|

시장보고서

상품코드

1871280

자동차 TIC 서비스 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Automotive TIC Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

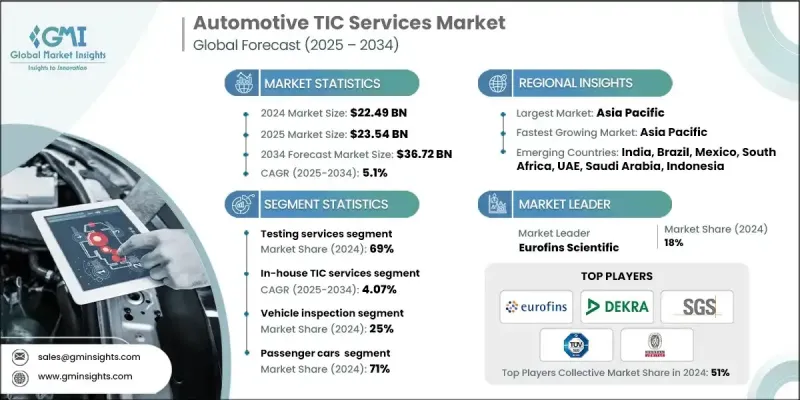

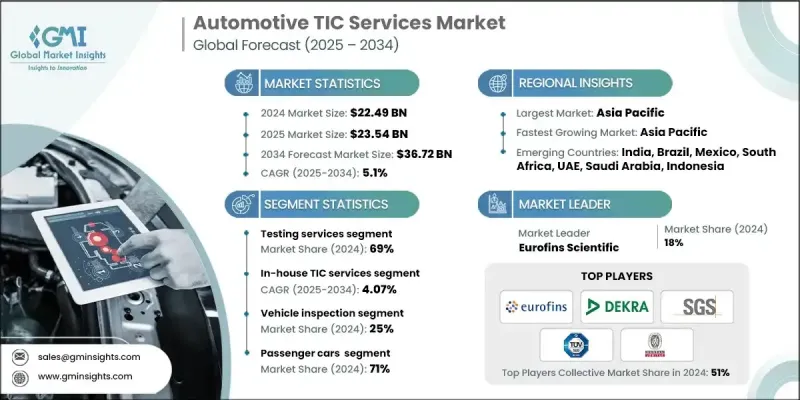

세계 자동차 TIC 서비스 시장은 2024년에 224억 9,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5.1%로 성장하고 367억 2,000만 달러에 이를 것으로 예측되고 있습니다.

자동차 TIC 분야는 진화하는 모빌리티 환경에서 기본적인 역할을 담당하게 되어 전기 파워트레인, 디지털 시스템, 커넥티드 기술을 탑재한 현대차량이 엄격한 안전성, 성능, 환경기준을 충족할 수 있도록 보장하고 있습니다. 이러한 서비스는 모든 부품과 프로세스가 국제 및 지역 규정을 준수하는지 확인하고 자동차 산업의 지속 가능하고 지능적인 이동성으로의 전환을 지원합니다. 전기자동차 및 하이브리드 자동차의 세계적인 보급에 따라 배터리 시스템, 배출 가스 제로 추진 기술, 커넥티드 소프트웨어 플랫폼에 대한 고도의 검증 수요가 높아지고 있는 가운데, TIC 서비스 수요는 계속 증가하고 있습니다. 또한 주요 경제권의 정부에 의한 엄격한 규제의 실시는 탄소 중립 목표와 안전 기준에의 적합을 보증하기 위한 독립적인 검증·인증의 필요성을 촉진하고 있습니다. 전기자동차 및 자율주행차를 위한 새로운 국제기준 도입도 시험 요건을 강화하여 세계 TIC 제공업체의 꾸준한 성장을 추진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 224억 9,000만 달러 |

| 예측 금액 | 367억 2,000만 달러 |

| CAGR | 5.1% |

시험 서비스 분야는 2024년에 69%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR)은 4.53%를 보일 것으로 예측됩니다. 이 분야의 이점은 차량의 성능과 안전성을 지속적으로 검증해야 하는 진화하는 규제 기준과 기술적 복잡성 때문입니다. 이 테스트는 차량이 소비자에게 도달하기 전에 내구성, 배출 가스, 안전 메커니즘 및 전반적인 기능성을 평가하기 위해 자동차 규정 준수의 기초입니다. 다양한 지역 시장에서의 정확성과 신뢰성에 대한 수요가 증가함에 따라 테스트 서비스 부문의 성장이 계속 추진되고 있습니다.

