|

시장보고서

상품코드

1665067

자동차용 연료전지 모니터 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Automotive Fuel Cell Monitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

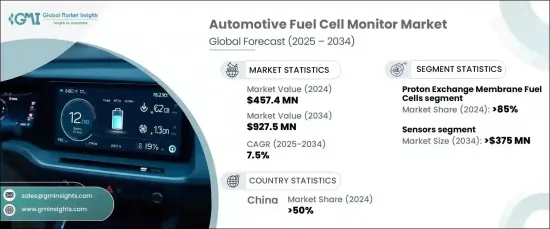

세계의 자동차용 연료전지 모니터 시장은 2024년에는 4억 5,740만 달러로 평가되었고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 7.5%로 성장할 것으로 예측됩니다.

세계 정부가 배기 가스 규제를 강화하고 야심찬 탄소 중립 목표를 지속적으로 설정함에 따라 자동차 제조업체는 제로 방출 기술, 특히 연료전지 시스템에 대한 투자를 늘리고 있습니다. 이러한 깨끗하고 지속 가능한 에너지 솔루션에 대한 수요의 급증이 자동차용 연료전지 모니터 시장의 성장을 뒷받침하고 있습니다.

센서 기술의 발전은 연료전지 모니터를 변화시키는 데 있어 매우 중요한 역할을 하고 있습니다. 이러한 기술 혁신을 통해 연료전지의 성능과 건전성을 보다 정확하고 실시간으로 추적할 수 있습니다. 새로운 반도체 기술은 인공지능과 머신러닝의 힘과 결합하여 잠재적인 고장을 예측하고 성능을 최적화하며 연료전지 부품의 수명을 연장하는 모니터링 시스템을 강화합니다. 이러한 혁신은 연료전지 모니터링을 단순화하고 비용을 절감하며 연료전지 시스템의 신뢰성과 효율성을 크게 향상시킵니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 4억 5,740만 달러 |

| 예측 금액 | 9억 2,750만 달러 |

| CAGR | 7.5% |

시장은 연료전지 유형별로 구분되며, 주요 카테고리에는 알칼리 연료전지(AFC), 고체 고분자형 연료전지(PEMFC), 인산형 연료전지(PAFC), 고체 산화물 연료전지(SOFC)가 포함됩니다. 2024년에는 고체 고분자형 연료전지(PEMFC) 분야가 85%의 점유율을 차지해 시장을 독점했습니다. 이 분야는 2034년까지 7억 5,000만 달러를 창출할 것으로 예상됩니다. 연구 개발은 내구성 향상, 전도성 개선, 온도 변화에 대한 내성 향상을 실현하는 차세대 막 재료의 개발로 크게 전진하고 있으며, PEMFC 기술을 더욱 진화시키고 있습니다.

자동차 연료전지 모니터 시장은 또한 제어 유닛, 센서, 통신 모듈 및 기타를 포함한 구성 요소별로 분류됩니다. 센서 분야는 2034년까지 3억 7,500만 달러를 창출할 것으로 예측됩니다. 특히 온도 센서는 연료전지 시스템 내에서 높은 정밀도와 멀티 포인트 모니터링 기능을 제공하기 때문에 상당한 업그레이드가 이루어지고 있습니다. 분산형 광섬유 감지와 고급 반도체 센서의 통합으로 이러한 온도 센서는 현재 중요한 연료전지 부품의 실시간 매핑을 제공할 수 있습니다. 약간의 온도 변화를 감지하면 열 스트레스를 방지하고 연료전지 시스템의 전반적인 성능과 수명을 최적화할 수 있습니다.

