|

시장보고서

상품코드

1892896

외래 종양학 주입 치료 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)Outpatient Oncology Infusion Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

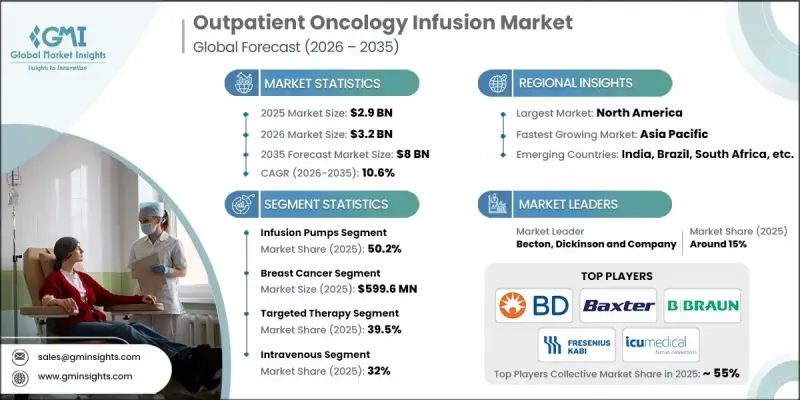

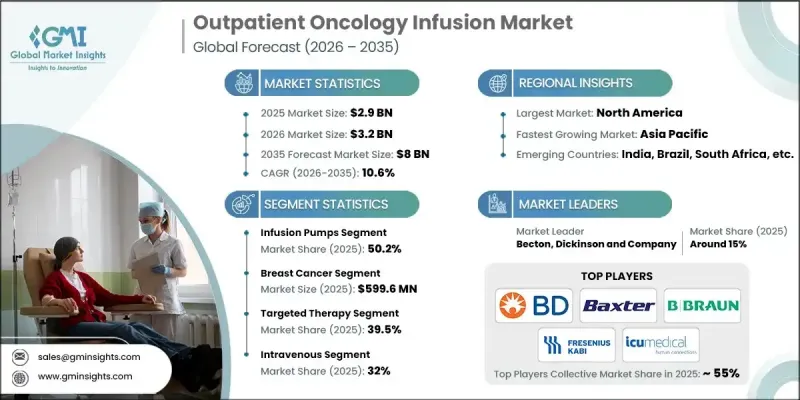

세계의 외래 종양학 주입 치료 시장은 2025년에 29억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 10.6%를 나타내 80억 달러에 달할 것으로 예측되고 있습니다.

시장 확대의 배경에는 비용 효과적인 외래 치료에 대한 수요 증가, 암 이환율의 상승, 암 계발을 추진하는 정부 시책, 점적 기술의 발전이 들 수 있습니다. 또한 표적요법과 면역요법 도입 확대, 가치 기반 의료로의 이행, 원격의료를 활용한 점적 서비스가 수요를 견인하고 있습니다. 생활습관요인, 비만, 환경적 영향이 암 증례 수 증가에 기여하고 있어 효과적이고 접근하기 쉬운 치료법의 필요성이 높아지고 있습니다. 외래 점적 센터는 입원에 비해 전체 비용을 절감하면서 환자에게 더 편리하고 효율적인 치료 모델을 제공합니다. 또한 자동투여, 에러경보, 전자건강기록(EHR)과의 호환성을 갖춘 첨단 스마트 점적펌프의 통합으로 안전성과 운용효율이 모두 향상되어 세계 외래 종양학 주입 치료 서비스의 매력이 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 가치 | 29억 달러 |

| 예측 금액 | 80억 달러 |

| CAGR | 10.6% |

주입 펌프 부문은 2025년에 50.2%의 점유율을 차지했습니다. 이 장비는 휴대용 설계와 스마트 시스템 통합을 특징으로 하며 환자의 편안함을 높이고 유연한 투여를 가능하게 하며 정확한 용량을 지원합니다. 펌프의 기술적 진보는 외래 주입 서비스의 성장에 중심적인 역할을 합니다.

2025년 시점에서 표적 치료 부문은 39.5%의 점유율을 차지했습니다. 이 요법은 암과 관련된 특정 분자 경로에 작용하며 통제 된 주입에 의해 투여됩니다. 그 투여에는 외래 주입 센터가 바람직하며, 정확한 투여량과 환자의 반응을 감시하기 위한 고급 주입 장치와 숙련된 인재의 필요성을 촉진하고 있습니다.

북미의 외래 종양학 주입 치료 시장은 2025년 43.1%의 점유율을 차지하며 대폭적인 성장이 전망되었습니다. 이 지역은 선진적인 의료 인프라, 다수의 암 환자, 혁신적인 점적 기술의 적극적인 도입이라는 이점을 가지고 있습니다. 종합적인 보험 적용 범위와 가치에 근거한 의료로의 이행에 의해 환자는 입원 환경에 비해 보다 저렴한 비용으로 외래암 치료를 받을 수 있게 되었습니다. 외래진료시설에서 스마트 주입펌프와 통합형 전자건강기록(EHR) 시스템의 도입은 환자 안전성과 업무 워크플로우를 향상시켜 시장의 추가 성장을 가속하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계적으로 증가하는 암의 유병률

- 비용 효율적인 외래 의료에 대한 선호도 증가

- 주입 펌프의 기술적 진보

- 암 계발을 향한 정부 주도의 대처의 급증

- 업계의 잠재적 위험 및 과제

- 암 치료의 고비용

- 기회

- 전자건강기록(EHR)과의 상호운용성을 갖춘 스마트 주입펌프 도입

- 치료 비용 절감을 위한 바이오시밀러의 개발

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 기술 및 혁신 현황

- 현재 기술 동향

- 신흥 기술

- 밸류체인 분석

- 상환 시나리오

- 정책 환경

- 역학 시나리오

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

- 향후 시장 동향

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병

- 파트너십 및 협력

- 신제품 출시

- 확대 계획

제5장 시장 추계·예측 : 제품별(2021-2034년)

