|

시장보고서

상품코드

1665059

인간면역결핍바이러스 치료제 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Human Immunodeficiency Virus Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

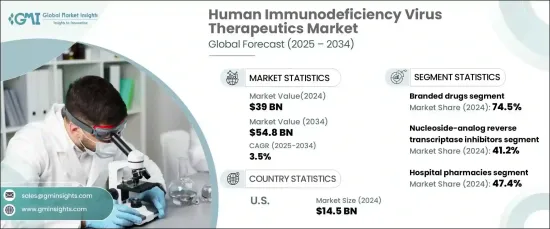

세계의 인간면역결핍바이러스 치료제 시장은 2024년에 390억 달러의 평가액에 이르렀고, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 3.5%을 나타내며 안정적인 성장을 이룰 것으로 예측되고 있습니다.

시장 확대의 주요 요인은 HIV 감염률의 상승, 치료법의 대폭적인 진보, 정부의 적극적인 노력, 유리한 규제 당국의 승인 등입니다. 이러한 요인들이 결합되어 시장의 지속적인 성장 궤도를 촉진하는데 중요한 역할을 합니다.

시장은 주로 약물의 유형에 따라 브랜드 의약품과 제네릭 의약품으로 구분됩니다. 2024년에는 브랜드 의약품이 74.5%라는 대폭적인 점유율로 시장을 선도했으며, 그 이유는 효능이 입증된 것, 오랜 임상적 신뢰성이 있는 것, HIV 치료에 있어서의 실적이 신뢰되었기 때문입니다. 합제는 투약 요법을 단순화하고 환자의 치료 계획에 대한 충격을 높이기 때문에 널리 보급되어 있습니다. 특히 바이러스량을 효과적으로 억제하기 위한 병용요법에서 중요한 역할은 시장 수요를 계속 견인하고 있으며, 향후 수년간 시장의 안정적인 성장을 확실히 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 390억 달러 |

| 예측 금액 | 548억 달러 |

| CAGR | 3.5% |

시장 유통 채널은 HIV 치료제의 도달범위와 접근성을 더욱 돋보이게 합니다. 주요 유통 부문에는 약국과 소매 약국, 온라인 약국 및 병원 약국이 포함됩니다. 2024년에는 병원 약국이 47.4%로 시장 최대 점유율을 차지했습니다. 병원 약국은 고급 항 레트로 바이러스 요법과 신중한 투여가 필요한 주사 치료를 포함하여보다 광범위한 전문 HIV 치료제를 제공하기위한 시설을 갖추고 있습니다. 의료 전문가의 감독하에, 병용 요법을 포함한 최첨단 치료를 제공할 수 있기 때문에 전문적인 케어와 배려가 필요한 환자에게 바람직한 선택이 되고 있습니다.

미국에서 HIV 치료제 시장은 2024년에 145억 달러를 창출했습니다. 이 나라는 고도로 발달한 의료 인프라의 혜택을 받고 있으며, 임상시험이나 장시간 작용형 주사요법 등 첨단 HIV 치료에 대한 액세스가 널리 확보되고 있습니다. 메디케이드와 메디케어와 같은 건강 보험 제도가 널리 보급되어 환자는 필요한 구명 치료를 받을 수 있습니다. 또한 소매 약국, 병원 시설 및 온라인 플랫폼의 광범위한 네트워크는 HIV 치료제의 원활한 유통과 입수를 촉진하고 환자가 필요한 치료법에 쉽게 액세스할 수 있도록 보장합니다.

세계의 인간 면역결핍 바이러스(HIV) 치료제 시장은 2024년에 390억 달러의 평가액에 달했고 2025년부터 2034년에 걸쳐 CAGR 3.5%에서 안정적인 성장을 이룰 것으로 예측되고 있습니다. 시장 확대의 주요 요인은 HIV 감염률 증가, 치료법의 상당한 진보, 정부의 지원책, 유리한 규제 당국의 승인입니다. 이러한 요인들이 결합되어 시장의 지속적인 성장 궤도를 촉진하는데 중요한 역할을 합니다.

시장은 주로 약물의 유형에 따라 브랜드 의약품과 제네릭 의약품으로 구분됩니다. 2024년에는 브랜드 의약품이 74.5%라는 대폭적인 점유율로 시장을 선도했으며, 그 이유는 효능이 입증된 것, 오랜 임상적 신뢰성이 있는 것, HIV 치료에 있어서의 실적이 신뢰되고 있기 때문입니다. 합제는 투약 요법을 단순화하고 환자의 치료 계획에 대한 충격을 높이기 때문에 널리 보급되어 있습니다. 특히 바이러스 양을 효과적으로 억제하는 병용 요법에서 중요한 역할은 계속 시장 수요를 견인하고 있으며, 앞으로도 안정된 시장 성장이 예상됩니다.