2024년 중국은 세계의 자동차용 연료전지 모니터 시장에서 50%의 압도적 점유율을 차지했습니다. 중국 정부는 연료전지 차량의 채용을 촉진하기 위해 까다로운 보조금, 세제 우대 조치 및 국가 개발 계획을 제공하며 이 성장의 주요 원동력이되었습니다. 수소 인프라 개발과 현지 생산 능력 향상에 중점을 둔 중국은 수소 자동차 기술의 세계 리더로서의 지위를 확립하고 있습니다. 중국의 국유기업과 비공개회사 모두 수소자동차의 효율, 신뢰성, 비용효과를 높이는 최첨단 연료전지 모니터링 시스템을 개발하기 위해 많은 투자를 받고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도의 산출

- 시장추계의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 정의

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 부품 제조업체

- 연료전지 시스템 제공업체

- 자동차 OEM

- 기술 통합

- 최종 용도

- 비용 내역

- 이익률 분석

- 차별화 기술

- 고급 센서 통합

- AI에 의한 진단

- 모듈식 시스템 설계

- 다층 안전 시스템

- 기타

- 주요 뉴스와 대처

- 특허 분석

- 규제 상황

- 영향요인

- 성장 촉진요인

- 세계의 탈탄소화 대처

- 차량 센싱 기술의 진보

- 연료전지의 대폭적인 비용 절감

- 연료전지차 인프라 투자 확대

- 업계의 잠재적 위험 및 과제

- 연료전지 모니터의 복잡한 기술 통합

- 경쟁 배터리 전기 기술

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계·예측 : 차량별(2021-2034년), 10억 달러

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV차

- 상용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

제6장 시장 추계·예측 : 연료전지별(2021-2032년), 10억 달러

- 주요 동향

- 양서앚 교환막 연료전지(PEMFC)

- 고체 산화물 연료전지(SOFC)

- 알칼리성 연료전지(AFC)

- 인산 연료전지(PAFC)

제7장 시장 추계·예측 : 구성 요소별(2021-2032년), 10억 달러

- 주요 동향

- 센서

- 제어 유닛

- 통신 모듈

- 기타

제8장 시장 추계·예측 : 모니터링 기능별(2021-2032년), 10억 달러

- 주요 동향

- 수소 모니터링

- 연료전지 스택 모니터링

- 열 관리

- 공기 공급

- 누출 감지

제9장 시장 추계·예측 : 판매 채널별(2021-2032년), 10억 달러

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계·예측 : 지역별(2021-2032년), 10억 달러

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- AVL

- Bosch

- Dilico Engineering

- dSpace

- Gamma Technologies

- Hans Turck

- Horiba

- H-TEC Education

- Infineon

- IST

- Kolibrik

- Marquardt

- Nedstack

- PST Process Sensing

- Smart Testsolutions

- Texas Instruments

- Vaisala

- Vitronic

- Zeiss

The Global Automotive Fuel Cell Monitor Market was valued at USD 457.4 million in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 7.5% from 2025 to 2034. As governments across the globe continue to tighten emissions regulations and set ambitious carbon neutrality targets, automakers are increasing their investments in zero-emission technologies, especially fuel cell systems. This surge in demand for clean, sustainable energy solutions is driving the growth of the automotive fuel cell monitor market.

Advancements in sensor technology are playing a pivotal role in transforming fuel cell monitoring. These innovations allow for more accurate, real-time tracking of fuel cell performance and health. Emerging semiconductor technologies, coupled with the power of artificial intelligence and machine learning, are enhancing monitoring systems to predict potential failures, optimize performance, and extend the lifespan of fuel cell components. These breakthroughs are simplifying fuel cell monitoring, driving down costs, and significantly improving both the reliability and efficiency of fuel cell systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $457.4 Million |

| Forecast Value | $927.5 Million |

| CAGR | 7.5% |

The market is segmented by fuel cell type, with key categories including Alkaline Fuel Cells (AFC), Proton Exchange Membrane Fuel Cells (PEMFC), Phosphoric Acid Fuel Cells (PAFC), and Solid Oxide Fuel Cells (SOFC). In 2024, the Proton Exchange Membrane Fuel Cells (PEMFC) segment dominated the market, holding an 85% share. This segment is expected to generate USD 750 million by 2034. Researchers are making significant strides in developing next-generation membrane materials that offer enhanced durability, improved conductivity, and better resistance to temperature fluctuations, further advancing PEMFC technology.

