|

시장보고서

상품코드

1858995

혈압계 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Sphygmomanometer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

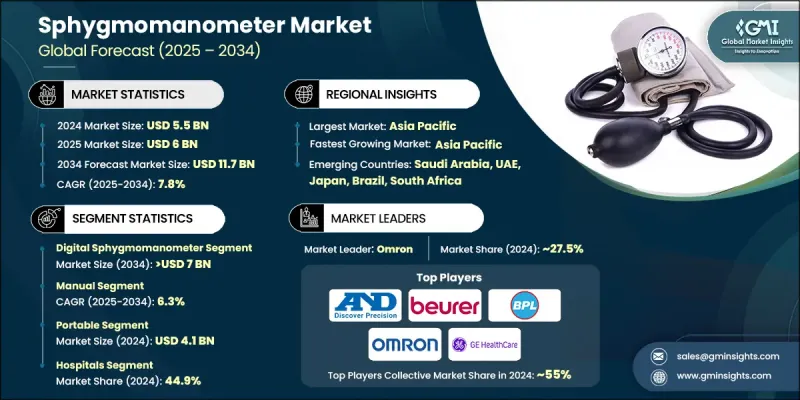

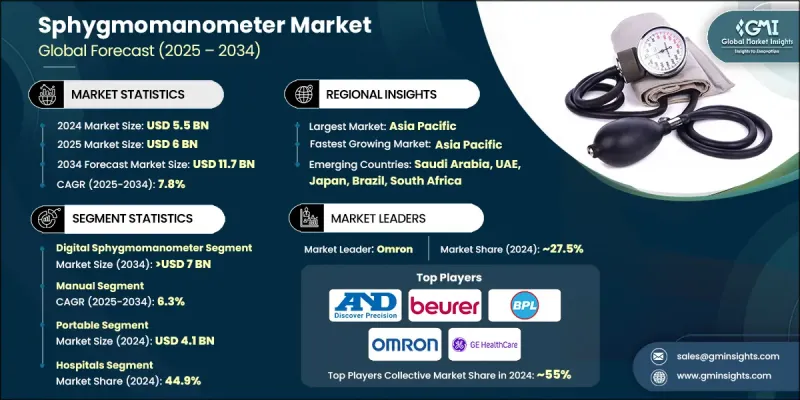

세계의 혈압계 시장은 2024년에는 55억 달러로 평가되었으며 CAGR 7.8%를 나타내 2034년에는 117억 달러에 이를 것으로 추정됩니다.

이 성장은 세계적인 고혈압 및 심혈관 질환의 이환율 증가, 노화, 건강 의식 증가, 예방 의료 및 조기 진단을 추진하는 정부의 강력한 이니셔티브를 기여합니다. 재택 헬스케어와 원격 모니터링 솔루션 수요가 급증하고 있는 것도 큰 요인입니다. 낮은 영양, 운동 부족 및 스트레스 수준의 상승을 특징으로 하는 라이프 스타일의 변화는 고혈압의 유병률을 증가시킵니다. 건강 상태를 파악하기 위해 신뢰할 수 있는 간단한 솔루션을 요구하는 사람이 늘어나기 때문에 사용하기 쉬운 혈압계 수요가 계속 증가하고 있습니다. 혈압계는 혈압을 측정하는 데 사용되는 의료기기이며 일반적으로 혈압 밴드, 압력계 및 수동 또는 자동 팽창 메커니즘으로 구성됩니다. 자체 모니터링과 조기 발견에 대한 관심이 높아짐에 따라 이러한 장비는 현대 건강 관리 동향의 중심에 자리 잡고 있으며 임상 애플리케이션과 개인 웰빙 추적을 모두 지원합니다. 시장의 현저한 변화는 디지털 기술로의 전환입니다. 자동 혈압계는 내장 메모리, 경과 추적, 무선 데이터 전송 등의 고급 기능으로 큰 지지를 얻고 있습니다. 이러한 디지털 도구는 건강 앱과 클라우드 기반 시스템과의 원활한 통합을 가능하게 하여 사용자의 건강 관리 및 의료 전문가와 측정치 간의 의사소통을 용이하게 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 55억 달러 |

| 예측 금액 | 117억 달러 |

| CAGR | 7.8% |

디지털 부문은 2024년에 56.7%의 점유율을 차지했습니다. 그 이유는 사용의 용이성, 정확한 판독, 개인 및 임상 환경에서의 급속한 보급에 있습니다. 이러한 장치는 오실로메트릭 측정법을 채택하여 수동 청진의 필요성을 제거함으로써 인위적인 실수를 최소화하고 보다 안정적인 판독을 가능하게 합니다. 또한 블루투스와 앱 호환성이 통합되어 원격 의료 및 가상 건강 관리 모델에 널리 채택되었습니다.

