|

시장보고서

상품코드

1665335

자동차용 열전발전기 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Thermoelectric Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

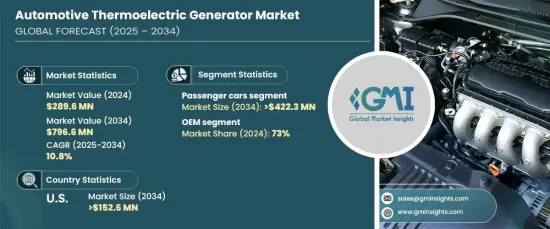

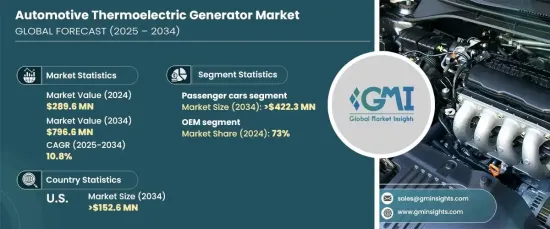

세계의 자동차 열전발전기 시장은 2024년에는 2억 8,960만 달러에 달하며, 2025-2034년 CAGR은 10.8%로 예측되며, 강력한 성장을 달성할 전망입니다. 이러한 성장의 원동력은 연료비 상승과 자동차 배기가스 감축을 위한 정부 규제 강화에 기인합니다. 이에 따라 연료 효율을 높이고 환경에 미치는 영향을 최소화하는 기술에 대한 수요가 급증하고 있습니다.

이러한 시장 확대의 가장 큰 요인은 전기자동차와 하이브리드차의 인기가 높아지고 있기 때문입니다. 이러한 첨단 자동차는 배터리 성능과 주행거리를 최적화하는 에너지 관리 시스템에 의존하고 있습니다. 배기 시스템의 폐열을 사용 가능한 전기로 변환하는 ATEG는 이러한 최적화에 매우 중요한 역할을 합니다. 보조 시스템에 전력을 공급하고 배터리 충전을 지원함으로써 이 발전기는 최신 자동차의 에너지 효율 향상에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 2억 8,960만 달러 |

| 예상 금액 | 7억 9,660만 달러 |

| CAGR | 10.8% |

차종별로는 승용차, 상용차, 하이브리드 및 전기자동차로 구분됩니다. 승용차는 2024년 시장 점유율의 57%를 차지하며 시장을 선도했습니다. 이 부문은 승용차 대량 생산과 저연비 기술에 대한 수요 증가에 힘입어 2034년까지 4억 2,230만 달러에 달할 것으로 예상됩니다. 승용차에 ATEG가 널리 채택되면 에너지 회수 시스템의 기술 혁신과 통합에 큰 기회가 생겨 이 부문의 지속적인 성장을 보장할 수 있습니다.

시장은 유통 채널에 따라 주문자 상표 부착 제품 제조업체(OEM)와 애프터마켓으로 분류되며, 2024년에는 OEM이 73%의 점유율을 차지하며, 이러한 추세는 예측 기간 중 지속될 것으로 전망됩니다. 호환성과 최적화된 성능을 보장하는 데 탁월합니다. OEM은 자동차 제조업체의 대량 주문에 대응함으로써 비용 효율성을 달성하는 동시에 이러한 기술의 채택을 가속화할 수 있습니다. 또한 OEM의 기술적 전문성을 통해 특정 차량 아키텍처에 맞게 시스템을 설계할 수 있으며, 전반적인 효율성과 신뢰성을 향상시킬 수 있습니다.

미국의 자동차용 열전발전기 시장은 2024년 86%의 점유율을 차지하며, 2034년에는 1억 5,260만 달러에 달할 것으로 예측됩니다. 기업 평균 연비(CAFE) 기준을 포함한 엄격한 연비 및 배기가스 규제가 이 수요를 촉진하는 주요 요인으로 작용하고 있습니다. 미국 시장은 또한 첨단 연비 시스템을 장착한 프리미엄 및 고급 차량에 대한 높은 수요로 인해 혜택을 누리고 있습니다. 또한, 연구 개발에 대한 막대한 투자와 주요 ATEG 제조업체의 존재는 기술 혁신을 촉진하고 시장의 성장 궤도를 뒷받침하고 있습니다.

