|

시장보고서

상품코드

1665285

우주 물류 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Space Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

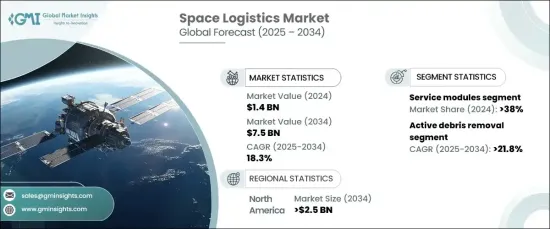

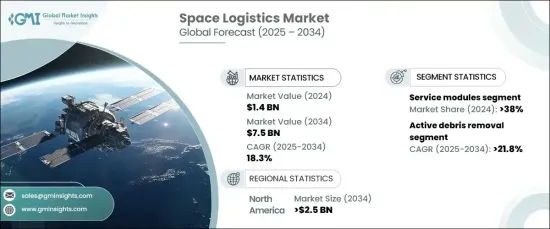

세계의 우주 물류 시장은 2024년에 14억 달러로 평가되었고, 2025년부터 2034년까지 CAGR은 18.3%로 예측되며 강력한 성장을 이룰 전망입니다. 이 성장은 위성 배치, 궤도 서비스, 우주 탐사 프로그램에 대한 수요 증가가 주요 요인입니다. 재사용 가능한 발사 기술의 혁신은 커뮤니케이션 및 지구관측을 위한 위성 별자리의 전개가 증가함에 따라 우주 공간에서의 효율적인 운송 및 운영 지원의 필요성을 크게 밀어 올리고 있습니다. 또한 우주 여행과 우주 채굴 등의 상업 벤처와 달과 화성을 목표로 하는 정부 주도의 야심적인 미션의 대두가 기술의 진보를 촉진하고 새로운 성장 기회를 가져오고 있습니다.

우주 물류 시장은 서비스 모듈, 미션 확장 포드(MEP), 화물 모듈, 로봇 암과 조작자, 스페이스 태그 등 다양한 유형으로 구분됩니다. 2024년에는 서비스 모듈이 38% 시장 점유율을 차지하며 큰 성장이 예상됩니다. 이러한 모듈은 추진, 전력, 통신 시스템과 같은 중요한 기능을 제공함으로써 위성의 운영을 유지하는 데 필수적입니다. 위성 별자리의 배치가 확대됨에 따라 서비스 모듈은 위성의 수명을 연장하고 궤도의 지속가능성을 지원하는 데 중요한 역할을 하며,이 부문에서의 급속한 보급을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 14억 달러 |

| 예측 금액 | 75억 달러 |

| CAGR | 18.3% |

이 시장은 또한 수명 연장, 마지막 마일 딜리버리, 액티브 파편 제거, 우주 상황 인식, 궤도 조립 및 제조 등 주요 부문을 포함한 운영별로 구분됩니다. 액티브 파편 제거 부문은 2034년까지 연평균 복합 성장률(CAGR) 21.8%라는 경이적인 성장이 예측되고 있습니다. 이 성장에는 우주 파편 관리 시스템을 강화하는 자율 로봇 공학과 인공지능(AI) 기술의 발전이 기여합니다. 로봇 암, 그물, 몰리와 같은 최첨단 도구는 사용되지 않는 위성과 파편을 포착하기 위해 개발되었으며, AI를 탑재한 알고리즘은 복잡한 궤도 환경에서의 탐색과 운영 정밀도를 향상시킵니다.

북미의 우주 물류 시장은 2034년까지 25억 달러에 이를 것으로 예측됩니다. 특히 미국 시장은 위성 배치 수요 증가와 우주 인프라의 진보에 의해 큰 성장을 이루고 있습니다. 재사용 가능한 발사 로켓의 채용은 운영 비용을 줄이고 발사 빈도를 증가시키는 데 중요한 역할을 하며 우주 물류의 운영을 보다 효율적이고 비용 효율적입니다.