수동 혈압계 부문은 2034년까지 연평균 복합 성장률(CAGR) 6.3%를 나타낼 것으로 예측됩니다. 디지털 기기의 보급에도 불구하고 수동 모니터는 탁월한 정확성으로 의료 현장에서 높은 평가를 받고 있습니다. 특히 고위험 환자 집단이나 임상 연구 등 정확한 평가를 위해 청진이 선호되는 경우에는 임상 평가에서 신뢰받고 있습니다. 이러한 장비는 편의성보다 진단의 신뢰성을 선호하는 건강 관리 환경에서도 지원됩니다.

북미의 혈압계 시장은 2034년까지의 CAGR은 5.3%를 나타낼 것으로 예측되고 있으며, 이는 확립된 헬스케어 시스템, 심혈관 건강에 대한 높은 의식, 원격 환자 모니터링 기술을 채용하는 소비자 증가에 지지되고 있습니다. 이 지역은 또한 가정 모니터링 장비에 대한 액세스를 향상시키는 유리한 건강 관리 상환 정책의 혜택을 받고 있습니다. FDA와 같은 규제기관은 제품의 안전성과 성능을 보장하며, 이는 시장의 신뢰성을 지원하고 수요를 촉진하고 있습니다. 메디케어나 민간 플랜을 포함한 보험이 널리 보급되고 있는 것도 가정용 혈압 모니터의 성장을 더욱 뒷받침하고 있습니다.

세계의 혈압계 시장을 선도하는 주요 업계 기업으로는 GE Healthcare, beurer, OMRON, BPL, ADC, ACCOSON, BOSCH SOHN, PRESTIGE MEDICAL, SUNTECH, Riester, microlife, Little Doctor, Rossmax, Spengler, AND 등이 있습니다. 세계 혈압계 시장에서의 존재를 강화하기 위해 주요 기업들은 몇 가지 전략적 움직임에 주력하고 있습니다. 여기에는 지속적인 제품 혁신, 앱과의 연계, AI 기반 분석 등의 고급 디지털 기능 통합, 세계 유통망 확대 등이 포함됩니다. 많은 기업들은 전문 의료 서비스 제공업체와 홈 사용자 모두를 수용하고 정확성, 편안함 및 사용 편의성을 높이기 위해 R&D에 투자하고 있습니다. 원격 의료 플랫폼 및 건강 관리 기관과의 전략적 파트너십도 보급 확대에 중요한 역할을 하고 있습니다. 또한 각 회사는 여행용 컴팩트한 장비부터 진료소용 전문 사양 모니터까지 다양한 사용자의 요구에 맞게 제품 라인을 조정하여 여러 고객층에 걸쳐 강력한 발판을 확보하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 고혈압과 심혈관 질환의 유병률 상승

- 예방 헬스케어와 조기 진단을 추진하는 정부의 대처

- 기술적 진보

- 재택치료와 원격 환자 모니터링 수요 증가

- 업계의 잠재적 리스크 및 과제

- 엄격한 규제 당국의 승인과 컴플라이언스

- 시장 기회

- 신흥국에서의 헬스케어 인프라의 확대

- 디지털 채용 혈압계

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술적 상황

- 현재의 기술

- 신흥기술

- 향후 시장 동향

- 소비자 행동 분석

- 고혈압 증례 수 : 지역별(2021-2024년)

- 상환 시나리오

- 파이프라인 분석

- 투자 상황

- 가격 분석(2024년)

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카, 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발표

- 확장 계획

제5장 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 디지털 혈압계

- 팔 전자 혈압계

- 손목 전자 혈압계

- 아네로이드 혈압계

- 수은 혈압계

제6장 시장 추계·예측 : 작동 방식별(2021-2034년)

- 주요 동향

- 수동

- 자동

- 반자동

제7장 시장 추계·예측 : 구성별(2021-2034년)

- 주요 동향

- 휴대용

- 책상 설치형

- 바닥 설치형

- 벽걸이형

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 재택치료

- 외래 수술 센터(ASC)

- 기타 최종 용도

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- ACCOSON

- ADC

- AND

- beurer

- BOSCH SOHN

- BPL

- GE Healthcare

- Little Doctor

- microlife

- Omron

- PRESTIGE MEDICAL

- Riester

- rossmax

- Spengler

- SUNTECH

The Global Sphygmomanometer Market was valued at USD 5.5 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 11.7 billion by 2034.