보고서 내용

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 어프로치

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도 산출

- 시장 추정의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 정의

제2장 개요

제3장 산업 인사이트

- 에코시스템 분석

- 기술 프로바이더

- 부품 공급업체

- 제조업체

- OEM

- 공급업체 상황

- 이익률 분석

- 기술 혁신 상황

- 주요 뉴스 & 구상

- 규제 상황

- 영향요인

- 촉진요인

- 연료 효율에 대한 수요 증가

- 엄격한 배기가스 규제

- 전기자동차와 하이브리드차의 채택 확대

- 열전재료의 기술 진보

- 산업의 잠재적 리스크·과제

- 기술의 높은 초기 비용

- 소비자 사이에서의 낮은 인지도

- 촉진요인

- 성장 가능성 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정·예측 : 재료별, 2021-2034년

- 주요 동향

- 텔루르화 비스무트

- 텔루르화 납

- 실리콘 게르마늄

- 기타

제6장 시장 추정·예측 : 차량별, 2021-2034년

- 주요 동향

- 승용차

- 상용차

- 하이브리드차·전기자동차

제7장 시장 추정·예측 : 기술별, 2021-2034년

- 주요 동향

- 폐열 회수

- 발전

- 배터리 관리

제8장 시장 추정·예측 : 유통 채널별, 2021-2034년

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추정·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트

- 남아프리카공화국

- 사우디아라비아

제10장 기업 개요

- Alphabet Energy

- European Thermodynamics

- Faurecia

- Ferrotec Holdings Corporation

- Gentherm Incorporated

- Hi-Z Technology, Inc.

- II-VI Marlow

- KELK Ltd.

- Komatsu Ltd.

- Laird Thermal Systems

- SANGO Co., Ltd.

- Tenneco Inc.

- Thermonamic Electronics(Jiangxi) Corp., Ltd.

- Valeo

- Yamaha Motor Co., Ltd.

The Global Automotive Thermoelectric Generator Market, valued at USD 289.6 million in 2024, is set to experience robust growth, projected at a CAGR of 10.8% from 2025 to 2034. This growth is driven by the rising costs of fuel and increasingly stringent government regulations aimed at reducing vehicle emissions. As a result, the demand for technologies that enhance fuel efficiency and minimize environmental impact is surging.

A significant driver of this market expansion is the growing popularity of electric and hybrid vehicles. These advanced vehicles rely on energy management systems to optimize battery performance and driving range. ATEGs, which convert waste heat from exhaust systems into usable electricity, play a pivotal role in this optimization. By powering auxiliary systems and supporting battery charging, these generators contribute to enhanced energy efficiency in modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $289.6 Million |

| Forecast Value | $796.6 Million |

| CAGR | 10.8% |

In terms of vehicle type, the market is segmented into passenger cars, commercial vehicles, and hybrid and electric vehicles. Passenger cars led the market in 2024, commanding 57% of the market share. This segment is forecasted to generate USD 422.3 million by 2034, fueled by the mass production of passenger vehicles and the increasing demand for fuel-efficient technologies. The widespread adoption of ATEGs in passenger cars creates substantial opportunities for innovation and integration of energy recovery systems, ensuring continuous growth in this segment.

The market is further categorized based on sales channels into original equipment manufacturers (OEMs) and aftermarket. In 2024, OEMs dominated with a 73% share, a trend expected to persist throughout the forecast period. OEMs excel in seamlessly incorporating ATEGs into vehicles during the manufacturing process, ensuring compatibility and optimized performance. By fulfilling bulk orders for automakers, OEMs achieve cost efficiencies while accelerating the adoption of these technologies. Additionally, their technical expertise enables them to design systems tailored to specific vehicle architectures, enhancing overall efficiency and reliability.

In the United States, the automotive thermoelectric generator market held an impressive 86% share in 2024 and is projected to reach USD 152.6 million by 2034. Stringent fuel efficiency and emissions regulations, including the Corporate Average Fuel Economy (CAFE) standards, are key drivers of this demand. The U.S. market also benefits from a high demand for premium and luxury vehicles, which increasingly incorporate advanced fuel-saving systems. Furthermore, significant investments in research and development, coupled with the presence of leading ATEG manufacturers, foster innovation and support the market's growth trajectory.

Report Content

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 OEMs

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing demand for fuel efficiency

- 3.7.1.2 Stringent emission regulations

- 3.7.1.3 Growing adoption of electric and hybrid vehicles

- 3.7.1.4 Technological advancements in thermoelectric materials

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial cost of technology

- 3.7.2.2 Limited awareness among consumers

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Bismuth telluride

- 5.3 Lead telluride

- 5.4 Silicon germanium

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Commercial vehicles

- 6.4 Hybrid and electric vehicles

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Waste heat recovery

- 7.3 Power generation

- 7.4 Battery management

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alphabet Energy

- 10.2 European Thermodynamics

- 10.3 Faurecia

- 10.4 Ferrotec Holdings Corporation

- 10.5 Gentherm Incorporated

- 10.6 Hi-Z Technology, Inc.

- 10.7 II-VI Marlow

- 10.8 KELK Ltd.

- 10.9 Komatsu Ltd.

- 10.10 Laird Thermal Systems

- 10.11 SANGO Co., Ltd.

- 10.12 Tenneco Inc.

- 10.13 Thermonamic Electronics (Jiangxi) Corp., Ltd.

- 10.14 Valeo

- 10.15 Yamaha Motor Co., Ltd.