|

시장보고서

상품코드

1850617

건식 진공 펌프 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Dry Vacuum Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

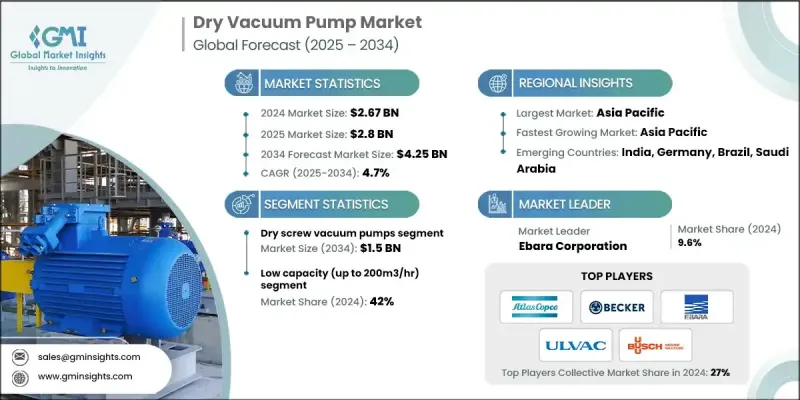

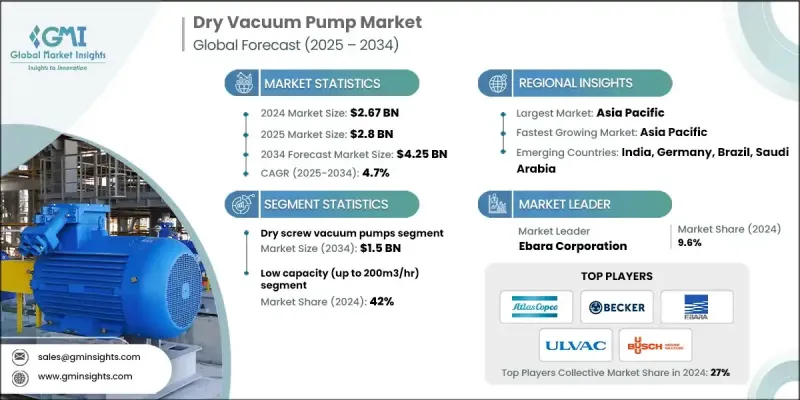

건식 진공 펌프 세계 시장은 2024년에 26억 7,000만 달러로 평가되었고 CAGR 4.7%로 성장하여 2034년에는 42억 5,000만 달러에 이를 것으로 예측되고 있습니다.

전자, 항공우주, 자동차 등 산업 제조의 급증은 성형, 코팅, 재료 운송과 같은 공정에서 건식 진공 펌프 수요를 계속 추진하고 있습니다. 제약 및 생명 공학 산업은 멸균, 동결 건조 및 용매 회수 작업에서 이러한 펌프가 필수적이기 때문에 시장 성장을 뒷받침하고 있습니다. 식품 및 음료 분야도 진공포장 및 식품 가공에 있어서 깨끗하고 오일 프리 시스템에 대한 요구가 높아지고 있기 때문에 채택을 뒷받침하고 있습니다. 한편, 화학 제조업체는 유지 보수가 용이한 설계와 오염이 없는 조작성을 통해 건식 진공 솔루션을 지원합니다. 자동화와 디지털화로의 전환이 진행됨에 따라 제조업체는 스마트 시스템을 진공 시스템에 통합하고 실시간 모니터링, 데이터 분석 및 예측 유지 보수를 제공하여 가동 시간과 효율성을 향상시키는 방향으로 있습니다. 2단 시스템은 보다 깊은 진공 레벨을 필요로 하는 용도에서 인기를 끌고 있습니다. 건식 진공 펌프는 에너지 효율, 내구성 및 환경 친화적인 조작성으로 인해 여러 응용 분야에서 오일 기반 시스템을 대체하는 것이 더 깨끗하고 안정적인 진공 기술을 요구하는 업계 전반에 걸쳐 매력적인 선택입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 26억 7,000만 달러 |

| 예측 금액 | 42억 5,000만 달러 |

| CAGR | 4.7% |

건식 스크류 진공 펌프 분야는 반도체 제조, 야금 및 화학 생산에서 높은 채택률에 힘입어 2034년까지 15억 달러의 매출이 예상됩니다. 건식 스크류 진공 펌프는 오염되지 않은 고진공 레벨과 고속 펌핑을 제공합니다. 에너지 효율적인 운전은 특히 전력 소비와 운전 경비 절감을 목표로 하는 시설에 있어서 중요한 이점입니다. 견고한 설계와 운전 간격 연장으로 유지보수 필요성을 줄이고 가동 시간을 향상시킬 수 있으므로 대량의 연속 사용 용도에 이상적입니다. 이 부문의 성장은 수요가 높은 환경에서 지속 가능하고 효율적인 장비를 선호하는 경향이 강해지고 있음을 반영합니다.

