|

시장보고서

상품코드

1716627

망막모세포종 치료 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Retinoblastoma Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

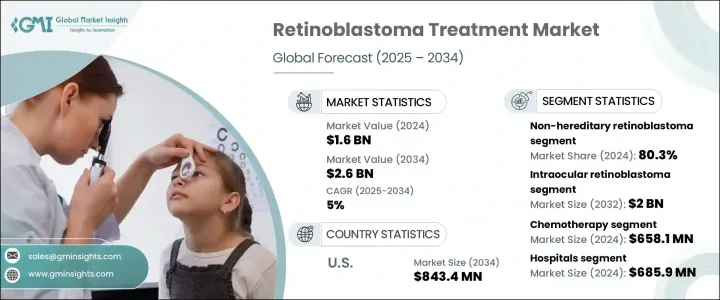

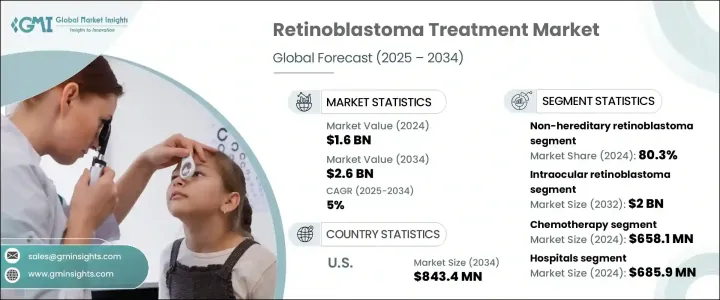

세계의 망막모세포종 치료 시장은 2024년에 16억 달러로 평가되었으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5%를 나타낼 것으로 예측됩니다.

이 성장은 주로 망막모세포종의 발생률 증가, 표적요법의 진보 증가, 눈종양학에 있어서의 지속적인 기술 혁신에 의해 초래됩니다. 효과적인 치료 전략의 필요성은 전례 없이 높아지고 있습니다.

세계 정부 및 의료기관은 조기 진단을 촉진하기 위한 계발 캠페인을 시작하여 생존율을 대폭 향상시키고 있습니다. 게다가, 안과 종양학에서 인공지능의 통합은 전문의가 망막모세포종을 조기에 발견하고 치료효과를 향상시키는 데 도움이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 16억 달러 |

| 예측 금액 | 26억 달러 |

| CAGR | 5% |

망막모세포종 치료 시장은 안내망막모세포종과 안외망막모세포종으로 구분됩니다. 유리체강 내 및 동맥 내 화학 요법에 대한 선호도가 증가하면서 이 부문의 성장에 크게 기여하고 있는데, 이러한 방법은 기존 화학 요법에 비해 전신 독성을 줄이는 데 도움이 되기 때문입니다.

최종 용도별로는 병원이 망막모세포종 치료 시장을 독점하여 2024년에는 6억 8,590만 달러를 창출했습니다. 센터가 병원내에 통합된 것으로, 치료에의 액세스가 향상해, 병원은 망막모세포종 관리의 중요한 담당자로서 자리매김되고 있습니다. 의료기관이 최첨단의 기술과 치료 프로토콜을 채용하고 있는 것으로부터, 병원 부문은 향후 수년간에 걸쳐 지속적인 성장을 나타낼 것으로 예측됩니다.

미국의 망막모세포종 치료 시장은 2024년에 5억 2,550만 달러를 창출했는데, 증례 증가는 소아에 있어서의 RB1 유전자 변이의 유병률 증가에 기인한 것입니다. 미국의 주요 의료 서비스 제공업체는 환자의 결과를 개선하기 위해 새로운 치료, 임상시험 및 소아 종양 전문센터에 투자하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 망막모세포종의 발생률 증가

- 망막모세포종의 조기 진단과 치료

- 업계의 잠재적 위험 및 과제

- 높은 치료비

- 망막모세포종 치료에 따른 부작용

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 전망

- 향후 시장 동향

- 갭 분석

- 특허 분석

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 질환 유형별(2021-2034년)

- 주요 동향

- 비유전성 망막모세포종

- 유전성 망막모세포종

제6장 시장 추계·예측 : 질환 단계별(2021-2034년)

- 주요 동향

- 안구 내 망막모세포종

- 안구 외 망막모세포종

제7장 시장 추계·예측 : 치료 유형별(2021-2034년)

- 주요 동향

- 화학 요법

- 방사선 요법

- 수술 요법

- 레이저 요법

- 동결 요법

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 암 치료 센터

- 전문 안과 클리닉

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Advancium Health

- Baxter International

- Bristol-Myers Squibb Company

- Cadila Pharmaceuticals

- Cellceutix Corporation

- GlaxoSmithKline

- Johnson &Johnson

- Merck &Co.

