|

시장보고서

상품코드

1664901

엔진 냉각용 자동차용 전동 워터 펌프 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Automotive Electric Water Pump for Engine Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

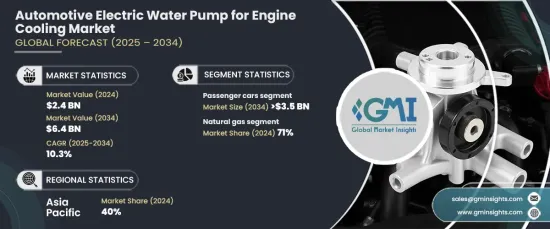

엔진 냉각용 자동차용 전동 워터 펌프 세계 시장은 2024년에 24억 달러에 달했으며, 2025년부터 2034년에 걸쳐 10.3%의 강력한 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다.

이 성장의 주요 요인은 저연비 차량에 대한 수요의 급증입니다. 세계 각국의 정부와 소비자는 연료 소비를 줄이고 환경에 미치는 영향을 줄이기 위해 에너지 효율을 중시하는 경향을 강화하고 있으며, 시장의 큰 확대를 이끌고 있습니다.

시장은 차량 유형별로 상용차와 승용차로 분류됩니다. 2024년에는 승용차 부문이 전체의 65%를 차지하고 시장을 독점하고 있으며, 2034년까지는 35억 달러에 이를 것으로 예상됩니다. 세계의 배기 가스 규제 강화로 자동차 제조업체는 내연 기관(ICE) 차량에 전동 워터 펌프와 같은 고급 냉각 솔루션을 채택해야 합니다. 이 펌프는 엔진 온도를 최적으로 유지하고 연비를 향상시키고 엔진 스트레스를 줄이고 배출 가스를 줄이는 데 필수적입니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025년-2034년 |

| 시작금액 | 24억 달러 |

| 예측 금액 | 64억 달러 |

| CAGR | 10.3% |

추진력 유형에 따라 시장은 내연 기관(ICE)과 전기자동차(EV)로 나뉩니다. 2024년에는 ICE 부문이 71%의 압도적인 시장 점유율을 차지했습니다. 소비자가 보다 조용하고 효율적인 차량과 개선된 기능을 추구함에 따라 전동 워터 펌프의 채용이 기세를 늘리고 있습니다. 이 펌프는 뛰어난 엔진 냉각을 실현할 뿐만 아니라 차량 내 난방 효율을 향상시켜 보다 편안하고 원활한 운전 경험을 제공합니다.

아시아태평양은 가장 규모가 큰 지역 시장으로 떠오르고 2024년에는 40%의 점유율을 차지했습니다. 중국과 인도 등 자동차 제조의 주요 거점으로 알려진 국가들이 첨단 엔진 냉각 기술 수요의 선진을 끊고 있습니다. 이 지역의 자동차 제조업체는 자동차의 성능과 효율에 대한 세계 표준을 충족시키기 위해 전동 워터 펌프를 내연 기관차와 전기자동차 모델 모두에 통합합니다.

보조금과 인프라 정비를 포함한 정부의 이니셔티브으로 아시아태평양에서는 EV의 보급이 가속화되고 있습니다. 이 급증은 EV의 효과적인 열 관리에 필수적인 전동 워터 펌프 수요를 촉진하고 있습니다. 세계 최대 EV 생산국인 중국은 정부 인센티브와 급속히 확대되는 전기차의 소비자층에 지지를 받고 있으며, 이 성장에 있어 매우 중요한 역할을 하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도의 산출

- 시장추계의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 소스

- 데이터 마이닝 소스

- 시장 범위와 정의

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 원재료 공급자

- 부품 공급자

- 제조업체

- 기술 제공업체

- 최종 사용자

- 공급자의 상황

- 이익률 분석

- 기술과 혁신의 전망

- 특허 분석

- 주요 뉴스 및 이니셔티브

- 규제 상황

- 가격 분석

- 영향요인

- 성장 촉진요인

- 전기자동차와 하이브리드 자동차의 보급

- 자동차의 배출가스 삭감과 연비 향상에 대한 규제 초점 강화

- 신흥 경제국의 자동차 생산 확대

- 전동 워터 펌프 설계의 기술 혁신

- 업계의 잠재적 리스크 및 과제

- 배터리 성능에 의존

- 전동 워터 펌프를 종래의 자동차 시스템에 통합할 때의 초기 비용의 높이와 복잡성

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 전압별, 2021년-2034년

- 주요 동향

- 12V

- 24V

제6장 시장 추정 및 예측 : 추진력별, 2021년-2034년

- 주요 동향

- ICE

- 가솔린

- 디젤

- 전기자동차

- 하이브리드 전기자동차(HEV)