This growth is fueled by the increasing global incidence of hypertension and cardiovascular conditions, the aging population, growing health awareness, and strong initiatives by governments promoting preventive care and early diagnosis. A major contributing factor is the surge in demand for home healthcare and remote monitoring solutions. Lifestyle shifts characterized by poor nutrition, physical inactivity, and elevated stress levels have intensified the prevalence of high blood pressure. As more individuals seek reliable and simple solutions to track their health, demand for user-friendly blood pressure monitors continues to rise. A sphygmomanometer is a medical device used to measure blood pressure and typically consists of a cuff, a pressure gauge, and an inflation mechanism, which may be manual or automated. The growing focus on self-monitoring and early detection has placed these devices at the center of modern healthcare trends, supporting both clinical applications and personal wellness tracking. A notable transformation in the market is the shift toward digital technology. Automated sphygmomanometers have gained significant traction due to advanced features such as internal memory, progress tracking, and wireless data transmission. These digital tools enable seamless integration with health apps and cloud-based systems, making it easier for users to manage their health and communicate readings with medical professionals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.5 Billion |

| Forecast Value | $11.7 Billion |

| CAGR | 7.8% |

The digital segment held a 56.7% share in 2024, owing to its user-friendliness, precise readings, and rapid uptake in personal and clinical environments. These devices use oscillometric measurement methods, which eliminate the need for manual auscultation, minimizing human error and allowing for more consistent readings. Additionally, the integration of Bluetooth and app compatibility has allowed for wider adoption in telemedicine and virtual healthcare models.

The manual sphygmomanometers segment is expected to grow at a CAGR of 6.3% through 2034. Despite the popularity of digital devices, manual monitors remain highly regarded in medical settings for their unmatched accuracy. They continue to be relied upon in clinical assessments, especially where auscultation is preferred for precise evaluation, such as in high-risk patient populations or clinical studies. These devices are also favored in healthcare environments that prioritize diagnostic reliability over convenience.

North America Sphygmomanometer Market is projected to grow at a CAGR of 5.3% through 2034, supported by a well-established healthcare system, high awareness of cardiovascular health, and growing consumer adoption of remote patient monitoring technologies. The region also benefits from favorable healthcare reimbursement policies that improve access to home monitoring devices. Regulatory agencies such as the FDA ensure product safety and performance, which supports market confidence and drives demand. Widespread insurance coverage, including Medicare and private plans, further supports the growth of home-use blood pressure monitors.

Key industry players leading the Global Sphygmomanometer Market include GE Healthcare, beurer, OMRON, BPL, ADC, ACCOSON, BOSCH + SOHN, PRESTIGE MEDICAL, SUNTECH, Riester, microlife, Little Doctor, Rossmax, Spengler, and AND. To strengthen their presence in the Global Sphygmomanometer Market, leading companies are focusing on several strategic moves. These include continuous product innovation, integrating advanced digital features like app connectivity and AI-based analytics, and expanding their global distribution networks. Many firms are investing in R&D to enhance accuracy, comfort, and usability, catering to both professional healthcare providers and home users. Strategic partnerships with telehealth platforms and healthcare institutions also play a key role in increasing adoption. Additionally, companies are tailoring product lines for various user needs from compact devices for travel to professional-grade monitors for clinics ensuring a strong foothold across multiple customer segments.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Operation trends

- 2.2.4 Configuration trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of hypertension and cardiovascular diseases

- 3.2.1.2 Government initiatives promoting preventive healthcare and early diagnosis

- 3.2.1.3 Technological advancements

- 3.2.1.4 Increasing demand for home healthcare and remote patient monitoring.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory approvals and compliance

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding healthcare infrastructure in emerging economies

- 3.2.3.2 Adoption of digital sphygmomanometer

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Consumer behavior analysis

- 3.8 Number of cases of hypertension, by region, 2021 - 2024

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.8.4 Latin America

- 3.8.5 MEA

- 3.9 Reimbursement scenario

- 3.10 Pipeline analysis

- 3.11 Investment landscape

- 3.12 Pricing analysis, 2024

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia Pacific

- 4.3.4 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Digital sphygmomanometer

- 5.2.1 Arm electronic sphygmomanometer

- 5.2.2 Wrist electronic sphygmomanometer

- 5.3 Aneroid sphygmomanometer

- 5.4 Mercury sphygmomanometer

Chapter 6 Market Estimates and Forecast, By Operation, 2021 - 2034 ($ Mn, Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Automatic

- 6.4 Semi-automatic

Chapter 7 Market Estimates and Forecast, By Configuration, 2021 - 2034 ($ Mn, Units)

- 7.1 Key trends

- 7.2 Portable

- 7.3 Desk mounted

- 7.4 Floor standing

- 7.5 Wall mounted

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Homecare

- 8.4 Ambulatory surgical centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ACCOSON

- 10.2 ADC

- 10.3 AND

- 10.4 beurer

- 10.5 BOSCH + SOHN

- 10.6 BPL

- 10.7 GE Healthcare

- 10.8 Little Doctor

- 10.9 microlife

- 10.10 Omron

- 10.11 PRESTIGE MEDICAL

- 10.12 Riester

- 10.13 rossmax

- 10.14 Spengler

- 10.15 SUNTECH