|

시장보고서

상품코드

1959570

면역관문 억제제 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Immune Checkpoint Inhibitors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

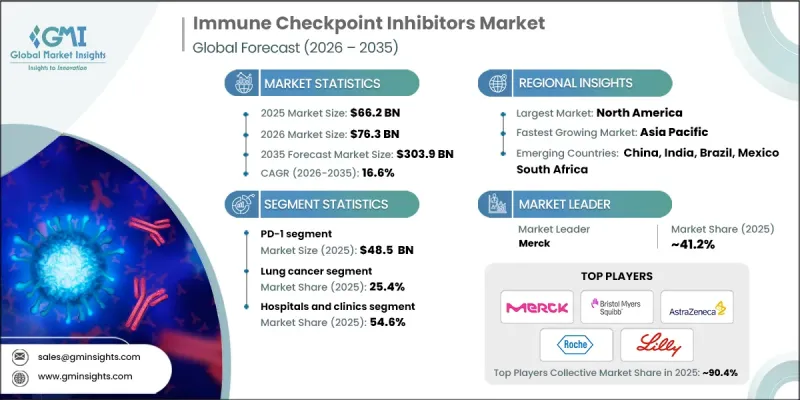

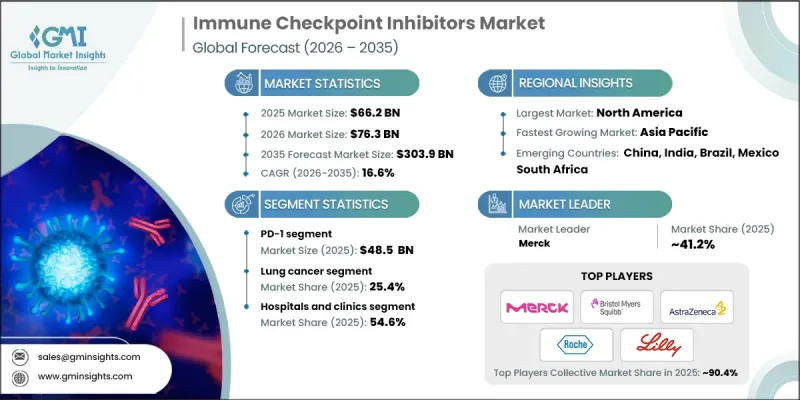

세계의 면역관문 억제제 시장은 2025년에 662억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 16.6%로 성장하여 3,039억 달러에 이를 것으로 예측됩니다.

이러한 시장 확대의 배경에는 다양한 암종에 대한 임상적 유효성이 입증되고, 종양학 분야에서 표준 치료로 채택이 확대되고 있다는 점이 있습니다. 전 세계적으로 암 발생률이 지속적으로 증가하고 있는 가운데, 면역관문 억제제와 같은 강력한 표적 치료제에 대한 수요가 증가하고 있습니다. 이들 치료제는 PD-1, PD-L1, CTLA-4와 같은 면역 체크포인트 단백질을 억제하여 체내 면역체계를 활성화시켜 종양세포와 싸우도록 작용합니다. 이 단백질은 암세포가 면역의 감지를 피하기 위해 사용하는 단백질입니다. 이 단백질을 억제하면 T세포 기능이 회복되어 면역계가 악성 세포를 효과적으로 표적화하여 제거할 수 있게 됩니다. 치료가 어려운 진행성 암 환자 증가로 면역치료 대상 환자군이 확대되는 한편, 보다 효과적이고 정밀하며 안전한 억제제 개발의 지속적인 혁신이 시장 성장을 견인하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 662억 달러 |

| 예측 금액 | 3,039억 달러 |

| CAGR | 16.6% |

PD-1 부문은 2025년 485억 달러에 달할 것으로 예상되며, 이는 암 면역치료에서 PD-1이 차지하는 중요한 역할을 반영합니다. PD-1 억제제는 암세포가 면역 인식을 피하기 위해 일반적으로 이용하는 PD-1 경로를 억제함으로써 면역계가 종양 세포를 공격하는 능력을 향상시킵니다. 이러한 치료법의 성공은 강력한 임상 결과, 승인된 적응증 증가, 종양학 진료에서의 광범위한 채택에 힘입어 PD-1 억제제가 현대 암 치료의 근간으로 자리매김하고 있습니다. 여러 암종에 대한 효능은 임상 종양학에서 그 지배적인 점유율을 강화하며 그 중요성을 확고히 하고 있습니다.

폐암 분야는 25.4%의 점유율을 차지하고 있으며, 2035년까지 연평균 16%의 성장률을 보일 것으로 예측됩니다. 이러한 우위는 면역관문 억제제가 폐암의 높은 유병률과 생존율 및 환자 예후 개선에 있어 입증된 임상적 이점에 기인합니다. 주요 치료제로서 면역요법의 채택이 확대되고 있으며, 폐암의 각 병기별 유효성을 확인하기 위한 임상시험이 지속되고 있어 시장에서의 입지가 더욱 강화되고 있습니다. 높은 질병 부담과 미충족 수요가 이러한 치료법에 대한 수요를 더욱 촉진하여 이 부문의 견조한 성장을 지속하고 있습니다.

