|

시장보고서

상품코드

1665240

모노폴라 전기 수술 기기 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Monopolar Electrosurgery Instrument Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

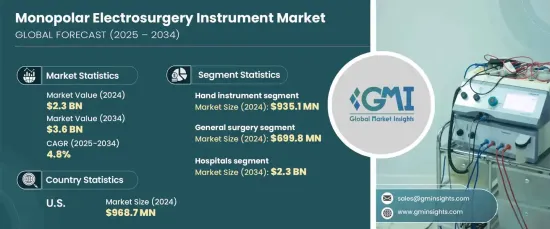

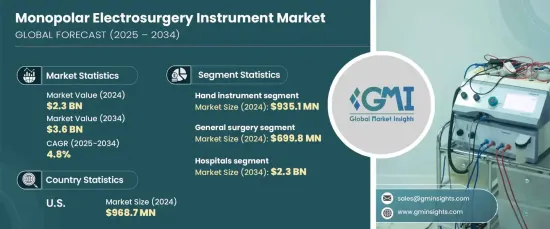

세계의 모노폴라 전기 수술 기기 시장은 2024년 23억 달러에 이르렀으며, 2025-2034년까지 CAGR 4.8%로 예측되어 강력한 성장이 전망되고 있습니다.

이 성장의 원동력은 낮은 침습 수술에 대한 수요가 증가하고, 만성 질환의 유병률이 증가하고, 세계 의료 투자의 확대입니다. 게다가 기술의 진보와 정밀한 수술 기기에 대한 요구 증가는 시장의 상승 궤도에 박차를 가하고 있습니다.

낮은 침습 수술은 일반 수술, 부인과, 비뇨기과, 소화기과 같은 다양한 의료 전문 분야에서 표준 기술입니다. 모노폴라 전기 수술 도구는 정확도, 효율성 및 수술 중 조직 손상을 최소화하는 능력으로 인해 이러한 부문에서 중요한 역할을 수행합니다. 조직의 절단, 응고, 건조에 범용성이 있기 때문에 일상적인 수술이나 복잡한 수술에도 필수적입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 23억 달러 |

| 예측 금액 | 36억 달러 |

| CAGR | 4.8% |

시장은 수용 기기, 전기 수술용 발전기, 분산 전극 및 액세서리를 포함한 제품 유형으로 구분됩니다. 핸드 기기 부문은 시장을 선도하고 있으며 2024년 매출이 9억 3,510만 달러였습니다. 이 장비는 많은 수술 부문에서 널리 사용되며 섬세한 절차에 필요한 정확성과 컨트롤을 제공합니다. 개복 수술과 낮은 침습 수술 모두에 적응할 수 있기 때문에 광범위한 의료 요구에 대응하고 여전히 지배적인 부문입니다.

용도별로는 일반 수술, 심장혈관 수술, 부인과, 신경 수술 등으로 나눌 수 있습니다. 일반 수술은 2024년 6억 9,980만 달러를 차지했으며 예측 기간 동안 CAGR 4.6%로 성장할 것으로 예측됩니다. 모노폴라 전기 수술 기기는 연부 조직의 관리, 지혈, 수술 시간의 단축에 있어서 효율적이기 때문에 이 부문에서 높게 평가되고 있습니다. 수술 결과를 향상시키고 환자의 회복을 가속화하는 능력은 병원과 수술센터 전체 수요를 계속 견인하고 있습니다.

미국의 모노폴라 전기 수술기기 시장은 2024년 9억 6,870만 달러를 창출했습니다. 이 시장은 2034년까지 연평균 복합 성장률(CAGR) 4.2%로 성장할 것으로 예상되며, 주요 제조업체의 존재와 확립된 의료 인프라에 지지를 받고 있습니다. 만성 질환의 유병률 증가와 낮은 침습 수술의 채용 증가가 이러한 기기에 대한 수요의 지속에 기여하고 있습니다. 게다가 첨단 의료 훈련과 전문 지식의 이용이 가능하다는 것이 모노폴라 전기 수술 기기의 채용을 더욱 가속화시켜 미국이 세계 시장에서 주도적 지위를 강화하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- 산업에 미치는 영향요인

