|

시장보고서

상품코드

1664869

자동차 스타터 모터 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Automotive Starter Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

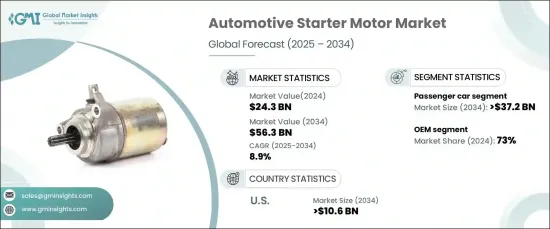

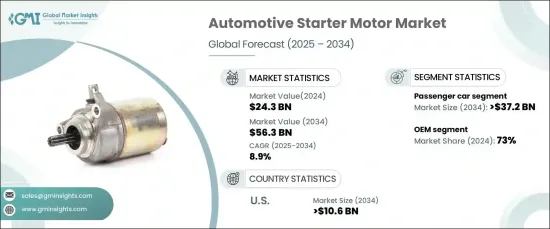

세계의 자동차 스타터 모터 시장은 2024년에 243억 달러로 평가되었고 2025년부터 2034년까지의 CAGR은 8.9%가 될 것으로 예측되어 현저한 성장이 전망되고 있습니다.

이 급성장의 배경은 기어 감속 메커니즘과 경량 설계와 같은 스타터 모터 기술의 최첨단 진보가 있습니다. 이러한 혁신은 효율성을 높일 뿐만 아니라 에너지 소비를 줄이고 자동차 성능을 향상시킵니다.

시장은 승용차와 상용차로 구분되며, 2024년 시장 점유율은 승용차가 67%로 압도적입니다. 2034년까지 이 부문은 372억 달러의 엄청난 이익을 창출할 것으로 예상됩니다. 이 성장을 뒷받침하는 주요 요인으로는 개인 이동성에 대한 수요가 증가하고 급속한 도시화, 특히 신흥 시장에서 가처분 소득이 증가하는 등이 있습니다. 또한, 연료 효율을 높이고 엄격한 배기 가스 기준을 충족하도록 설계된 스타트 스톱 시스템의 발전은 주로 승용차에 통합되어 있습니다. 이러한 지속적인 수요는 현대 자동차 솔루션에서 고도로 내구성 있는 스타터 모터가 매우 중요한 역할을 한다는 것을 뒷받침합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 243억 달러 |

| 예측 금액 | 563억 달러 |

| CAGR | 8.9% |

시장은 또한 상대방 상표 제품 제조업체(OEM)와 애프터마켓으로 나뉘어 2024년 시장 점유율은 OEM이 73%를 차지했습니다. 자동차 생산에 직접 참여하는 OEM은 원활한 통합, 우수한 품질 및 신뢰성 향상을 보장합니다. 자동차 제조업체는 스타터 모터를 대량으로 조달하고 최적화된 공급망을 활용하여 비용 효율성을 높입니다. 또한, 엄격한 성능과 규제 벤치마크를 충족시킬 필요성으로 인해 첨단 스타터 모터 솔루션공급자로서 OEM의 이점은 더욱 강력해졌습니다.

미국의 자동차 스타터 모터 시장은 2024년에 85%의 점유율을 차지했으며, 2034년까지는 106억 달러에 이를 것으로 예측됩니다. 이 나라의 장점은 자동차 제조 에코시스템이 확립하고 있으며 스타트 스톱 시스템과 같은 첨단 기술을 탑재한 자동차 수요가 높기 때문입니다. 연비 효율을 촉진하는 규제 조치에 의해 에너지 효율이 높은 스타터 모터의 채용이 가속되고 있습니다. 또한 주요 자동차 및 부품 제조업체가 존재하고 견고한 공급망 네트워크가 구축됨으로써 미국 시장의 리더십을 강화하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도의 산출

- 시장추계의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 소스

- 데이터 마이닝 소스

- 시장 정의

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 기술 제공업체

- 부품 공급자

- 제조업체

- OEM 제조업체

- 공급자의 상황

- 이익률 분석

- 기술 혁신의 상황

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 자동차 생산·판매 증가

- 스타터 모터 기술의 진보

- 전기차와 하이브리드차의 성장

- 연비와 배기가스 규제에 대한 관심 증가

- 업계의 잠재적 리스크·과제

- 높은 도입 비용

- 엄격한 규제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계·예측 : 스타터 모터별(2021-2034년), 10억 달러

- 주요 동향

- 전동 스타터 모터

- 공압 스타터 모터

- 유압 스타터 모터

- 기타

제6장 시장 추계·예측 : 차량별(2021-2034년), 10억 달러

- 주요 동향

- 승용차

- 상용차

제7장 시장 추계·예측 : 정격 출력별(2021-2034년), 10억 달러

- 주요 동향

- 1.5kW 미만

- 1.5-2.5kW

- 2.5kW 이상

제8장 시장 추계·예측 : 판매 채널별(2021-2034년), 10억 달러

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- BorgWarner Inc.

