16 WEG