북미 면역관문 억제제 시장은 2025년 48.3%의 점유율을 차지했습니다. 이러한 선도적 지위는 이러한 치료법의 연구개발 및 상업화에 적극적으로 참여하는 주요 제약회사들의 존재에 의해 뒷받침되고 있습니다. 이 지역은 유리한 규제 환경, 암 치료 이니셔티브에 대한 정부 및 비정부기구의 강력한 지원, 암 발병률 증가로 인한 수요 증가의 혜택을 누리고 있습니다. 북미는 높은 수준의 의료 인프라, 면역 치료 옵션에 대한 폭넓은 인식, 혁신적인 치료 솔루션에 대한 접근성이 결합되어 세계 시장에서의 입지를 강화하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별, 2022-2035

제6장 시장 추산 및 예측 : 용도별, 2022-2035

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제8장 시장 추산 및 예측 : 지역별, 2022-2035

제9장 기업 개요

LSH 26.03.18The Global Immune Checkpoint Inhibitors Market was valued at USD 66.2 billion in 2025 and is estimated to grow at a CAGR of 16.6% to reach USD 303.9 billion by 2035.

The market expansion is driven by the proven clinical effectiveness of these therapies across a broad spectrum of cancers and their increasing adoption as a standard of care in oncology. As cancer incidence continues to rise worldwide, the demand for potent and targeted treatments such as immune checkpoint inhibitors is intensifying. These therapies work by enhancing the body's immune system to combat tumor cells, specifically by blocking immune checkpoint proteins like PD-1, PD-L1, and CTLA-4, which are exploited by cancer cells to evade immune detection. By inhibiting these proteins, T-cell function is restored, enabling the immune system to effectively target and eliminate malignant cells. The rising prevalence of hard-to-treat and late-stage cancers is increasing the patient population for immunotherapy, while ongoing innovation in the development of more effective, precise, and safe inhibitors continues to propel market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $66.2 Billion |

| Forecast Value | $303.9 Billion |

| CAGR | 16.6% |

The PD-1 segment reached USD 48.5 billion in 2025, reflecting its critical role in cancer immunotherapy. PD-1 inhibitors enhance the immune system's ability to attack tumor cells by blocking the PD-1 pathway, which is commonly used by cancer cells to escape immune recognition. The success of these therapies is supported by strong clinical outcomes, a growing list of approved indications, and widespread adoption in oncology practices, positioning PD-1 inhibitors as a cornerstone in modern cancer treatment. Their effectiveness across multiple cancer types reinforces their dominant share and solidifies their importance in clinical oncology.

The lung cancer segment held 25.4% share and is expected to grow at a CAGR of 16% through 2035. This dominance is attributed to the high prevalence of lung cancer and the demonstrated clinical benefits of immune checkpoint inhibitors in improving survival rates and patient outcomes. The increasing adoption of immunotherapy as a primary treatment, combined with ongoing clinical trials exploring its efficacy in different stages of lung cancer, continues to strengthen market presence. The high disease burden and unmet medical needs further drive demand for these therapies, sustaining robust growth in this segment.

North America Immune Checkpoint Inhibitors Market held 48.3% share in 2025. This leadership is supported by the presence of major pharmaceutical companies actively engaged in research, development, and commercialization of these therapies. The region benefits from a favorable regulatory environment, strong governmental and non-governmental support for cancer treatment initiatives, and rising demand driven by increasing cancer prevalence. Advanced healthcare infrastructure, widespread awareness of immunotherapy options, and access to innovative treatment solutions collectively strengthen North America's dominant position in the global market.

Key players in the Global Immune Checkpoint Inhibitors Market include Merck, Bristol-Myers Squibb Company, AstraZeneca, BeiGene, GlaxoSmithKline, Eli Lilly and Company, Sanofi, Immutep Limited, Incyte Corporation, Shanghai Junshi Biosciences, Zydus Lifesciences, Regeneron Pharmaceuticals, F. Hoffmann-La Roche, and Sun Pharmaceuticals. Companies in the immune checkpoint inhibitors market are leveraging multiple strategies to expand their footprint and reinforce their market presence. They are investing heavily in research and development to create next-generation inhibitors with improved safety profiles, broader efficacy, and expanded indications across cancer types. Strategic partnerships with biotechnology firms, hospitals, and academic institutions accelerate clinical trials and innovation. Geographic expansion into emerging markets allows firms to tap into growing patient populations. Additionally, mergers and acquisitions, licensing agreements, and collaborations with regulatory agencies streamline market entry and product approvals.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer worldwide

- 3.2.1.2 Expanding approvals across multiple cancer indications

- 3.2.1.3 Growing shift toward immunotherapy as standard of care

- 3.2.1.4 Increasing investments and partnerships

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Growing risk of immune-related adverse events

- 3.2.2.2 High treatment costs

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of combination immunotherapy regimens

- 3.2.3.2 Development of next-generation immune checkpoint targets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Reimbursement scenario

- 3.6 Pipeline analysis

- 3.7 Pricing analysis

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 PD-1

- 5.3 PD-L1

- 5.4 CTLA-4

- 5.5 Other types

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Lung cancer

- 6.3 Breast cancer

- 6.4 Bladder cancer

- 6.5 Melanoma

- 6.6 Cervical cancer

- 6.7 Hodgkin lymphoma

- 6.8 Colorectal cancer

- 6.9 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Cancer centers

- 7.4 Academic and research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AstraZeneca

- 9.2 BeiGene

- 9.3 Bristol-Myers Squibb Company

- 9.4 Eli Lilly and Company

- 9.5 F. Hoffmann-La Roche

- 9.6 GlaxoSmithKline

- 9.7 Incyte Corporation

- 9.8 Immutep Limited

- 9.9 Merck

- 9.10 Regeneron Pharmaceuticals

- 9.11 Sanofi

- 9.12 Shanghai Junshi Biosciences

- 9.13 Sun Pharmaceuticals

- 9.14 Zydus Lifesciences