|

시장보고서

상품코드

1797859

디젤 발전기 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Diesel Gensets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

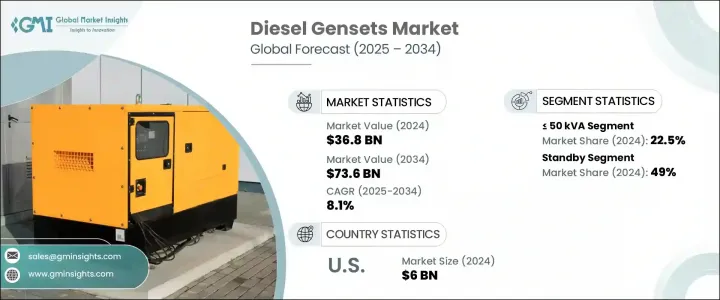

세계의 디젤 발전기 시장 규모는 2024년 368억 달러에 달하고, CAGR 8.1%로 성장하여 2034년까지 736억 달러에 이를 것으로 예측됩니다.

이 시장의 확대는 특히 주택, 상업, 산업 부문 전체에서 신뢰할 수 있는 백업 전력에 대한 수요가 증가하고 있는데, 특히 전력망이 불안정하거나 빈번하게 중단되는 지역에 있습니다. 디젤 발전기는 이러한 지역에서 즉시 전력을 복구하고 통신, 헬스케어, 인프라 등의 분야에서 서비스의 연속성을 보장하기 위해 매우 중요합니다. 환경 규제가 엄격해짐에 따라 제조업체는 자동화, 원격 모니터링 및 배출량 감소를 목표로 한 기능을 통합합니다. 또한 지속가능성에 대한 우려로 디젤에 태양광이나 축전지 등의 재생에너지를 조합한 하이브리드 시스템도 보급되고 있습니다. 이 시프트는 신뢰성과 환경 부하 감소를 모두 제공하여 환경에 민감한 지역에서 디젤 발전기의 실행 가능성을 높입니다. 아시아태평양에서는 특히 빈번한 정전에 시달리는 도시와 농촌 지역에서 디젤 발전기 시장이 성장하고 있습니다.

도로, 병원, 데이터센터와 같은 중요한 인프라에 대한 투자는 신뢰할 수 있는 백업 전원 솔루션에 대한 수요를 크게 촉진하고 있습니다. 정부와 민간 부문이 인프라의 확장과 현대화에 계속 힘을 쏟고 있는 가운데, 이러한 중요한 업무를 지원하는 지속적인 전력 공급의 필요성이 높아지고 있습니다. 도로와 교통망은 교통 관리 시스템, 신호 및 긴급 서비스를 위해 중단 없는 전력이 필요합니다. 병원에서는 특히 중증 환자 치료실이나 응급 치료실에서 정전시에도 구명 기기가 확실하게 작동하도록 백업 전원에 의존하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 368억 달러 |

| 예측 금액 | 736억 달러 |

| CAGR | 8.1% |

50kVA 이상 125kVA 미만의 디젤 발전기 시장은 2034년까지 연평균 복합 성장률(CAGR) 7.5%를 보일 것으로 예측됩니다. 이러한 시스템은 중소기업, 건강 관리 기관, 건설 현장에서 인기가 높아지고 있습니다. 특히 송전망이 끊어졌을 때 무정전으로 전력을 공급하여 중요한 서비스나 업무를 끊임없이 계속할 수 있는 점이 평가되고 있습니다.

대기 디젤 발전기 부문은 2024년에 49%의 점유율을 차지하며 2034년까지 연평균 복합 성장률(CAGR) 7.5%를 보일 것으로 예측됩니다. 이 부문의 성장은 건강 관리, 상업 인프라, 데이터센터와 같은 중요한 섹터에서 신뢰할 수 있는 백업 전원의 필요성이 증가하고 있기 때문입니다. 송전망의 신뢰성에 대한 우려가 강해지고 있는 중(특히 이상 기상이나 자연재해), 기업은 다운타임을 경감하고 업무 연속성을 확보하기 위해 백업 시스템을 우선하고 있습니다. 대기 디젤 발전기는 이러한 분야에서 우선적으로 선택되며 필요할 때 신속한 전력 복구를 제공합니다.