- 배터리 전기자동차(BEV)

- 연료전지 전기자동차

제7장 시장 추정 및 예측 : 차량별, 2021년-2034년

- 주요 동향

- 승용차

- 세단

- 해치백

- SUV차

- 기타

- 상용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

제8장 시장 추정 및 예측 : 판매 채널별, 2021년-2034년

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- Aisin Seiki

- BLDC Pump

- Bosch

- Carter Fuel Systems

- Continental

- Cummins

- Davies Craig

- Denso

- Gates

- GMB Corporation

- Hanon

- Hitachi Automotive

- Mahle

- Mitsubishi Electric

- Rexroth

- Rheinmetall

- Schaeffler Technologies

- Shandong Boshan

- Valeo

- VOVYO Technology

The Global Automotive Electric Water Pump For Engine Cooling Market was valued at USD 2.4 billion in 2024 and is projected to grow at a robust CAGR of 10.3% from 2025 to 2034. This growth is primarily fueled by the surging demand for fuel-efficient vehicles. Governments and consumers worldwide are increasingly emphasizing energy efficiency to reduce fuel consumption and mitigate environmental impact, driving significant market expansion.

The market is categorized by vehicle type into commercial vehicles and passenger cars. In 2024, the passenger car segment dominated the market, accounting for 65% of the total share, and is projected to reach USD 3.5 billion by 2034. Stricter global emission regulations are compelling automakers to adopt advanced cooling solutions, such as electric water pumps, in internal combustion engine (ICE) vehicles. These pumps are critical for maintaining optimal engine temperatures, enhancing fuel efficiency, reducing engine stress, and lowering emissions-key factors in meeting rigorous environmental standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 10.3% |

Based on propulsion type, the market is divided into ICE and electric vehicles (EVs). In 2024, the ICE segment held a commanding 71% market share. As consumers increasingly demand quieter, more efficient vehicles with improved features, the adoption of electric water pumps has gained momentum. These pumps not only deliver superior engine cooling but also enhance cabin heating efficiency, offering a more comfortable and seamless driving experience.

Asia Pacific emerged as the largest regional market, holding a 40% share in 2024. Countries like China and India, recognized as major automotive manufacturing hubs, are spearheading the demand for advanced engine cooling technologies. Automakers in the region are integrating electric water pumps into both ICE and EV models to meet global standards for vehicle performance and efficiency.

Government initiatives, including subsidies and infrastructure development, are accelerating EV adoption in Asia Pacific. This surge is driving demand for electric water pumps, which are essential for effective thermal management in EVs. As the world's largest EV producer, China is playing a pivotal role in this growth, supported by government incentives and a rapidly expanding consumer base for electric vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising adoption of electric and hybrid vehicles

- 3.9.1.2 Increasing regulatory focus on reducing vehicle emissions and improving fuel efficiency

- 3.9.1.3 Expansion of automotive production in emerging economies

- 3.9.1.4 Technological innovations in electric water pump design

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Dependence on battery performance

- 3.9.2.2 High initial costs and complexity in integrating electric water pumps into traditional automotive systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Voltage, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 12V

- 5.3 24V

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.2.1 Gasoline

- 6.2.2 Diesel

- 6.3 Electric

- 6.3.1 Hybrid electric vehicles (HEVs)

- 6.3.2 Battery electric vehicles (BEVs)

- 6.3.3 Fuel cell electric vehicles

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedans

- 7.2.2 Hatchbacks

- 7.2.3 SUVs

- 7.2.4 Others

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Heavy commercial vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aisin Seiki

- 10.2 BLDC Pump

- 10.3 Bosch

- 10.4 Carter Fuel Systems

- 10.5 Continental

- 10.6 Cummins

- 10.7 Davies Craig

- 10.8 Denso

- 10.9 Gates

- 10.10 GMB Corporation

- 10.11 Hanon

- 10.12 Hitachi Automotive

- 10.13 Mahle

- 10.14 Mitsubishi Electric

- 10.15 Rexroth

- 10.16 Rheinmetall

- 10.17 Schaeffler Technologies

- 10.18 Shandong Boshan

- 10.19 Valeo

- 10.20 VOVYO Technology