사내 부문은 2024년에 59%의 점유율을 차지하며, 2025년부터 2034년까지 4.07%의 연평균 복합 성장률(CAGR)로 성장할 것으로 추정됩니다. 기업은 품질 보증, 데이터 보안 및 사내 생산 시스템과의 통합을 완벽하게 관리하기 위해 사내 TIC(Test In Compliance) 운영을 선호합니다. 전용 테스트 인프라를 갖춘 주요 자동차 제조업체는 엄격한 규제 요구 사항을 충족하고 일관된 제조 기준을 보장하기 위해 내부 검증에 의존합니다. 이 접근법은 인증 프로세스의 가속화와 깊은 프로세스 최적화를 가능하게 하여 세계 시장에서 이 부문의 이점을 강화하고 있습니다.

아시아태평양 자동차 TIC 서비스 시장은 2024년 38%의 점유율을 차지했으며 85억 3,000만 달러 규모에 이르렀습니다. 이 지역의 주도적 지위는 방대한 자동차 생산 능력, 규제의 진화, 기술적 진보에 기인하고 있습니다. 아시아태평양 국가들은 보다 높은 안전 기준과 배출 가스 기준을 충족하기 위해 차량 시험 프레임워크를 확대하고 있습니다. 이 지역의 지속적인 산업화와 전기자동차 및 커넥티드 자동차 시험 시설에 대한 투자도 시장 성장을 가속하고 있습니다.

자동차 TIC 서비스 시장의 주요 기업으로는 TUV Rheinland, Eurofins Scientific, DEKRA, BSI, Burau Veritas, Intertek, SGS, TUV SUD, DNV GL 등이 있습니다. 주요 기업들은 전략적 확대, 디지털 전환, 파트너십 구축에 주력하여 시장에서의 지위 강화를 도모하고 있습니다. 많은 기업들이 효율성 향상, 테스트 시간 단축, 정확성 향상을 위해 자동화 및 AI 구동 테스트 솔루션에 대한 투자를 추진하고 있습니다. 자동차 제조업체와 정부 기관과의 협력을 통해 공급자는 새로운 규제 프레임 워크에 대응하고 전기자동차 및 자동 운전 차량을위한 고급 테스트 능력을 개발하고 있습니다. 또한 합병, 인수 및 합작 투자를 통한 지리적 확대로 새로운 시장 진출과 서비스 포트폴리오의 다양화도 진행하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝의 출처

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 엄격한 규제 준수

- 자동차산업의 세계화

- 차량 성능 테스트에 대한 수요 증가

- 품질보증에 대한 소비자 수요

- 자동차 시스템의 기술적 진보

- 업계의 잠재적 위험 및 과제

- 고급 TIC 기기의 고비용

- 복잡한 규제 환경

- 시장 기회

- 신흥 시장에서의 성장 기회

- 전기자동차 및 자율주행차의 개발

- 상용차용 TIC서비스 확충

- OEM에 의한 TIC서비스 아웃소싱

- 성장 촉진요인

- 성장 가능성 분석

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 코스트 내역 분석

- 기술 상황

- 현재의 기술 동향

- 신규기술

- 규제 상황

- 가격 동향

- 지역별

- 서비스별

- 지속가능성과 환경 컴플라이언스

- 탄소발자국 및 배출량 시험

- 수명 주기 평가(LCA) 서비스

- 순환형 경제와 재활용 가능성 테스트

- 환경 지속가능성 인증

- 환경 대응 차량의 적합 기준

- 비용 최적화 및 투자 이익률(ROI) 분석

- TIC서비스 투자 대 효과 분석

- 비용 편익 평가 프레임워크

- 총소유비용 모델

- 설비 가동률과 자원 최적화

- 실험실용량 분석

- 설비 가동률

- 노동력 생산성 지표

- 외부 위탁과 사내 실시의 의사 결정 분석

- 자사 개발과 외부 조달에 관한 의사 의사 결정의 틀

- 핵심 역량 평가

- 리스크·베네핏 분석

- 서비스 레벨 계약의 벤치마크

- SLA 퍼포먼스 기준

- 품질 지표 및 주요 성과 평가 지표(KPI)

