|

시장보고서

상품코드

2019059

정맥주사액 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Intravenous Solutions Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

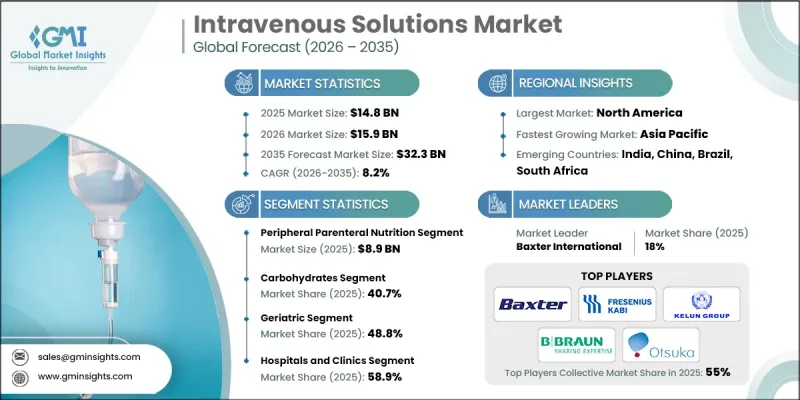

세계의 정맥주사액 시장은 2025년에 148억 달러로 평가되었으며, CAGR 8.2%로 성장하여 2035년까지 323억 달러에 달할 것으로 추정됩니다.

이 시장의 성장은 영양실조 유병률의 증가와 신흥국과 선진국 모두에서 전문적인 영양 지원에 대한 요구가 증가함에 따라 주도되고 있습니다. 비경구영양(PN)을 포함한 정맥주사는 필수 영양소, 수분 및 전해질을 혈류에 직접 공급하는 데 매우 중요한 역할을 하며, 특히 경구로 영양분을 섭취하거나 흡수할 수 없는 환자들에게 매우 중요한 역할을 합니다. 또한, 의료진이 오염 및 준비 오류의 위험을 최소화하고 환자의 안전과 업무 효율성을 향상시키면서 미리 혼합되어 바로 사용할 수 있는 정맥주사제를 선호하는 것도 수요를 촉진하고 있습니다. 또한, 제형 기술의 발전과 적절한 시기에 영양 중재의 중요성에 대한 인식이 높아짐에 따라 병원과 클리닉에서는 신생아 의료, 중환자 치료, 종양학, 만성질환 관리에 정맥 수액을 도입하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 시작 시점 시장 규모 | 148억 달러 |

| 예측 규모 | 323억 달러 |

| CAGR | 8.2% |

말초정맥영양(PPN) 부문은 2025년 89억 달러의 시장 규모를 기록했습니다. PPN은 단기간의 영양 지원이 필요한 환자에게 널리 사용되며, 아미노산, 포도당, 지질 등 중요한 주요 영양소를 말초 정맥을 통해 공급합니다. 이 요법은 경구 또는 장내 섭취가 제한된 환자에서 영양 균형을 회복하고, 추가적인 영양소 소모를 방지하며, 결핍증을 개선하는 데 도움이 됩니다. 임상 연구에 따르면, PPN을 적시에 투여하면 환자의 결과와 만족도가 향상되는 것으로 나타났습니다. PPN의 정밀한 배합은 환자가 필요한 미량영양소와 다량 영양소를 적절한 비율로 섭취할 수 있도록 하여 합병증 위험을 줄이고 회복 기간 동안 신진대사를 안정적으로 유지하도록 돕습니다. 병원에서는 중환자실이나 수술 현장에서 영양 지원을 유지하기 위한 안전하고 효율적인 방법으로 PPN 제제에 대한 의존도가 높아지고 있습니다.

2025년에는 탄수화물 부문이 40.7%의 점유율을 차지하며 주요 기여 요인으로 자리 잡았습니다. 포도당 기반 정맥 수액은 경구 또는 경장영양으로 충분한 칼로리를 섭취할 수 없는 환자에게 필수적인 에너지를 공급합니다. 이 수액은 세포의 에너지 수요를 지원하고, 제지방 체중 감소를 방지하며, 중증 환자나 영양실조 환자의 대사 균형을 유지합니다. 탄수화물이 풍부한 정맥 주사액의 사용은 에너지 수요가 높고 적시에 영양 공급이 필수적인 중환자실, 외과 병동 및 신생아 치료에서 특히 중요합니다. 의료진은 환자 개개인의 필요에 따라 정확하게 투여할 수 있는 포도당 함유 용액을 선호하고 있으며, 이는 현대의 비경구 영양 요법에서 필수적인 요소로 자리 잡았습니다.