- Bosch

- Delco Remy

- DENSO

- Dongfeng Motor Parts and Components Group Co., Ltd.

- GDST Auto Parts

- Hella KGaA Hueck &Co.

- Hitachi Automotive Systems

- Lucas Electrical

- Magneti Marelli

- MITSUBA Corporation

- Mitsubishi Electric Corporation

- Nikko Electric Industry Co., Ltd.

- Prestolite Electric

- Remy International

- Sawafuji Electric Co., Ltd.

- TYK Automotive Electric Co., Ltd.

- Unitech Automotive Electrical Appliance Co., Ltd.

- Valeo

- WAI Global

The Global Automotive Starter Motor Market, valued at USD 24.3 billion in 2024, is poised for remarkable growth, with a projected robust CAGR of 8.9% from 2025 to 2034. This surge is fueled by cutting-edge advancements in starter motor technologies, such as gear reduction mechanisms and lightweight designs. These innovations not only enhance efficiency but also reduce energy consumption and improve vehicle performance, aligning with the automotive industry's increasing emphasis on fuel efficiency and emissions reduction.

The market is segmented into passenger cars and commercial vehicles, with passenger cars dominating at 67% of the market share in 2024. By 2034, this segment is projected to generate an impressive USD 37.2 billion. Key factors propelling this growth include rising demand for personal mobility, rapid urbanization, and higher disposable incomes, especially in emerging markets. Furthermore, advancements in start-stop systems, designed to boost fuel efficiency and comply with stringent emission standards, are predominantly integrated into passenger vehicles. This sustained demand underscores the pivotal role of advanced and durable starter motors in modern automotive solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $24.3 billion |

| Forecast Value | $56.3 billion |

| CAGR | 8.9% |

The market is also divided between original equipment manufacturers (OEMs) and the aftermarket, with OEMs commanding a significant 73% market share in 2024. Their direct involvement in vehicle production ensures seamless integration, superior quality, and enhanced reliability. Automakers leverage cost efficiencies by sourcing starter motors in bulk and utilizing optimized supply chains. Additionally, the need to meet stringent performance and regulatory benchmarks further solidifies OEMs' dominance as providers of state-of-the-art starter motor solutions.

The U.S. automotive starter motor market held an 85% share in 2024 and is forecasted to reach USD 10.6 billion by 2034. The nation's dominance can be attributed to its well-established automotive manufacturing ecosystem and high demand for vehicles equipped with advanced technologies like start-stop systems. Regulatory measures promoting fuel efficiency have accelerated the adoption of energy-efficient starter motors. Furthermore, the presence of leading automakers and component manufacturers, coupled with robust supply chain networks, reinforces the U.S. market's leadership.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 OEMs

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising vehicle production and sales

- 3.7.1.2 Advancements in starter motor technology

- 3.7.1.3 Growth in electric and hybrid vehicles

- 3.7.1.4 Increased focus on fuel efficiency and emissions control

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High implementation costs

- 3.7.2.2 Stringent regulations

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Starter Motor, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Electric starter motor

- 5.3 Pneumatic starter motor

- 5.4 Hydraulic starter motor

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger car

- 6.3 Commercial vehicle

Chapter 7 Market Estimates & Forecast, By Power Rating, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Below 1.5 kW

- 7.3 1.5–2.5 kW

- 7.4 Above 2.5 kW

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 BorgWarner Inc.

- 10.2 Bosch

- 10.3 Delco Remy

- 10.4 DENSO

- 10.5 Dongfeng Motor Parts and Components Group Co., Ltd.

- 10.6 GDST Auto Parts

- 10.7 Hella KGaA Hueck & Co.

- 10.8 Hitachi Automotive Systems

- 10.9 Lucas Electrical

- 10.10 Magneti Marelli

- 10.11 MITSUBA Corporation

- 10.12 Mitsubishi Electric Corporation

- 10.13 Nikko Electric Industry Co., Ltd.

- 10.14 Prestolite Electric

- 10.15 Remy International

- 10.16 Sawafuji Electric Co., Ltd.

- 10.17 TYK Automotive Electric Co., Ltd.

- 10.18 Unitech Automotive Electrical Appliance Co., Ltd.

- 10.19 Valeo

- 10.20 WAI Global