목차

제1장 조사 방법 및 조사 범위

- 시장 범위 및 정의

- 기본 추정 및 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 자료

- 유료 정보원

- 공적 정보원

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 변혁

- 장래 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향 요인

- 성장 촉진요인

- 위성 발사 수요 증가

- 우주 수송 및 인프라의 진보

- 재사용 가능한 발사 시스템 및 우주선 증가

- 우주에서의 복잡한 페이로드 전개에 대한 수요 증가

- 위성 플릿 전개 및 관리를 위한 서비스로서 우주와 유연한 모델로의 시프트

- 산업의 잠재적 리스크 및 과제

- 우주 사업의 고비용

- 우주 교통 관리 및 파편 완화

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 미션 확대 포드(MEP)

- 화물 모듈

- 서비스 모듈

- 로봇 암 및 매니퓰레이터

- 스페이스 태그

제6장 시장 추정 및 예측 : 오퍼레이션별(2021-2034년)

- 주요 동향

- 라스트 마일 딜리버리

- 우주 상황 인식

- 수명 연장

- 액티브 파편 제거

- 궤도상 조립 및 제조

제7장 시장 추정 및 예측 : 궤도별(2021-2034년)

- 주요 동향

- 지구 근방 궤도

- 지구 저궤도

- 정지궤도

제8장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 상업

- 정부 및 방위

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Arianespace

- Astroscale

- Atomos Space

- Blue Origin

- ClearSpace

- D-Orbit

- Exolaunch

- Japan Aerospace Exploration Agency

- Lockheed Martin

- Maxar Technologies

- Northrop Grumman

- Rocket Lab

- SpaceX

- Thales Alenia Space

The Global Space Logistics Market, valued at USD 1.4 billion in 2024, is set to experience robust growth with a projected compound annual growth rate (CAGR) of 18.3% from 2025 to 2034. This growth is largely driven by the increasing demand for satellite deployment, in-orbit servicing, and space exploration programs. Innovations in reusable launch technologies, coupled with the rising deployment of satellite constellations for communication and Earth observation, have significantly boosted the need for efficient transportation and operational support in space. Furthermore, the rise of commercial ventures, such as space tourism and mining, along with ambitious government-led missions to the Moon and Mars, are catalyzing technological advancements and opening up new growth opportunities.

The space logistics market is segmented into various types, including service modules, Mission Extension Pods (MEPs), cargo modules, robotic arms and manipulators, and space tugs. In 2024, the service modules segment held a substantial 38% market share and is expected to see significant growth. These modules have become essential for maintaining satellite operations by providing critical functions such as propulsion, power, and communication systems. As the deployment of satellite constellations expands, service modules are playing a key role in extending satellite lifespans and supporting orbital sustainability, driving their rapid adoption across the sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 billion |

| Forecast Value | $7.5 billion |

| CAGR | 18.3% |

The market is also segmented by operation, with key areas including life extension, last-mile delivery, active debris removal, space situational awareness, and on-orbit assembly and manufacturing. The active debris removal segment is forecasted to grow at an impressive CAGR of 21.8% through 2034. This growth is fueled by advancements in autonomous robotics and artificial intelligence (AI) technologies, which enhance space debris management systems. Cutting-edge tools such as robotic arms, nets, and harpoons are being developed to capture unused satellites and debris, while AI-powered algorithms improve navigation and operational precision in complex orbital environments.

North America space logistics market is projected to reach USD 2.5 billion by 2034. The U.S. market, in particular, is experiencing significant growth due to the increasing demand for satellite deployment and advancements in space infrastructure. The adoption of reusable launch vehicles has played a critical role in reducing operational costs and increasing launch frequencies, making space logistics operations more efficient and cost-effective.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increased satellite launch demand

- 3.6.1.2 Advancements in space transportation and infrastructure

- 3.6.1.3 Growing reusable launch systems and spacecraft

- 3.6.1.4 Rising demand for complex payload deployment in space

- 3.6.1.5 Shift toward space as a service and flexible models for deploying and managing satellite fleets

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs of space operations

- 3.6.2.2 Space traffic management and debris mitigation

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Mission extension pods (MEPs)

- 5.3 Cargo modules

- 5.4 Service modules

- 5.5 Robotic arms and manipulators

- 5.6 Space tugs

Chapter 6 Market Estimates & Forecast, By Operation, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Last mile delivery

- 6.3 Space situational awareness

- 6.4 Life-extension

- 6.5 Active debris removal

- 6.6 On-orbit assembly and manufacturing

Chapter 7 Market Estimates & Forecast, By Orbit, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Near earth orbit

- 7.3 Lower earth orbit

- 7.4 Geostationary orbit

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government and defense

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Arianespace

- 10.2 Astroscale

- 10.3 Atomos Space

- 10.4 Blue Origin

- 10.5 ClearSpace

- 10.6 D-Orbit

- 10.7 Exolaunch

- 10.8 Japan Aerospace Exploration Agency

- 10.9 Lockheed Martin

- 10.10 Maxar Technologies

- 10.11 Northrop Grumman

- 10.12 Rocket Lab

- 10.13 SpaceX

- 10.14 Thales Alenia Space