북미 정맥주사액 시장은 2025년에 가장 큰 시장 점유율을 차지했습니다. 이는 높은 의료 인프라, 높은 수술 건수, 다양한 의료 현장에서의 비경구 영양 및 정맥 수액 요법의 광범위한 활용에 힘입은 바 큽니다. 미국과 캐나다의 병원, 진료소, 외래 환자 센터, 그리고 확대되는 재택 의료 서비스는 정맥주사 솔루션에 대한 지속적인 수요를 창출하고 있습니다. 이 지역은 미국 FDA와 캐나다 보건부가 주도하는 강력한 규제 프레임워크의 혜택을 받고 있으며, 무균성, 표시, 품질 관리 및 GMP(Good Manufacturing Practice) 준수에 대한 엄격한 기준을 시행하고 있습니다. 이러한 규제는 환자의 안전, 일관된 제품 품질 및 신뢰할 수 있는 공급망을 보장합니다. 또한, 병원 내 기술 도입, 첨단 임상 프로토콜 및 즉시 사용 가능한 프리믹스 수액 도입으로 업무 효율성이 향상되고 임상적 실수를 최소화하여 북미 수액 시장에서 북미의 우위를 더욱 공고히 하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 유형별, 2022-2035

제6장 시장 추정 및 예측 : 조성별, 2022-2035

제7장 시장 추정 및 예측 : 연령층별, 2022-2035

제8장 시장 추정 및 예측 : 용도별, 2022-2035

제9장 시장 추정 및 예측 : 최종 용도별, 2022-2035

제10장 시장 추정 및 예측 : 지역별, 2022-2035

제11장 기업 개요

KSM 26.05.06The Global Intravenous Solutions Market was valued at USD 14.8 billion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 32.3 billion by 2035.

The market growth is fueled by the rising prevalence of malnutrition and an increasing need for specialized nutrition support across both emerging and developed regions. Intravenous solutions, including parenteral nutrition (PN), play a critical role in delivering essential nutrients, hydration, and electrolytes directly into the bloodstream, particularly for patients who cannot ingest or absorb nutrients orally. The demand is also driven by healthcare providers' preference for pre-mixed, ready-to-use IV solutions, which minimize the risks of contamination and preparation errors while enhancing patient safety and operational efficiency. In addition, advancements in formulation technology and increasing awareness of the importance of timely nutritional intervention have encouraged hospitals and clinics to adopt IV solutions for neonatal, critical care, oncology, and chronic disease management.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.8 Billion |

| Forecast Value | $32.3 Billion |

| CAGR | 8.2% |

The peripheral parenteral nutrition (PPN) segment generated USD 8.9 billion in 2025. PPN is widely used for patients requiring short-term nutritional support, delivering vital macronutrients like amino acids, dextrose, and lipids through peripheral veins. The solution helps restore nutrient balance, prevent further nutritional depletion, and correct deficiencies in patients with limited oral or enteral intake. Clinical studies indicate that the timely administration of PPN improves patient outcomes and satisfaction. The precise formulation of PPN ensures that patients receive the necessary micromolecules and macromolecules in the right proportion, reducing the risk of complications and supporting metabolic stability during recovery periods. Hospitals increasingly rely on PPN solutions as a safe, efficient method to maintain nutritional support in critical care and surgical settings.

The carbohydrates segment accounted for 40.7% share in 2025, establishing the segment as a key contributor. Dextrose-based IV solutions provide essential energy for patients who cannot obtain adequate calories orally or through enteral feeding. These solutions support cellular energy requirements, prevent the breakdown of lean body mass, and maintain metabolic balance in critically ill and malnourished patients. The use of carbohydrate-enriched IV fluids is particularly critical in intensive care units, surgical wards, and neonatal care, where energy demands are high and timely nutrient delivery is essential. Clinicians favor dextrose-containing solutions because they can be accurately dosed to meet individual patient needs, making them indispensable in modern parenteral nutrition therapy.