저속(200m3/hr까지) 부문은 정밀하고 컴팩트하며 에너지 효율적인 솔루션을 필요로 하는 용도으로 인해 2024년에는 42%의 점유율을 차지했습니다. 이 부문은 연구실, 소규모 제약 생산, 분석 장비, 전자 장비 제조 등에서 널리 채택됩니다. 펌프의 인기는 오염 방지 및 신뢰성이 중요한 환경에서 깨끗하고 오일이없는 성능을 제공할 수 있기 때문입니다. 컴팩트한 설계, 낮은 유지 보수 및 비용 효율적인 운전으로 인해 이러한 펌프는 제한된 공간에서의 설치 및 간헐적인 사용에 적합합니다.

북미의 건식 진공 펌프 시장은 2034년까지 10억 7,000만 달러에 이를 것으로 예측됩니다. 제약 및 생명공학의 상황은 동결건조 및 무균 포장과 같은 공정이 오염이 없는 환경을 필요로 하는 주요 추진력입니다. 엄격한 산업 규제에 대한 대응과 이 지역의 생물 제제 제조 확대는 이러한 시스템에 대한 수요를 강화하고 있습니다. 높은 생산 기준, R&D 투자 증가, 프로세스 무결성에 대한 강한 관심은 북미 시설 전체의 성장을 지원하는 중요한 요소입니다.

건조 진공 펌프 산업을 형성하는 주요 제조업체는 Edwards Vacuum, Ebara Corporation, ULVAC, Becker Vacuum Pumps, Atlas Copco, Welch Vacuum, Agilent Technologies, Grundfos, Alfa Laval, Leibold GmbH, KNF Neuberger, Flowserve Corporation, Tuthill Corporation, DEK 드라이진공펌프를 선도하는 제조업체는 그 지위를 강화하기 위해 에너지 효율적인 기술 혁신에 주력하고 진화하는 업계 수요에 부응하기 위해 제품 라인을 확대하고 있습니다. 대부분은 자동화 기능을 갖춘 스마트팜프 시스템에 투자하여 사용자가 실시간 성능 데이터 및 예측 유지 보수 도구에 액세스할 수 있도록 합니다. 또한 각 회사는 전략적 제휴와 파트너십을 맺고 특히 고성장 지역에서 판매망을 강화하고 있습니다. 지속적인 R&D 노력으로 개선된 진공 레벨, 보다 조용한 작동, 긴 서비스 수명의 펌프가 개발되었습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 기회

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신규 기술

- 가격 동향

- 지역별

- 펌프유형별

- 규제 상황

- 표준 및 컴플라이언스 요건

- 지역 규제 틀

- 인증기준

- 무역 통계(HS코드 841410)

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정 및 예측 : 펌프 유형별, 2021-2034

- 주요 동향

- 드라이 스크류 진공 펌프

- 드라이 스크롤 진공 펌프

- 드라이 다이어프램 펌프

- 드라이 클로 & 훅 펌프

- 기타

제6장 시장 추정 및 예측 : 용량별, 2021-2034

- 주요 동향

- 저(최대 200m3/시)

- 중(200-500m3/시)

- 고(500m3/시 이상)

제7장 시장 추정 및 예측 : 최종 이용 산업별, 2021-2034

- 주요 동향

- 일렉트로닉스 및 반도체

- 의약품

- 화학 및 석유화학

- 석유 및 가스

- 식음료

- 기타

제8장 시장 추정 및 예측 : 유통채널별, 2021-2034

- 주요 동향

- 직접 판매

- 간접 판매

제9장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Agilent Technologies

- Atlas Copco

- Becker Vacuum Pumps

- Busch Vacuum Solutions

- Ebara Corporation

- Flowserve Corporation

- Graham Corporation

- Ingersoll Rand Inc

- Kashiyama Industries

- Orion Machinery

- Osaka Vacuum

- Schmalz Group

- Shinko Seiki

- ULVAC

- Unozawa

The Global Dry Vacuum Pumps Market was valued at USD 2.67 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 4.25 billion by 2034.