The automotive fuel cell monitor market is also categorized by components, including control units, sensors, communication modules, and others. The sensors segment is projected to generate USD 375 million by 2034. Notably, temperature sensors are undergoing significant upgrades, offering higher precision and multi-point monitoring capabilities within fuel cell systems. With the integration of distributed fiber optic sensing and advanced semiconductor sensors, these temperature sensors can now provide real-time mapping of crucial fuel cell components. By detecting even small temperature variations, they help prevent thermal stress and optimize the overall performance and longevity of fuel cell systems.

In 2024, China held a dominant 50% share of the global automotive fuel cell monitor market. The Chinese government has been a major driver of this growth, offering generous subsidies, tax incentives, and national development plans to promote the adoption of fuel cell vehicles. With a strong focus on developing hydrogen infrastructure and advancing local manufacturing capabilities, China is positioning itself as a global leader in hydrogen-powered vehicle technology. Both state-owned enterprises and private companies in China are receiving significant investments to develop cutting-edge fuel cell monitoring systems that enhance the efficiency, reliability, and cost-effectiveness of hydrogen-powered vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component manufacturers

- 3.2.2 Fuel cell system providers

- 3.2.3 Automotive OEM

- 3.2.4 Technology integrators

- 3.2.5 End Use

- 3.3 Cost breakdown

- 3.4 Profit margin analysis

- 3.5 Technology differentiators

- 3.5.1 Advanced sensor integrations

- 3.5.2 AI-driven diagnostics

- 3.5.3 Modular system design

- 3.5.4 Multi-layered safety systems

- 3.5.5 Others

- 3.6 Key news & initiatives

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Global decarbonization initiatives

- 3.9.1.2 Advancements in vehicle sensing technologies

- 3.9.1.3 Significant cost reductions in fuel cells

- 3.9.1.4 Growing fuel cell vehicle infrastructure investments

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Complex technical integration of fuel cell monitors

- 3.9.2.2 Competitive battery electric technologies

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light Commercial Vehicles (LCV)

- 5.3.2 Heavy Commercial Vehicles (HCV)

Chapter 6 Market Estimates & Forecast, By Fuel Cell, 2021 - 2032 ($Bn, Units)

- 6.1 Key trends

- 6.2 Proton Exchange Membrane Fuel Cells (PEMFC)

- 6.3 Solid Oxide Fuel Cells (SOFC)

- 6.4 Alkaline Fuel Cells (AFC)

- 6.5 Phosphoric Acid Fuel Cells (PAFC)

Chapter 7 Market Estimates & Forecast, By Component, 2021 - 2032 ($Bn, Units)

- 7.1 Key trends

- 7.2 Sensors

- 7.3 Control unit

- 7.4 Communication modules

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Monitoring Function, 2021 - 2032 ($Bn, Units)

- 8.1 Key trends

- 8.2 Hydrogen monitoring

- 8.3 Fuel cell stack monitoring

- 8.4 Thermal management

- 8.5 Air supply

- 8.6 leakage detection

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2032 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2032 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AVL

- 11.2 Bosch

- 11.3 Dilico Engineering

- 11.4 dSpace

- 11.5 Gamma Technologies

- 11.6 Hans Turck

- 11.7 Horiba

- 11.8 H-TEC Education

- 11.9 Infineon

- 11.10 IST

- 11.11 Kolibrik

- 11.12 Marquardt

- 11.13 Nedstack

- 11.14 PST Process Sensing

- 11.15 Smart Testsolutions

- 11.16 Texas Instruments

- 11.17 Vaisala

- 11.18 Vitronic

- 11.19 Zeiss