|

시장보고서

상품코드

1892819

전립선암 진단 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Prostate Cancer Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

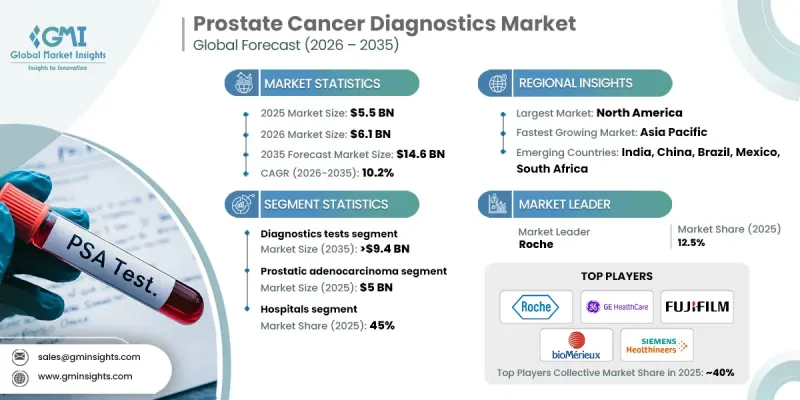

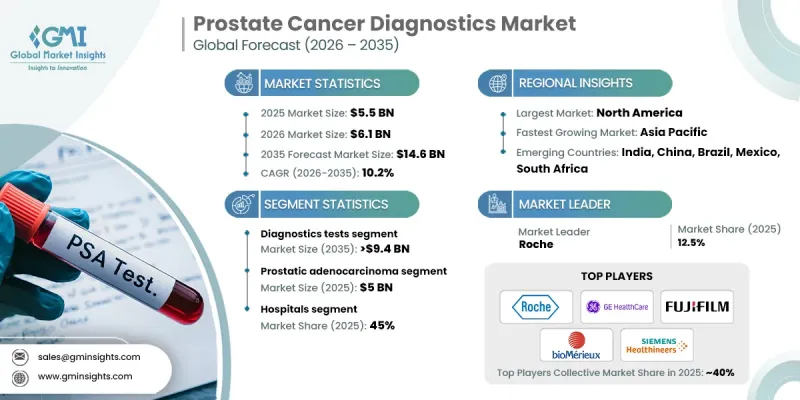

세계의 전립선암 진단 시장은 2025년에 55억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 10.2%로 성장하여 146억 달러에 이를 것으로 예측됩니다.

이러한 성장은 진단 기술의 지속적인 발전, 전 세계 전립선암 발병률 증가, 인식 개선 활동 확대, 검진 프로그램 확대, 남성 인구의 급속한 고령화 등에 의해 주도되고 있습니다. 전립선암 진단은 질병의 발견, 진행 정도 평가, 치료 방침을 결정하는 데 사용되는 종합적인 임상 검사 및 의료 절차를 말합니다. 이러한 진단에는 혈액 검사, 첨단 영상 진단 기술, 조직 분석법 등 정확한 질환의 확인과 경과 관찰을 지원하는 방법들이 포함됩니다. 차세대 시퀀싱, 액체 기반 진단 접근법, 다변량 영상 진단, AI 지원 분석 도구 등 최근 기술 발전으로 진단 정확도가 크게 향상되는 동시에 불필요한 개입이 감소하고 있습니다. 업계는 보다 정확하고 덜 침습적인 진단 경로로의 전환과 분자 및 유전체 프로파일링에 대한 의존도가 높아짐에 따라 의료 현장 전반에서 조기 발견율과 임상적 의사결정을 개선하는 데 도움이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 개시 연도 시장 규모 | 55억 달러 |

| 예측 금액 | 146억 달러 |

| CAGR | 10.2% |

진단 검사 부문은 2025년 63.6%의 점유율을 차지할 것으로 예측됩니다. 이러한 선도적 지위는 선별검사 및 바이오마커 검사의 이용 증가, 조기 발견에 대한 관심 증가, 비침습적 진단법의 보급을 반영합니다. 질병 유병률 증가와 환자 인식의 향상으로 인해 신뢰할 수 있고 정확한 검사 솔루션에 대한 수요는 꾸준히 증가하고 있습니다.

병원 부문은 2025년에 45%의 점유율을 차지할 것으로 예상되며, 2025년부터 2035년 사이에 64억 달러에 달할 것으로 전망됩니다. 병원은 초기 환자 평가, 고급 영상진단, 확진 검사에 있어서의 역할로 인해 전립선암 진단의 중심이 되고 있습니다. 통합 진단 능력은 단일 의료 환경 내에서 종합적인 질병 평가 및 병기 분류를 지원합니다.