- 성장 촉진요인

- 낮은 침습 수술에 대한 수요 증가

- 전기 수술 기술의 진보

- 만성질환의 유병률 증가

- 세계의 의료 지출 증가

- 산업의 잠재적 리스크 및 과제

- 열 손상이 높은 위험

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 상환 시나리오

- 기술

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업 점유율 분석

- 주요 시장 진출기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정·예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 핸드 기기

- 전기 수술용 발전기

- 분산 전극

- 부속품

제6장 시장 추정·예측 : 용도별, 2021-2034년

- 주요 동향

- 일반 수술

- 심장혈관 수술

- 부인과 수술

- 뇌신경 수술

- 기타

제7장 시장 추정·예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타

제8장 시장 추정·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Apyx Medical

- B.Braun

- BOWA MEDICAL

- CONMED

- Encision

- Erbe Elektromedizin

- Johnson & Johnson

- KLS Martin Group

- Medtronic

- Meyer-Haake

- Olympus

- Stryker

The Global Monopolar Electrosurgery Instrument Market reached USD 2.3 billion in 2024 and is expected to experience strong growth, with a projected CAGR of 4.8% from 2025 to 2034. This growth is driven by the increasing demand for minimally invasive procedures, the rising prevalence of chronic diseases, and expanding healthcare investments around the world. Additionally, technological advancements and the growing need for precise surgical instruments are fueling the market's upward trajectory.

Minimally invasive procedures have become standard practice across various medical specialties such as general surgery, gynecology, urology, and gastroenterology. Monopolar electrosurgery instruments play a crucial role in these fields due to their precision, efficiency, and ability to minimize tissue damage during surgical procedures. Their versatility in cutting, coagulating, and desiccating tissues makes them indispensable for both routine and complex surgeries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 4.8% |

The market is segmented into product types, including hand instruments, electrosurgical generators, dispersive electrodes, and accessories. The hand instrument segment led the market with a revenue of USD 935.1 million in 2024. These instruments are widely used across numerous surgical disciplines, offering the precision and control required for delicate procedures. Their adaptability to both open and minimally invasive surgeries ensures they remain the dominant segment, addressing a wide array of medical needs.

In terms of application, the market is divided into general surgery, cardiovascular surgery, gynecology, neurosurgery, and others. General surgery accounted for USD 699.8 million in 2024 and is projected to grow at a CAGR of 4.6% during the forecast period. Monopolar electrosurgery instruments are highly regarded in this segment for their efficiency in managing soft tissues, providing hemostasis, and reducing surgical time. Their ability to enhance surgical outcomes and promote faster patient recovery continues to drive demand across hospitals and surgical centers.

The U.S. monopolar electrosurgery instrument market generated USD 968.7 million in 2024. This market is expected to grow at a CAGR of 4.2% through 2034, supported by the presence of leading manufacturers and a well-established healthcare infrastructure. The growing prevalence of chronic conditions and the increasing adoption of minimally invasive procedures contribute to sustained demand for these instruments. Additionally, the availability of advanced medical training and expertise further accelerates the adoption of monopolar electrosurgery instruments, reinforcing the U.S.'s leadership position in the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for minimally invasive procedures

- 3.2.1.2 Advancements in electrosurgical technologies

- 3.2.1.3 Growing prevalence of chronic diseases

- 3.2.1.4 Rising global healthcare expenditure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk of thermal injuries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hand instrument

- 5.3 Electrosurgical generators

- 5.4 Dispersive electrodes

- 5.5 Accessories

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Cardiovascular surgery

- 6.4 Gynecology surgery

- 6.5 Neurosurgery

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Apyx Medical

- 9.2 B.Braun

- 9.3 BOWA MEDICAL

- 9.4 CONMED

- 9.5 Encision

- 9.6 Erbe Elektromedizin

- 9.7 Johnson & Johnson

- 9.8 KLS Martin Group

- 9.9 Medtronic

- 9.10 Meyer-Haake

- 9.11 Olympus

- 9.12 Stryker