시장 유통 채널은 HIV 치료제의 도달범위와 접근성을 더욱 돋보이게 합니다. 주요 유통 경로는 약국, 소매 약국, 온라인 약국, 병원 약국 등입니다. 2024년에는 병원 약국이 47.4%로 가장 큰 점유율을 차지했습니다. 병원 약국은 고급 항 레트로 바이러스 요법과 신중한 투여가 필요한 주사 치료를 포함하여보다 광범위한 전문 HIV 치료제를 제공하기위한 시설을 갖추고 있습니다. 의료 전문가의 감독하에, 병용 요법을 포함한 최첨단 치료를 제공할 수 있기 때문에 전문적인 케어와 배려가 필요한 환자에게 바람직한 선택이 되고 있습니다.

미국에서 HIV 치료제 시장은 2024년에 145억 달러를 창출했습니다. 이 나라는 고도로 발달한 의료 인프라의 혜택을 받고 있으며, 임상시험이나 장시간 작용형 주사요법 등 첨단 HIV 치료에 대한 액세스가 널리 확보되고 있습니다. 메디케이드와 메디케어와 같은 건강 보험 제도가 널리 보급되어 환자는 필요한 구명 치료를 받을 수 있습니다. 또한 소매 약국, 병원 시설, 의료 기관 등의 광범위한 네트워크는 환자를 구명하는 데 필요한 치료법을 제공할 수 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도의 산출

- 시장추계의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 높은 HIV 감염률

- 치료 옵션의 진보

- 정부의 이니셔티브나 보건 프로그램에 의한 지원 확대

- 유리한 규제 당국의 승인

- 업계의 잠재적 위험 및 과제

- 고액의 치료비

- 환자의 순응도와 치료 연속성에 대한 우려

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 갭 분석

- 특허 분석

- 기술적 전망

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망

제5장 시장 추계·예측 : 약제 유형별(2021-2034년), 100만 달러

- 주요 동향

- 브랜드 의약품

- 제네릭 의약품

제6장 시장 추계·예측 : 약제 클래스별(2021-2034년), 100만 달러

- 주요 동향

- 뉴클레오사이드-아날로그 역전사효소 억제제

- 인테그라제 억제제

- 비뉴클레오사이드 역전사효소 억제제

- 프로테아제 억제제

- 진입 및 융합 억제제

- 코어수용체 길항제

제7장 시장 추계·예측 : 유통 채널별(2021-2034년), 100만 달러

- 주요 동향

- 병원 약국

- 약국 및 소매 약국

- 온라인 약국

제8장 시장 추계·예측 : 지역별(2021-2034년), 100만 달러

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- AbbVie

- Aurobindo Pharma

- Boehringer Ingelheim International GmbH

- Bristol-Myers Squibb Company

- Cipla

- Dr. Reddy's Laboratories

- F. Hoffmann-La Roche

- Gilead Sciences

- Hetero Drugs

- Johnson &Johnson

- Merck &Co

- Mylan NV(Viatris)

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

- ViiV Healthcare

The Global Human Immunodeficiency Virus Therapeutics Market reached a valuation of USD 39 billion in 2024 and is projected to experience steady growth at a CAGR of 3.5% from 2025 to 2034. The market expansion is largely driven by the rising rates of HIV infections, significant advancements in treatment options, supportive government initiatives, and favorable regulatory approvals. These factors combined are playing a crucial role in fostering the market's ongoing growth trajectory.

The market is primarily segmented by drug type into branded and generic drugs. In 2024, branded drugs led the market with a substantial share of 74.5%, attributed to their proven efficacy, long-standing clinical reliability, and trusted performance in HIV treatment. Fixed-dose combinations have been gaining widespread popularity, as they offer simplified dosing regimens that enhance patient adherence to treatment plans. Their key role in combination therapies, particularly for effectively suppressing viral loads, continues to drive demand in the market, ensuring consistent market growth in the years to come.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $39 Billion |

| Forecast Value | $54.8 Billion |

| CAGR | 3.5% |

The market's distribution channels further highlight the reach and accessibility of HIV therapeutics. The primary distribution segments include drug stores and retail pharmacies, online pharmacies, and hospital pharmacies. In 2024, hospital pharmacies held the largest share of the market, with a notable 47.4%. Hospital pharmacies are well-equipped to offer a broader selection of specialized HIV medications, including advanced antiretroviral therapies and injectable treatments that require careful administration. Their ability to provide cutting-edge treatments, including combination regimens, under the supervision of healthcare professionals makes them the preferred choice for patients who require specialized care and attention.