미국 디젤 발전기 시장은 2024년에 85.9%의 점유율을 차지하고 60억 달러를 창출합니다. 백업 전원 솔루션 수요는 송전망의 신뢰성, 날씨로 인한 빈번한 장애, 인프라의 노후화에 대한 우려 증가가 원동력이 되고 있습니다. 산업시설과 상업시설은 정전시의 사업 연속성을 확보하기 위해 디젤 발전기에 투자하고 있습니다. 또한 신재생에너지원의 통합이 진행되어 디젤 발전기가 신뢰성 높은 보조전원으로서 기능하는 하이브리드 전원 시스템에 대한 관심이 높아지고 있습니다.

세계 디젤 발전기 시장에서 최고의 기업은 Cummins, Caterpillar, Aggreko, Rolls-Royce, Generac Power Systems 등입니다. 시장에서의 존재감을 확고하게 하기 위해, 디젤 발전기 업계의 기업은 몇 가지 중요한 전략에 주력하고 있습니다. 대부분은 자동화와 원격 감시 등의 기술적 진보에 많은 투자를 하고 있으며, 이로써 사용자는 발전기를 보다 효율적으로 감시 및 제어할 수 있게 되어 운영 효율이 향상되고 있습니다. 각 회사는 또한 배출 감축 기능을 도입하고, 디젤과 태양광이나 축전지와 같은 재생에너지원을 조합한 하이브리드 시스템을 개발하여 지속가능성을 우선하고 있습니다. 이 기술 혁신은 이산화탄소 배출량을 줄일 뿐만 아니라 환경 의식이 높은 시장에서 제품 호소를 강화합니다. 또한 업계 각사는 중소기업부터 대규모 산업 사업에 이르기까지 보다 폭넓은 고객을 수용하기 위해 제품 포트폴리오를 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTLE 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석 : 지역별

- 북미

- 유럽

- 아시아태평양

- 중동

- 아프리카

- 라틴아메리카

- 전략적 대시보드

- 전략적 노력

- 경쟁 벤치마킹

- 혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 출력별, 2021-2034년

- 주요 동향

- 50kVA 이하

- 50-125kVA 이상

- 125-200kVA 이상

- 200-330kVA 이상

- 330-750kVA 이상

- 750kVA 이상

제6장 시장 규모와 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 주택

- 상업

- 산업

제7장 시장 규모와 예측 : 용도별, 2021-2034년

- 주요 동향

- 대기

- 피크 셰이빙

- 프라임 및 연속

제8장 시장 규모와 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 러시아

- 영국

- 독일

- 프랑스

- 스페인

- 오스트리아

- 이탈리아

- 아시아태평양

- 중국

- 호주

- 인도

- 일본

- 한국

- 인도네시아

- 말레이시아

- 태국

- 베트남

- 필리핀

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 튀르키예

- 이란

- 오만

- 아프리카

- 이집트

- 나이지리아

- 알제리

- 남아프리카

- 앙골라

- 케냐

- 모잠비크

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 칠레

제9장 기업 프로파일

- Aggreko

- Ashok Leyland

- Atlas Copco

- Captiva Energy Solutions Private Limited

- Caterpillar

- Cooper Corp.

- Cummins, Inc.

- Deere & Company

- FG Wilson

- Generac Power Systems, Inc.

- Greaves Cotton Limited

- HIMOINSA

- JC Bamford Excavators Ltd.

- Kirloskar

- Rehlko

- Mahindra POWEROL

- Mitsubishi Heavy Industries, Ltd.

- Powerica Limited

- Rapid Power Generation Ltd.

- Rolls-Royce plc

- Siemens

- Sterling and Wilson Pvt. Ltd.

- Sudhir Power Ltd.

- Supernova Genset

- Wartsila

- Yamaha Motor Co., Ltd.

The Global Diesel Gensets Market was valued at USD 36.8 billion in 2024 and is anticipated to grow at a CAGR of 8.1% to reach USD 73.6 billion by 2034. The expansion of this market is driven by an increasing demand for reliable backup power across residential, commercial, and industrial sectors, particularly in regions with unstable or frequently interrupted power grids. Diesel gensets are crucial in these areas, providing immediate power restoration and ensuring the continuity of services in sectors like telecom, healthcare, and infrastructure. As stricter environmental regulations come into play, manufacturers are incorporating automation, remote monitoring, and features aimed at reducing emissions. In response to sustainability concerns, hybrid systems that combine diesel with renewable energy sources, such as solar or battery storage, are gaining traction. This shift is making diesel gensets more viable in environmentally sensitive regions, offering both reliability and lower environmental impact. In the Asia-Pacific region, the diesel genset market is experiencing growth, particularly in urban and rural areas suffering from frequent power outages.