- 페널티 및 인센티브 제도

- 자동차 테스트에서 사이버 보안

- 소프트웨어 보안 테스트 및 검증

- 취약성 평가 및 침투 테스트

- ISO/SAE 21434 준거와 규격

- 커넥티드카 및 자율주행차 사이버 보안

- 시장 출시 속도 및 애자일 테스트

- 가속 테스트 프로토콜

- 병행 테스트 조사 방법

- 신속한 인증 취득 프로세스

- 단축된 개발 사이클 전략

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신규 조달 개시

- 사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 서비스별, 2021년-2034년

- 주요 동향

- 시험 서비스

- 검사 서비스

- 인증서비스

- 기타

제6장 시장 추정 및 예측 : 제공원별, 2021년-2034년

- 주요 동향

- 자사 조달

- 외부 위탁

제7장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 차량 검사

- 배출가스 시험

- 부품시험

- 텔레매틱스

- ADAS

- 인증시험

- 연료, 유체 및 윤활유

- 전기 시스템 및 부품

- 기타

제8장 시장 추정 및 예측 : 차량별, 2021년-2034년

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 인도네시아

- 필리핀

- 태국

- 한국

- 싱가포르

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 기업

- BSI

- Bureau Veritas

- DEKRA

- DNV GL

- Eurofins Scientific

- Intertek

- Kiwa

- RINA

- SGS

- TUV Rheinland

- TUV SUD

- UL Solutions

- 지역 기업

- ALS

- Applus Services

- MISTRAS

- NSF International

- SOCOTEC

- The Smithers

- TUV NORD

- UTAC CERAM

- 신규 기업/디스럽터

- AVL

- Element Materials Technology

- ESCRYPT

- ETAS

- Keysight Technologies

The Global Automotive TIC Services Market was valued at USD 22.49 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 36.72 billion by 2034.

The automotive TIC sector has become a fundamental part of the evolving mobility landscape, ensuring that modern vehicles equipped with electric powertrains, digital systems, and connected technologies meet rigorous safety, performance, and environmental standards. These services validate that every component and process complies with international and regional regulations, supporting the automotive industry's transition toward sustainable and intelligent mobility. The demand for TIC services continues to rise as electric and hybrid vehicles expand globally, requiring more sophisticated validation for battery systems, emissions-free propulsion, and connected software platforms. In addition, the implementation of stringent regulations by governments across major economies is driving the need for independent verification and certification to ensure compliance with carbon neutrality goals and safety mandates. The introduction of new global standards for electric and autonomous vehicles has also intensified testing requirements, fueling steady growth for TIC providers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.49 Billion |

| Forecast Value | $36.72 Billion |

| CAGR | 5.1% |

The testing services segment held a 69% share in 2024 and is projected to grow at a 4.53% CAGR through 2034. The segment's dominance is attributed to evolving regulatory standards and technological complexity that demand continuous validation of vehicle performance and safety. Testing remains the cornerstone of automotive compliance as it assesses durability, emissions, safety mechanisms, and overall functionality before vehicles reach consumers. The rising need for precision and reliability across diverse regional markets continues to propel the testing services segment forward.

The in-house segment held a 59% share in 2024 and is estimated to register a 4.07% CAGR from 2025 to 2034. Companies favor in-house TIC operations to maintain full control over quality assurance, data security, and integration with internal production systems. Large automotive OEMs with dedicated testing infrastructure rely on in-house validation to meet strict regulatory requirements and ensure consistent manufacturing standards. This approach enables faster certification timelines and deeper process optimization, which has strengthened the dominance of this segment in the global market.

Asia Pacific Automotive TIC Services Market held a 38% share and generated USD 8.53 billion in 2024. The region's leadership is due to its vast automotive production capacity, regulatory evolution, and technological progress. Countries across APAC are expanding their vehicle testing frameworks to meet higher safety and emissions standards. The region's continuous industrialization and investment in electric and connected vehicle testing facilities are also propelling market growth.

Prominent players in the Automotive TIC Services Market include TUV Rheinland, Eurofins Scientific, DEKRA, BSI, Bureau Veritas, Intertek, SGS, TUV SUD, and DNV GL. Leading companies in the Automotive TIC Services Market are focusing on strategic expansion, digital transformation, and partnerships to strengthen their market position. Many firms are investing in automated and AI-driven testing solutions to improve efficiency, reduce testing times, and enhance accuracy. Collaborations with automotive OEMs and government bodies help providers align with emerging regulatory frameworks and develop advanced testing capabilities for electric and autonomous vehicles. Companies are also expanding geographically through mergers, acquisitions, and joint ventures to access new markets and diversify service portfolios.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Sourcing