북미 전립선암 진단 시장은 2025년 40.4%의 점유율을 차지했습니다. 높은 질병 발생률, 확립된 검진 관행, 선진화된 의료 인프라가 이 지역의 견조한 성과를 뒷받침하고 있습니다. 잘 갖추어진 진단 시설과 조기 발견 이니셔티브가 지역 전체에서 첨단 진단 기술 채택을 지속적으로 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 기술 동향

- 현재 기술 동향

- 신기술

- 상환 시나리오

- 향후 시장 동향

- 밸류체인 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추산 및 예측 : 테스트 유형별, 2022-2035

- 주요 동향

- 진단 검사

- PSA

- 전립선 생검

- 분자 및 유전체 검사

- 기타 진단 검사

- 영상 검사

- 경직장 초음파 검사(TRUS)

- MRI

- CT 스캔

- 기타 영상 검사

제6장 시장 추산 및 예측 : 암 유형별, 2022-2035

- 주요 동향

- 전립선선암

- 소세포암

- 기타 암종

제7장 시장 추산 및 예측 : 최종 용도별, 2022-2035

- 주요 동향

- 병원

- 진단실험실

- 암 연구기관

- 기타 용도

제8장 시장 추산 및 예측 : 지역별, 2022-2035

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 개요

- Abbott

- Beckman Coulter

- Becton, Dickinson and Company

- bioMerieux

- FUJIFILM

- GE HealthCare

- Glycanostics

- HEALGEN

- KOELIS

- Metamark Genetics

- Myriad Genetics

- OPKO Health

- PHILIPS

- Proteomedix

- Roche

- SIEMENS Healthineers

- Veracyte

The Global Prostate Cancer Diagnostics Market was valued at USD 5.5 billion in 2025 and is estimated to grow at a CAGR of 10.2% to reach USD 14.6 billion by 2035.

This growth is driven by continuous progress in diagnostic technologies, the increasing global burden of prostate cancer, wider awareness initiatives, and expanding screening programs, along with a rapidly aging male population. Prostate cancer diagnostics refers to a comprehensive range of clinical tests and medical procedures used to detect the disease, assess its progression, and guide treatment decisions. These diagnostics include blood-based assessments, advanced imaging techniques, and tissue analysis methods that support accurate disease identification and monitoring. Recent technological advancements, such as next-generation sequencing, liquid-based diagnostic approaches, multiparametric imaging, and AI-supported analysis tools, have significantly enhanced diagnostic precision while reducing unnecessary interventions. The industry continues to benefit from a shift toward more accurate, less invasive diagnostic pathways and greater reliance on molecular and genomic profiling, which together are improving early detection rates and clinical decision-making across healthcare settings.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.5 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 10.2% |

The diagnostic tests segment held a 63.6% share in 2025. This leadership position reflects rising utilization of screening and biomarker-based tests, increased preference for early-stage detection, and broader acceptance of non-invasive diagnostic methods. Growing disease prevalence and improved patient awareness continue to drive consistent demand for reliable and accurate testing solutions.

The hospitals segment held a 45% share in 2025 and is expected to reach USD 6.4 billion during 2025-2035. Hospitals remain central to prostate cancer diagnosis due to their role in initial patient evaluation, advanced imaging, and confirmatory procedures. Integrated diagnostic capabilities support comprehensive disease assessment and staging within a single care setting.

North America Prostate Cancer Diagnostics Market held a 40.4% share in 2025. Strong regional performance is supported by high disease incidence, established screening practices, and advanced healthcare infrastructure. The presence of well-equipped diagnostic facilities and early detection initiatives continues to drive the adoption of advanced diagnostic technologies across the region.

Key companies operating in the Global Prostate Cancer Diagnostics Market include Roche, Abbott, Siemens Healthineers, GE HealthCare, PHILIPS, Myriad Genetics, Becton, Dickinson and Company, Beckman Coulter, bioMerieux, Veracyte, FUJIFILM, OPKO Health, Proteomedix, Glycanostics, Metamark Genetics, KOELIS, and HEALGEN. Companies in the Global Prostate Cancer Diagnostics Market implement focused strategies to strengthen their competitive positioning. Continuous investment in research and development supports the launch of more accurate and clinically validated diagnostic tools. Firms emphasize integration of molecular diagnostics, advanced imaging analytics, and AI-driven interpretation to enhance diagnostic confidence. Strategic collaborations with healthcare providers and research institutions accelerate technology adoption and clinical validation. Expansion into emerging markets supports long-term growth, while regulatory alignment ensures timely product approvals.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Test type trends

- 2.2.3 Cancer type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of prostate cancer

- 3.2.1.2 Advancements in imaging and biomarker-based diagnostics

- 3.2.1.3 Surging awareness and screening initiatives

- 3.2.1.4 Growing demand for minimally invasive diagnostic procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced diagnostic modalities

- 3.2.2.2 Limited accessibility in low- and middle-income regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of AI-powered diagnostic tools

- 3.2.3.2 Growing adoption of personalized medicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Value chain analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Test Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostics tests

- 5.2.1 PSA

- 5.2.2 Prostate biopsy

- 5.2.3 Molecular/ genomic test

- 5.2.4 Other diagnostics tests

- 5.3 Imaging tests

- 5.3.1 Transrectal Ultrasound (TRUS)

- 5.3.2 MRI

- 5.3.3 CT Scan

- 5.3.4 Other imaging tests

Chapter 6 Market Estimates and Forecast, By Cancer Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Prostatic adenocarcinoma

- 6.3 Small cell carcinoma

- 6.4 Other cancer types

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Diagnostic laboratories

- 7.4 Cancer research institutes

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 Beckman Coulter

- 9.3 Becton, Dickinson and Company

- 9.4 bioMerieux

- 9.5 FUJIFILM

- 9.6 GE HealthCare

- 9.7 Glycanostics

- 9.8 HEALGEN

- 9.9 KOELIS

- 9.10 Metamark Genetics

- 9.11 Myriad Genetics

- 9.12 OPKO Health

- 9.13 PHILIPS

- 9.14 Proteomedix

- 9.15 Roche

- 9.16 SIEMENS Healthineers

- 9.17 Veracyte