|

시장보고서

상품코드

1913381

산업용 3D 프린터 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)Industrial 3D Printer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

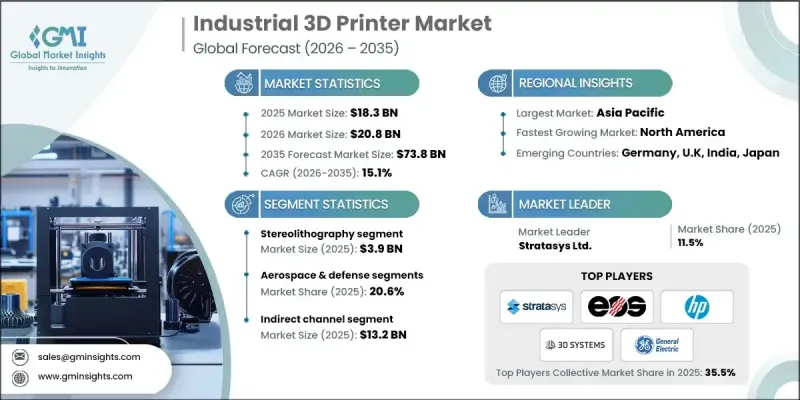

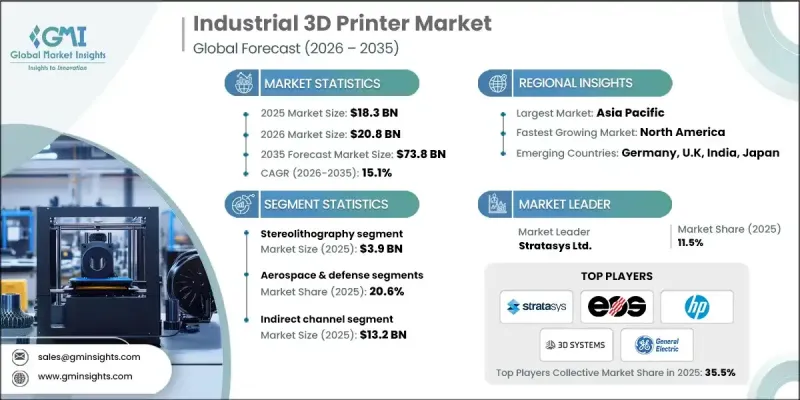

세계의 산업용 3D 프린터 시장은 2025년 183억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 15.1%로 성장할 전망이며, 738억 달러에 이를 것으로 예측됩니다.

비용 효율성은 시장 성장을 이끌어내는 주요 요인으로, 제조업체는 금형 비용을 최대 80-90% 절감할 수 있으며, 특정 용도에서는 소량 생산 시에도 부품당 10만 달러 이상의 절약으로 이어집니다. 이 시장은 고도로 맞춤화된 기하학적으로 복잡한 부품을 생산할 수 있는 3D 인쇄 기술로부터 혜택을 누리고 있습니다. 의료 분야에서는 환자 특이적인 임플란트를 제공하고 회복 성과 향상에 기여하고 있습니다. 재료 효율 및 지속가능성도 중요한 역할을 하고 있으며, 3D 프린팅은 용도에 따라 폐기물을 30-95% 삭감합니다. 금속 적층 성형 및 멀티 머티리얼 인쇄와 같은 기술 혁신은 새로운 산업 이용 사례를 가능하게 함으로써 시장을 더욱 확대하고 있습니다. 정부 이니셔티브 및 자금 지원 프로그램은 특히 정밀성과 고급 재료 성능이 필요한 이용 사례에서 조사 및 도입을 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 당초 시장 규모 | 183억 달러 |

| 시장 규모 예측 | 738억 달러 |

| CAGR | 15.1% |

스테레오 리소그래피(SLA)는 2025년 39억 달러 시장 규모를 창출했습니다. SLA는 매우 정밀한 복잡한 프로토타입과 기능 부품을 생산할 수 있어 복잡한 설계가 필요한 산업에 이상적입니다. 정부의 자금 원조나 시책에 의해 산업 분야에서의 채용이 진행되어, 특수한 SLA 수지 및 특정 용도에 있어서의 기술 혁신이 촉진되고 있습니다.

항공우주 및 방위 분야는 2025년에 20.6%의 점유율을 차지했습니다. 경량화, 연료 효율, 기하학적으로 고급 부품에 대한 수요가 배경에 있습니다. 적층 조형 기술은 종래 기술로는 실현 불가능한 격자 구조나 컨포멀 냉각 채널의 제조를 가능하게 해, 항공우주 및 방위 분야를 산업용 3D 프린팅의 주요 도입 분야로서 확고한 지위에 밀어 올리고 있습니다.

미국의 산업용 3D 프린터 시장은 2025년에 78.1%의 점유율을 차지했습니다. 이 성장은 견고한 제조거점과 첨단 기술의 급속한 도입으로 지원됩니다. 스트라타시스나 3D 시스템즈 등 주요 기업은 항공우주 및 의료 등 고정밀 분야 수요에 부응하기 위해 제품 라인을 확충하고, 주요 제조업체와의 제휴에 의해 3D생산 라인의 규모 확대를 추진함으로써 미국 시장의 성장을 견인하고 있습니다.