- 2.2.4 Application

- 2.2.5 Vehicle

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future-outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent regulatory compliance

- 3.2.1.2 Globalization of the automotive industry

- 3.2.1.3 Rising demand for vehicle performance testing

- 3.2.1.4 Consumer demand for quality assurance

- 3.2.1.5 Technological advancements in automotive systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced TIC equipment

- 3.2.2.2 Complex regulatory environment

- 3.2.3 Market opportunities

- 3.2.3.1 Growth opportunities in emerging markets

- 3.2.3.2 Development of electric and autonomous vehicles

- 3.2.3.3 Expansion of commercial vehicle TIC services

- 3.2.3.4 Outsourcing of TIC services by OEMs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Patent analysis

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Cost breakdown analysis

- 3.8 Technology landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.2 Europe

- 3.9.3 Asia Pacific

- 3.9.4 Latin America

- 3.9.5 Middle East and Africa

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By service

- 3.11 Sustainability & environmental compliance

- 3.11.1 Carbon footprint and emissions testing

- 3.11.2 Lifecycle assessment (LCA) services

- 3.11.3 Circular economy and recyclability testing

- 3.11.4 Environmental sustainability certifications

- 3.11.5 Green vehicle compliance standards

- 3.12 Cost optimization & ROI analysis

- 3.12.1 TIC service investment return analysis

- 3.12.2 Cost-benefit assessment framework

- 3.12.3 Total cost of ownership models

- 3.13 Capacity utilization & resource optimization

- 3.13.1 Laboratory capacity analysis

- 3.13.2 Equipment utilization rates

- 3.13.3 Workforce productivity metrics

- 3.14 Outsourcing vs in-house decision analysis

- 3.14.1 Make vs buy decision framework

- 3.14.2 Core competency assessment

- 3.14.3 Risk-benefit analysis

- 3.15 Service level agreement benchmarking

- 3.15.1 SLA performance standards

- 3.15.2 Quality metrics & KPIs

- 3.15.3 Penalty & incentive structures

- 3.16 Cybersecurity in automotive testing

- 3.16.1 Software security testing and validation

- 3.16.2 Vulnerability assessment and penetration testing

- 3.16.3 ISO/SAE 21434 compliance and standards

- 3.16.4 Connected and autonomous vehicle cybersecurity

- 3.17 Speed to market & agile testing

- 3.17.1 Accelerated testing protocols

- 3.17.2 Parallel testing methodologies

- 3.17.3 Rapid certification pathways

- 3.17.4 Compressed development cycle strategies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New sourcing launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2021 - 2034 (USD Bn)

- 5.1 Key trends

- 5.2 Testing services

- 5.3 Inspection services

- 5.4 Certification services

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Sourcing, 2021 - 2034 (USD Bn)

- 6.1 Key trends

- 6.2 In-house

- 6.3 Outsourced

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Bn)

- 7.1 Key trends

- 7.2 Vehicle inspection

- 7.3 Emission testing

- 7.4 Component testing

- 7.5 Telematics

- 7.6 ADAS

- 7.7 Homologation testing

- 7.8 Fuels, fluids and lubricants

- 7.9 Electric systems and components

- 7.10 Others

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Bn)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicles (LCV)

- 8.3.2 Medium commercial vehicles (MCV)

- 8.3.3 Heavy commercial vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Indonesia

- 9.4.6 Philippines

- 9.4.7 Thailand

- 9.4.8 South Korea

- 9.4.9 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 BSI

- 10.1.2 Bureau Veritas

- 10.1.3 DEKRA

- 10.1.4 DNV GL

- 10.1.5 Eurofins Scientific

- 10.1.6 Intertek

- 10.1.7 Kiwa

- 10.1.8 RINA

- 10.1.9 SGS

- 10.1.10 TUV Rheinland

- 10.1.11 TUV SUD

- 10.1.12 UL Solutions

- 10.2 Regional Players

- 10.2.1 ALS

- 10.2.2 Applus+ Services

- 10.2.3 MISTRAS

- 10.2.4 NSF International

- 10.2.5 SOCOTEC

- 10.2.6 The Smithers

- 10.2.7 TUV NORD

- 10.2.8 UTAC CERAM

- 10.3 Emerging Players / Disruptors

- 10.3.1 AVL

- 10.3.2 Element Materials Technology

- 10.3.3 ESCRYPT

- 10.3.4 ETAS

- 10.3.5 Keysight Technologies