In the United States, the HIV therapeutics market generated USD 14.5 billion in 2024. The country benefits from a highly developed healthcare infrastructure that ensures widespread access to advanced HIV treatments, including clinical trials and long-acting injectable therapies. The widespread availability of health insurance programs, such as Medicaid and Medicare, further guarantees that patients can afford the life-saving therapies they need. Moreover, the extensive network of retail pharmacies, hospital facilities, and online platforms helps facilitate seamless distribution and availability of HIV therapeutics, ensuring that patients can easily access the treatments they require.

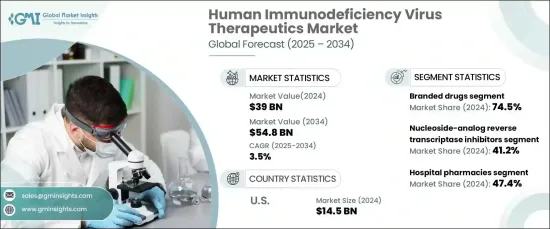

The global Human Immunodeficiency Virus (HIV) therapeutics market reached a valuation of USD 39 billion in 2024 and is projected to experience steady growth at a CAGR of 3.5% from 2025 to 2034. The market expansion is largely driven by the rising rates of HIV infections, significant advancements in treatment options, supportive government initiatives, and favorable regulatory approvals. These factors combined are playing a crucial role in fostering the market's ongoing growth trajectory.

The market is primarily segmented by drug type into branded and generic drugs. In 2024, branded drugs led the market with a substantial share of 74.5%, attributed to their proven efficacy, long-standing clinical reliability, and trusted performance in HIV treatment. Fixed-dose combinations have been gaining widespread popularity, as they offer simplified dosing regimens that enhance patient adherence to treatment plans. Their key role in combination therapies, particularly for effectively suppressing viral loads, continues to drive demand in the market, ensuring consistent market growth in the years to come.

The market's distribution channels further highlight the reach and accessibility of HIV therapeutics. The primary distribution segments include drug stores and retail pharmacies, online pharmacies, and hospital pharmacies. In 2024, hospital pharmacies held the largest share of the market, with a notable 47.4%. Hospital pharmacies are well-equipped to offer a broader selection of specialized HIV medications, including advanced antiretroviral therapies and injectable treatments that require careful administration. Their ability to provide cutting-edge treatments, including combination regimens, under the supervision of healthcare professionals makes them the preferred choice for patients who require specialized care and attention.

In the United States, the HIV therapeutics market generated USD 14.5 billion in 2024. The country benefits from a highly developed healthcare infrastructure that ensures widespread access to advanced HIV treatments, including clinical trials and long-acting injectable therapies. The widespread availability of health insurance programs, such as Medicaid and Medicare, further guarantees that patients can afford the life-saving therapies they need. Moreover, the extensive network of retail pharmacies, hospital facilities, and on

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High incidence of HIV infections

- 3.2.1.2 Advances in therapeutic treatment options

- 3.2.1.3 Growing support through government initiatives and health programs

- 3.2.1.4 Favorable regulatory approvals

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Concerns related to patient adherence and treatment continuity

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Technological landscape

- 3.8 Future market trends

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded drugs

- 5.3 Generic drugs

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Nucleoside-analog reverse transcriptase inhibitors

- 6.3 Integrase inhibitors

- 6.4 Non-nucleoside reverse transcriptase inhibitors

- 6.5 Protease inhibitors

- 6.6 Entry and fusion inhibitors

- 6.7 Coreceptor antagonists

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Drugs stores and retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 Aurobindo Pharma

- 9.3 Boehringer Ingelheim International GmbH

- 9.4 Bristol-Myers Squibb Company

- 9.5 Cipla

- 9.6 Dr. Reddy's Laboratories

- 9.7 F. Hoffmann-La Roche

- 9.8 Gilead Sciences

- 9.9 Hetero Drugs

- 9.10 Johnson & Johnson

- 9.11 Merck & Co

- 9.12 Mylan N.V. (Viatris)

- 9.13 Sun Pharmaceutical Industries

- 9.14 Teva Pharmaceutical Industries

- 9.15 ViiV Healthcare