- 주입 펌프

- 정맥 주사 세트

- 정맥 카테터

- 바늘 없는 커넥터

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 폐암

- 간암

- 유방암

- 전립선암

- 기타 암

제7장 시장 추계·예측 : 치료법별(2021-2034년)

- 항암화학요법

- 표적요법

- 면역요법

- 호르몬요법

제8장 시장 추계·예측 : 투여 경로별(2021-2034년)

- 근육 내(IM)

- 정맥 내(IV)

- 피하

- 기타 방식

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

제10장 기업 프로파일

- B. Braun

- Baxter

- Becton, Dickinson and Company

- Fresenius Kabi

- ICU Medical

- IRADIMED

- Medtronic

- Micrel

- MOOG

- NIPRO

- Penlon

- Teleflex

- Terumo

The Global Outpatient Oncology Infusion Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 10.6% to reach USD 8 billion by 2035.

The market expansion is fueled by increasing preference for cost-efficient outpatient care, rising cancer prevalence, government initiatives promoting cancer awareness, and advancements in infusion technologies. Rising adoption of targeted therapies and immunotherapies, the shift toward value-based care, and telehealth-assisted infusion services are further driving demand. Lifestyle factors, obesity, and environmental influences contribute to the growing number of cancer cases, increasing the need for effective and accessible treatments. Outpatient infusion centers provide patients with a more convenient and efficient treatment model while reducing overall costs compared to hospitalization. Additionally, the integration of advanced smart infusion pumps with automated dosing, error alerts, and electronic health record (EHR) compatibility has enhanced both safety and operational efficiency, strengthening the appeal of outpatient oncology infusion services worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $8 Billion |

| CAGR | 10.6% |

The infusion pumps segment held a 50.2% share in 2025. These devices, featuring portable designs and smart system integration, enhance patient comfort, allow flexible administration, and support precise dosing. Technological improvements in pumps are central to the growth of outpatient infusion services.

The targeted therapy segment accounted for a 39.5% share in 2025. These therapies act on specific molecular pathways linked to cancer and delivered through controlled infusion. Outpatient infusion centers are preferred for their administration, driving the need for advanced infusion devices and skilled personnel to monitor accurate dosing and patient response.

North America Outpatient Oncology Infusion Market held 43.1% share in 2025 and is expected to grow significantly. The region benefits from advanced healthcare infrastructure, a high number of cancer patients, and strong adoption of innovative infusion technologies. Comprehensive insurance coverage and the shift toward value-based care allow patients to access outpatient cancer treatments more affordably than in hospital settings. Adoption of smart infusion pumps and integrated EHR systems in outpatient centers enhances patient safety and operational workflow, further boosting market growth.

Key companies operating in the Global Outpatient Oncology Infusion Market include B. Braun, Baxter, Fresenius Kabi, Medtronic, MOOG, IRADIMED, Micrel, NIPRO, Teleflex, Terumo, ICU Medical, Penlon, and Becton, Dickinson and Company. Companies in the Global Outpatient Oncology Infusion Market focus on strategies such as continuous product innovation in smart infusion pumps, integration of digital health platforms, and development of user-friendly, portable devices to improve patient outcomes. Expansion into new geographic regions and partnerships with healthcare providers enhance market reach. Firms also invest in training programs for clinical staff to ensure accurate administration of therapies. Additionally, collaborations with telehealth services, EHR integration, and value-based care initiatives strengthen operational efficiency, patient safety, and long-term adoption, helping companies solidify their market foothold and maintain leadership in a competitive environment.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 Therapy trends

- 2.2.5 Mode trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer across the globe

- 3.2.1.2 Increasing preference for cost-effective outpatient care

- 3.2.1.3 Technological advancements in infusion pumps

- 3.2.1.4 Surging government initiatives for cancer awareness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of cancer therapies

- 3.2.3 Opportunities

- 3.2.3.1 Adoption of smart infusion pumps with EHR interoperability

- 3.2.3.2 Development of biosimilars to reduce treatment costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 LAMEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Value chain analysis

- 3.7 Reimbursement scenario

- 3.8 Policy landscape

- 3.9 Epidemiology scenario

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Infusion pumps

- 5.3 Intravenous sets

- 5.4 IV cannulas

- 5.5 Needleless connectors

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Lung cancer

- 6.3 Liver cancer

- 6.4 Breast cancer

- 6.5 Prostate cancer

- 6.6 Other cancers

Chapter 7 Market Estimates and Forecast, By Therapy, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Chemotherapy

- 7.3 Targeted therapy

- 7.4 Immunotherapy

- 7.5 Hormonal therapy

Chapter 8 Market Estimates and Forecast, By Mode, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Intramuscular (IM)

- 8.3 Intravenous (IV)

- 8.4 Subcutaneous

- 8.5 Other modes

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Nigeria

- 9.6.5 Egypt

Chapter 10 Company Profiles

- 10.1 B. Braun

- 10.2 Baxter

- 10.3 Becton, Dickinson and Company

- 10.4 Fresenius Kabi

- 10.5 ICU Medical

- 10.6 IRADIMED

- 10.7 Medtronic

- 10.8 Micrel

- 10.9 MOOG

- 10.10 NIPRO

- 10.11 Penlon

- 10.12 Teleflex

- 10.13 Terumo