Investments in critical infrastructure like roads, hospitals, and data centers are significantly driving the demand for reliable backup power solutions. As governments and private sectors continue to focus on expanding and modernizing infrastructure, there is an increasing need for a continuous power supply to support these vital operations. Roads and transportation networks require uninterrupted power for traffic management systems, signaling, and emergency services. Hospitals depend on backup power to ensure life-saving equipment remains operational during power outages, especially in critical care units or emergency rooms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $36.8 Billion |

| Forecast Value | $73.6 Billion |

| CAGR | 8.1% |

The diesel genset market for units between >50 kVA and 125 kVA is expected to grow at a CAGR of 7.5% through 2034. These systems are becoming increasingly popular among small to medium-sized businesses, healthcare institutions, and construction sites. They are particularly valued for their ability to provide uninterrupted power during grid disruptions, ensuring that critical services and operations continue without delay.

The standby diesel genset segment held a 49% share in 2024 and is expected to grow at a 7.5% CAGR until 2034. This segment's rise is attributed to the growing need for reliable backup power in essential sectors such as healthcare, commercial infrastructure, and data centers. As concerns over grid reliability intensify-especially due to extreme weather events and natural disasters-businesses are prioritizing backup systems to mitigate downtime and ensure operational continuity. Standby diesel gensets are the preferred choice in these sectors, providing quick power restoration in times of need.

U.S. Diesel Gensets Market held 85.9% share in 2024, generating USD 6 billion. The demand for backup power solutions is driven by increasing concerns about grid reliability, frequent weather-related disruptions, and aging infrastructure. Industrial and commercial facilities are investing in diesel gensets to ensure business continuity during outages. Moreover, the growing integration of renewable energy sources has spurred interest in hybrid power systems, with diesel gensets serving as reliable supplemental power sources.

Top companies in the Global Diesel Gensets Market include Cummins, Caterpillar, Aggreko, Rolls-Royce, and Generac Power Systems. To solidify their market presence, companies in the diesel genset industry are focusing on several key strategies. Many are investing heavily in technological advancements, such as automation and remote monitoring, which allow users to monitor and control gensets more efficiently, improving operational efficiency. Companies are also prioritizing sustainability by incorporating emissions-reduction features and developing hybrid systems that combine diesel with renewable energy sources like solar and battery storage. This innovation not only reduces carbon footprints but also enhances product appeal in environmentally conscious markets. Additionally, players in the industry are expanding their product portfolios to cater to a broader range of customers, from small businesses to large-scale industrial operations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating, 2021 - 2034 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Standby

- 7.3 Peak shaving

- 7.4 Prime/continuous

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Russia

- 8.3.2 UK

- 8.3.3 Germany

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Indonesia

- 8.4.7 Malaysia

- 8.4.8 Thailand

- 8.4.9 Vietnam

- 8.4.10 Philippines

- 8.5 Middle East

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Turkey

- 8.5.5 Iran

- 8.5.6 Oman

- 8.6 Africa

- 8.6.1 Egypt

- 8.6.2 Nigeria

- 8.6.3 Algeria

- 8.6.4 South Africa

- 8.6.5 Angola

- 8.6.6 Kenya

- 8.6.7 Mozambique

- 8.7 Latin America

- 8.7.1 Brazil

- 8.7.2 Mexico

- 8.7.3 Argentina

- 8.7.4 Chile

Chapter 9 Company Profiles

- 9.1 Aggreko

- 9.2 Ashok Leyland

- 9.3 Atlas Copco

- 9.4 Captiva Energy Solutions Private Limited

- 9.5 Caterpillar

- 9.6 Cooper Corp.

- 9.7 Cummins, Inc.

- 9.8 Deere & Company

- 9.9 FG Wilson

- 9.10 Generac Power Systems, Inc.

- 9.11 Greaves Cotton Limited

- 9.12 HIMOINSA

- 9.13 J C Bamford Excavators Ltd.

- 9.14 Kirloskar

- 9.15 Rehlko

- 9.16 Mahindra POWEROL

- 9.17 Mitsubishi Heavy Industries, Ltd.

- 9.18 Powerica Limited

- 9.19 Rapid Power Generation Ltd.

- 9.20 Rolls-Royce plc

- 9.21 Siemens

- 9.22 Sterling and Wilson Pvt. Ltd.

- 9.23 Sudhir Power Ltd.

- 9.24 Supernova Genset

- 9.25 Wartsila

- 9.26 Yamaha Motor Co., Ltd.