The surge in industrial manufacturing across electronics, aerospace, and automotive continues to fuel demand for dry vacuum pumps in processes such as molding, coating, and material transport. Pharmaceutical and biotech industries boost market growth, as these pumps are essential in sterilization, freeze-drying, and solvent recovery operations. The food and beverage sector is also driving adoption due to growing requirements for clean, oil-free systems in vacuum packaging and food processing. Meanwhile, chemical companies favor dry vacuum solutions for their maintenance-friendly designs and contamination-free operation. The increasing shift toward automation and digitalization pushes manufacturers to integrate smart features in vacuum systems, offering real-time monitoring, data analytics, and predictive maintenance to improve uptime and efficiency. Two-stage systems are gaining popularity in applications needing deeper vacuum levels. Dry vacuum pumps replace oil-based systems in several applications due to their energy efficiency, durability, and environmentally friendly operation, making them an attractive choice across industries seeking cleaner and more reliable vacuum technology.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.67 Billion |

| Forecast Value | $4.25 Billion |

| CAGR | 4.7% |

The dry screw vacuum pumps segment is expected to generate USD 1.5 billion by 2034, fueled by high adoption across semiconductor fabrication, metallurgy, and chemical production. These pumps deliver high vacuum levels and fast pumping speeds without contamination. Their energy-efficient operation is a key benefit, especially for facilities aiming to reduce power consumption and operational expenses. The robust design and extended service intervals lead to reduced maintenance needs and enhanced uptime, making them ideal for high-volume, continuous-use applications. This segment's growth reflects an increasing preference for sustainable and efficient equipment in high-demand environments.

The low (up to 200m3/hr) segment held a 42% share in 2024 owing to the applications requiring precise, compact, and energy-efficient solutions. This segment is widely adopted across laboratories, small-scale pharmaceutical production, analytical instrumentation, and electronics manufacturing. Its popularity stems from the pumps' ability to deliver clean, oil-free performance in environments where contamination control and reliability are critical. Compact design, low maintenance, and cost-effective operation make these pumps suitable for limited-space installations and intermittent-use scenarios.

North America Dry Vacuum Pumps Market is projected to reach USD 1.07 billion by 2034. The pharmaceutical and biotechnology landscape is a major driver, where processes like freeze-drying and aseptic packaging require contamination-free environments. Compliance with stringent industry regulations and the expansion of biologics manufacturing in the region are strengthening demand for these systems. High production standards, rising R&D investments, and a strong focus on process integrity are key factors supporting growth across North American facilities.

The key manufacturers shaping the Dry Vacuum Pumps Industry include Edwards Vacuum, Ebara Corporation, ULVAC, Becker Vacuum Pumps, Atlas Copco, Welch Vacuum, Agilent Technologies, Grundfos, Alfa Laval, Leybold GmbH, KNF Neuberger, Flowserve Corporation, Tuthill Corporation, DEKKER Vacuum Technologies, and Graham Corporation. To strengthen their position, leading dry vacuum pump manufacturers are focusing on innovation in energy-efficient technologies and expanding their product lines to meet evolving industry demands. Many are investing in smart pump systems with automation features, enabling users to access real-time performance data and predictive maintenance tools. Companies are also entering strategic alliances and partnerships to enhance distribution networks, particularly in high-growth regions. Continuous R&D efforts are developing pumps with improved vacuum levels, quieter operation, and longer service life.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Pump type

- 2.2.3 Capacity

- 2.2.4 End use industry

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By pump type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code-841410)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Pump Type, 2021-2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Dry screw vacuum pump

- 5.3 Dry scroll vacuum pump

- 5.4 Dry diaphragm pump

- 5.5 Dry claw and hook pumps

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Low (Up to 200m3/hr)

- 6.3 Mid (200-500 m3/hr)

- 6.4 High (More than 500 m3/hr)

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Electronics and semiconductors

- 7.3 Pharmaceutical

- 7.4 Chemical and petrochemical

- 7.5 Oil and gas

- 7.6 Food and beverages

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Agilent Technologies

- 10.2 Atlas Copco

- 10.3 Becker Vacuum Pumps

- 10.4 Busch Vacuum Solutions

- 10.5 Ebara Corporation

- 10.6 Flowserve Corporation

- 10.7 Graham Corporation

- 10.8 Ingersoll Rand Inc

- 10.9 Kashiyama Industries

- 10.10 Orion Machinery

- 10.11 Osaka Vacuum

- 10.12 Schmalz Group

- 10.13 Shinko Seiki

- 10.14 ULVAC

- 10.15 Unozawa