North America Intravenous Solutions Market held the largest market share in 2025, driven by advanced healthcare infrastructure, high surgical procedure volumes, and widespread use of parenteral nutrition and IV fluid therapy across multiple care settings. Hospitals, clinics, ambulatory centers, and expanding home healthcare services in the U.S. and Canada have created sustained demand for intravenous solutions. The region benefits from a strong regulatory framework, led by the U.S. FDA and Health Canada, which enforces rigorous standards for sterility, labeling, quality control, and GMP compliance. These regulations ensure patient safety, consistent product quality, and reliable supply chains. Additionally, technological adoption in hospitals, advanced clinical protocols, and integration of ready-to-use pre-mixed IV solutions enhance operational efficiency and minimize clinical errors, further consolidating North America's dominance in the intravenous solutions market.

Key players operating in the Global Intravenous Solutions Market include Baxter International, B. Braun Melsungen, Fresenius Kabi, Grifols, ICU Medical, AdvaCare Pharma, JW Life Science, Otsuka Pharmaceutical, Aculife Healthcare, Amanta Healthcare, Albert David, Axa Parenterals, and Haisco Pharmaceutical Group. Companies in the Intravenous Solutions Market strengthen their presence by focusing on developing pre-mixed, ready-to-use formulations that reduce contamination risk and enhance operational efficiency. They invest in advanced manufacturing technologies to improve sterility, stability, and shelf life. Strategic collaborations with hospitals, clinics, and home healthcare providers help expand distribution networks and increase product adoption. Market leaders also prioritize regulatory compliance, leveraging certifications from U.S. FDA, Health Canada, and other authorities to build trust and maintain quality standards. Additionally, companies emphasize product innovation, offering customized nutrient compositions tailored for neonatal, critical care, and oncology patients.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.3 Type trends

- 2.4 Compositions trends

- 2.5 Age group trends

- 2.6 Application trends

- 2.7 End use trends

- 2.8 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing cases of malnutrition

- 3.2.1.2 High prevalence of pre-term births

- 3.2.1.3 Increasing prevalence of diseases, such as gastrointestinal disorder, neurological diseases, and cancer

- 3.2.1.4 Increasing number of surgical procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory and quality requirements

- 3.2.3 Market opportunity

- 3.2.3.1 Rising shift toward home-based and outpatient infusion care

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.1.1 Ready-to-use (RTU) premixed solutions

- 3.5.1.2 Personalized IV nutrition formulations

- 3.5.2 Emerging technologies

- 3.5.2.1 Shift toward oral rehydration therapy

- 3.5.2.2 Multi-chamber and self-compounding bags

- 3.5.1 Current technologies

- 3.6 Future market trends (Driven by Primary Research)

- 3.7 Patent analysis (Driven by Primary Research)

- 3.8 Impact of AI and generative AI on the market (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Total parenteral nutrition

- 5.3 Peripheral parenteral nutrition

Chapter 6 Market Estimates and Forecast, By Composition, 2022 - 2035 ($ Mn and Units)

- 6.1 Key trends

- 6.2 Carbohydrates

- 6.3 Vitamins and minerals

- 6.4 Single-dose amino acids

- 6.5 Parenteral lipid emulsion

- 6.6 Other compositions

Chapter 7 Market Estimates and Forecast, By Age Group, 2022 - 2035 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adults

- 7.4 Geriatric

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Nutritional support

- 8.3 Blood transfusion

- 8.4 Fluid and electrolyte balance

- 8.5 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Ambulatory surgery centers

- 9.4 Home care settings

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aculife Healthcare

- 11.2 AdvaCare Pharma

- 11.3 Albert David

- 11.4 Amanta Healthcare

- 11.5 Axa Parenterals

- 11.6 B. Braun Melsungen

- 11.7 Baxter International

- 11.8 CSL

- 11.9 Fresenius Kabi

- 11.10 Grifols

- 11.11 Haisco Pharmaceutical Group

- 11.12 ICU Medical

- 11.13 JW Life Science

- 11.14 Kelun Industry Group

- 11.15 Otsuka Pharmaceutical