자주 묻는 질문

목차

제1장 분석 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계의 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 래피드 프로토타이핑의 광범위한 활용

- 제품 개발 및 공급망 개선

- 3D 프린팅 프로젝트에 대한 정부 투자

- 업계의 잠재적 위험 및 과제

- 재료의 제약 및 품질 관리

- 3D 프린팅 기술에 의한 설계의 복제 용이성

- 시장 기회

- 의료 분야 및 바이오프린팅에 대한 전개

- 지속가능성 및 규제 준수 솔루션

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술 및 혁신 동향

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 기술별

- 지역별

- 규제 상황

- 규격 및 컴플라이언스 요건

- 지역별 규제 프레임워크

- 인증 기준

- 갭 분석

- 리스크 평가 및 경감책

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업별 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 동향

- 기업 합병 및 인수(M&A)

- 사업 제휴 및 협력

- 신제품 발매

- 확대 계획

제5장 시장의 추정 및 예측 : 기술별(2022-2035년)

- 선택적 레이저 소결법

- 스테레오 리소그래피

- 용융 적층법

- 직접 금속 레이저 소결

- 잉크젯 인쇄

- 폴리젯 인쇄

- 전자빔 용해

- 적층 물체 제조

- 디지털 광처리 기술

- 레이저 금속 적층법

- 기타

제6장 시장의 추정 및 예측 : 최종 사용자별(2022-2035년)

- 자동차

- 항공우주 및 방위

- 의료

- 소비자용 전자 기기

- 식품 및 요리

- 전력 및 에너지

- 기타

제7장 시장의 추정 및 예측 : 유통 채널별(2022-2035년)

- 직접

- 간접

제8장 시장의 추정 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- 3D Systems

- Desktop Metal

- EOS

- Formlabs

- General Electric

- HP

- Markforged

- Materialise

- Nano Dimension

- Prodways

- Renishaw

- SLM Solutions

- Stratasys

- Ultimaker

- Velo3D

The Global Industrial 3D Printer Market was valued at USD 18.3 billion in 2025 and is estimated to grow at a CAGR of 15.1% to reach USD 73.8 billion by 2035.

Cost efficiency remains a key factor driving market growth, with manufacturers able to reduce tooling costs by up to 80-90%, translating into savings of over USD 100,000 per part in certain applications, even for limited production runs. The market benefits from 3D printing's ability to produce highly customized and geometrically complex components. In the healthcare sector, companies are delivering patient-specific implants, enhancing recovery outcomes. Material efficiency and sustainability also play a crucial role, as 3D printing reduces waste by 30-95% depending on the application. Technological innovations, including metal additive manufacturing and multi-material printing, are further broadening the market by enabling new industrial use cases. Government initiatives and funding programs are supporting research and adoption, particularly for applications requiring precision and advanced material capabilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18.3 Billion |

| Forecast Value | $73.8 Billion |

| CAGR | 15.1% |

The stereolithography (SLA) generated USD 3.9 billion in 2025. SLA enables the production of highly intricate prototypes and functional parts with exceptional precision, making it ideal for industries that demand complex designs. Its industrial adoption is bolstered by government funding and initiatives, fostering innovation in specialized SLA resins and targeted applications.

The aerospace and defense sector held 20.6% share in 2025, driven by the need for lightweight, fuel-efficient, and geometrically sophisticated components. Additive manufacturing allows production of lattice structures and conformal cooling channels that are impossible to achieve with conventional techniques, cementing aerospace and defense as a leading adopter of industrial 3D printing.

United States Industrial 3D Printer Market held 78.1% share in 2025. The growth is supported by a strong manufacturing base and rapid adoption of advanced technologies. Leading companies such as Stratasys and 3D Systems have propelled the U.S. market by expanding their portfolios to meet the demands of high-precision sectors, including aerospace and healthcare, and collaborating with major manufacturers to scale 3D production lines.

Key players in the Global Industrial 3D Printer Market include HP, Markforged, Nano Dimension, Prodways, SLM Solutions, 3D Systems, Stratasys, EOS, General Electric, Formlabs, Ultimaker, Velo3D, and Materialise. Companies in the Global Industrial 3D Printer Market are strengthening their position through several strategic initiatives. They are heavily investing in R&D to enhance precision, material versatility, and production speed. Partnerships with OEMs and industry leaders enable large-scale adoption of 3D printing technologies. Firms focus on expanding regional distribution networks and service infrastructure to improve accessibility and customer support. They are also introducing software solutions for process optimization and workflow integration. Emphasis on sustainability, including reducing material waste and energy consumption, helps companies meet regulatory requirements and attract environmentally conscious clients.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 End use

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Wide use of rapid prototyping

- 3.2.1.2 Improvements in product development and supply chains

- 3.2.1.3 Government investments in 3D printing projects

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Material limitations and quality control

- 3.2.2.2 Ease of replicating designs with 3D printing technology

- 3.2.3 Opportunities

- 3.2.3.1 Expansion into healthcare and bioprinting

- 3.2.3.2 Sustainability and regulatory compliance solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By technology

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Gap analysis

- 3.9 Risk assessment and mitigation

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Technology, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Selective laser sintering

- 5.3 Stereolithography

- 5.4 Fuse deposition modeling

- 5.5 Direct metal laser sintering

- 5.6 Inkjet printing

- 5.7 Polyjet printing

- 5.8 Electron beam melting

- 5.9 Laminated object manufacturing

- 5.10 Digital light processing

- 5.11 Laser metal deposition

- 5.12 Others

Chapter 6 Market Estimates & Forecast, By End-User, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automotive

- 6.3 Aerospace & defense

- 6.4 Healthcare

- 6.5 Consumer electronics

- 6.6 Food & culinary

- 6.7 Power & energy

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Direct

- 7.3 Indirect

Chapter 8 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3D Systems

- 9.2 Desktop Metal

- 9.3 EOS

- 9.4 Formlabs

- 9.5 General Electric

- 9.6 HP

- 9.7 Markforged

- 9.8 Materialise

- 9.9 Nano Dimension

- 9.10 Prodways

- 9.11 Renishaw

- 9.12 SLM Solutions

- 9.13 Stratasys

- 9.14 Ultimaker

- 9.15 Velo3D

(주말 및 공휴일 제외)