- Novartis

- Pfizer

- Teva Pharmaceutical Industries

- Theriva Biologics

The Global Retinoblastoma Treatment Market was valued at USD 1.6 billion in 2024 and is projected to grow at a CAGR of 5% between 2025 and 2034. This growth is primarily driven by the rising incidence of retinoblastoma, increasing advancements in targeted therapies, and continuous innovations in ocular oncology. With the prevalence of this rare but serious eye cancer rising among children, the need for effective treatment strategies has never been more critical. Research institutions and pharmaceutical companies are aggressively investing in the development of novel therapies that can enhance patient outcomes while minimizing adverse effects.

Governments and healthcare organizations worldwide are launching awareness campaigns to promote early diagnosis, significantly improving survival rates. The availability of advanced treatment modalities, including intra-arterial chemotherapy and intravitreal chemotherapy, is transforming the landscape of retinoblastoma management. Emerging technologies, such as gene therapy and precision medicine, are further driving optimism in the market. Additionally, the integration of artificial intelligence in ocular oncology is helping specialists detect retinoblastoma at earlier stages, improving treatment efficacy. With major hospitals and cancer centers expanding pediatric oncology units, access to specialized retinoblastoma care is becoming more widespread, fueling market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 5% |

The market for retinoblastoma treatment is segmented into intraocular and extraocular retinoblastoma. The intraocular segment is expected to generate USD 2 billion by 2032, driven by the rising incidence of intraocular retinoblastoma cases and the growing adoption of innovative treatment methods. The increasing preference for intravitreal and intra-arterial chemotherapy is significantly contributing to this segment's growth, as these methods help reduce systemic toxicity compared to traditional chemotherapy. Patients and healthcare providers are actively seeking treatment options that offer improved efficacy while minimizing long-term side effects, which is further propelling market demand.

In terms of end-use, hospitals dominated the retinoblastoma treatment market, generating USD 685.9 million in 2024. With hospitals making significant investments in oncology and specialized pediatric ophthalmology units, multidisciplinary teams comprising ophthalmologists, genetic specialists, and oncologists are collaborating to develop targeted treatment approaches. The integration of chemotherapy centers within hospital settings is enhancing treatment accessibility, positioning hospitals as key players in retinoblastoma management. As medical institutions continue to adopt cutting-edge technologies and treatment protocols, the hospital segment is set to witness sustained growth over the coming years.

U.S. retinoblastoma treatment market generated USD 525.5 million in 2024, with rising cases attributed to the increasing prevalence of RB1 gene mutations among children. The National Cancer Institute and the American Cancer Society are actively promoting early detection initiatives through awareness campaigns, which are accelerating the demand for advanced treatment options. Leading healthcare providers across the U.S. are investing in novel therapies, clinical trials, and specialized pediatric oncology centers to improve patient outcomes. With continued advancements in precision medicine and targeted treatment approaches, the U.S. is expected to remain a dominant player in the global retinoblastoma treatment market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° Synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of retinoblastoma

- 3.2.1.2 Early diagnosis and treatment of retinoblastoma

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Side effects associated with retinoblastoma treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Patent analysis

- 3.9 Pipeline analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Non-hereditary retinoblastoma

- 5.3 Hereditary retinoblastoma

Chapter 6 Market Estimates and Forecast, By Disease Stage, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Intraocular retinoblastoma

- 6.3 Extraocular retinoblastoma

Chapter 7 Market Estimates and Forecast, By Treatment Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Chemotherapy

- 7.3 Radiation therapy

- 7.4 Surgery

- 7.5 Laser therapy

- 7.6 Cryotherapy

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Cancer treatment center

- 8.4 Specialty eye clinics

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Advancium Health

- 10.2 Baxter International

- 10.3 Bristol-Myers Squibb Company

- 10.4 Cadila Pharmaceuticals

- 10.5 Cellceutix Corporation

- 10.6 GlaxoSmithKline

- 10.7 Johnson & Johnson

- 10.8 Merck & Co.

- 10.9 Novartis

- 10.10 Pfizer

- 10.11 Teva Pharmaceutical Industries

- 10.12 Theriva Biologics