|

시장보고서

상품코드

1665351

자동차용 삼원촉매 컨버터 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Three-Way Catalytic Converter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

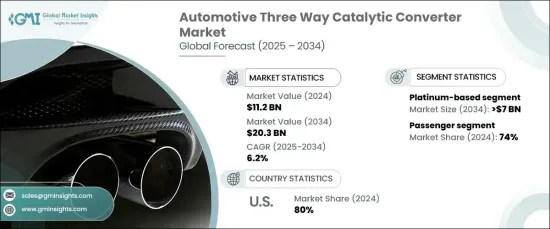

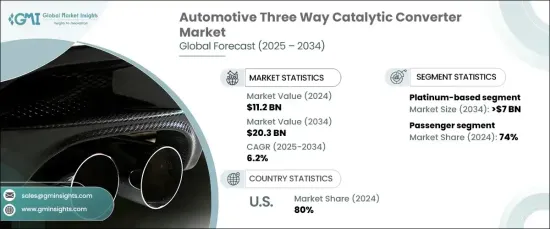

세계의 자동차용 삼원촉매 컨버터 시장은 2024년에는 112억 달러에 달하며, 2025-2034년에 CAGR 6.2%로 견고하게 확대할 전망입니다. 이러한 성장은 촉매 컨버터와 같은 자동차 부품에 대한 수요가 급증하고 있으며, 전 세계에서 자동차 생산 및 판매가 증가하고 있기 때문입니다. 내연기관차(ICE)의 보급으로 엄격한 환경 기준을 충족하기 위한 첨단 배출가스 제어 시스템의 필요성이 증가하고 있습니다. 또한 개인 이동성 및 운송 서비스에 대한 선호도가 높아짐에 따라 시장 수요가 더욱 증가하고 있습니다.

세계에서 엄격한 배출가스 규제가 시장 성장의 주요 요인으로 작용하고 있습니다. 각국 정부는 대기 오염과 싸우고 온실 가스 배출을 억제하기 위해 더욱 엄격한 조치를 시행하고 있습니다. 이러한 지침은 일산화탄소, 질소산화물, 탄화수소와 같은 유해 오염물질의 대폭적인 감축을 요구하고 있습니다. 그 결과, 제조업체들은 점점 더 까다로워지는 성능 기준을 충족하는 혁신적이고 효율적이며 내구성이 뛰어난 촉매 컨버터에 집중하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 112억 달러 |

| 예상 금액 | 203억 달러 |

| CAGR | 6.2% |

재료 유형별로 시장은 백금 기반, 팔라듐 기반, 로듐 기반 컨버터로 분류되며, 2024년에는 백금 기반 촉매 컨버터가 40%의 큰 점유율을 차지하여 2034년까지 70억 달러를 창출할 것으로 예상됩니다. 백금의 뛰어난 촉매 특성으로 인해 백금은 효과적인 배기가스 규제 시스템에 필수적인 요소로 작용하여 엄격한 규제 요건을 충족시킬 수 있습니다. 배기가스 처리에서 백금의 고성능과 환경 보호에 대한 관심이 높아지면서 주요 시장에서 백금의 채택이 증가하고 있습니다.

차종별로는 승용차가 2024년 시장의 74%를 차지하며 압도적인 점유율을 차지하고 있습니다. 저연비, 친환경 자동차에 대한 소비자 수요 증가가 이 부문 성장의 주요 요인으로 작용하고 있습니다. 배출가스 및 지속가능성에 대한 인식이 높아짐에 따라 자동차 제조업체들은 저공해 기술을 개발하여 승용차용 촉매 컨버터의 청정화 및 효율화를 추진하고 있습니다.

미국의 자동차용 삼원촉매 컨버터 시장은 2024년에 80%라는 경이로운 점유율을 획득했습니다. 자동차 배기가스 감축에 중점을 둔 규제는 제조업체들이 최첨단 촉매 기술을 채택하도록 유도하고 있습니다. 소재, 기판 설계, 내열 부품의 혁신은 컨버터의 효율과 내구성을 향상시켜 진화하는 환경 기준을 충족할 수 있도록 돕고 있습니다. 청정 기술에 대한 연방 정부의 인센티브와 투자는 이 지역의 성장을 더욱 가속화하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 어프로치

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도 산출

- 시장 추정의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 스코프와 정의

제2장 개요

제3장 산업 인사이트

- 에코시스템 분석

- 원료 공급업체

- 부품 공급업체

- 제조업체

- 유통 채널

- 최종사용자

- 공급업체 상황

- 이익률 분석

- 기술 혁신 상황

- 특허 분석

- 주요 뉴스 & 구상

- 규제 상황

- 비용 분석

- 영향요인

- 촉진요인

- 연구개발과 신제품 개발에 대한 급속한 투자

- 환경 규제의 증가

- 촉매 컨버터의 기술 진보

- 저연비차에 대한 수요 증가

- 신흥 시장에서의 자동차 수요 증가

- 산업의 잠재적 리스크·과제

- 높은 제조 비용

- 규제상 허들과 컴플라이언스 문제

- 촉진요인

- 성장 가능성 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정·예측 : 재료별, 2021-2034년

- 주요 동향

- 플래티넘 기반

- 팔라듐 기반

- 로듐 기반

제6장 시장 추정·예측 : 차량별, 2021-2034년

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV차

- 상용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

제7장 시장 추정·예측 : 추진력별, 2021-2034년

- 주요 동향

- 가솔린

- 디젤

- 기타

제8장 시장 추정·예측 : 유통 채널별, 2021-2034년

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추정·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 뉴질랜드

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트

- 남아프리카공화국

- 사우디아라비아

제10장 기업 개요

- BASF SE

- Benteler

- BorgWarner

- Bosal

- Calsonic

- Corning

- Delphi

- Denso

- Eberspacher

- Faurecia

- Haldex

- Johnson Matthey

- Magna

- Marelli

- Sango

- Tenneco

- Umicore

- Valeo

- Walker Exhaust Systems

- Yutaka

The Global Automotive Three-Way Catalytic Converter Market, valued at USD 11.2 billion in 2024, is set to expand at a robust CAGR of 6.2% from 2025 to 2034. This growth is fueled by increasing vehicle production and sales worldwide as demand for automotive components such as catalytic converters continues to soar. The widespread use of internal combustion engine (ICE) vehicles has intensified the need for advanced emission control systems to meet stringent environmental standards. Moreover, the rising preference for personal mobility and transportation services is further propelling market demand.

Stringent emissions regulations globally are a major driver behind market growth. Governments are implementing tougher policies to combat air pollution and curb greenhouse gas emissions. These mandates require significant reductions in harmful pollutants like carbon monoxide, nitrogen oxides, and hydrocarbons. As a result, manufacturers are focusing on innovative, efficient, and durable catalytic converters that comply with increasingly rigorous performance standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.2 Billion |

| Forecast Value | $20.3 Billion |

| CAGR | 6.2% |

By material type, the market is categorized into platinum-based, palladium-based, and rhodium-based converters. In 2024, platinum-based catalytic converters held a significant 40% share, with projections to generate USD 7 billion by 2034. The exceptional catalytic properties of platinum make it integral to effective emission control systems, enabling compliance with stringent regulatory requirements. Platinum's high-performance capabilities in treating exhaust gases and the growing focus on environmental sustainability are driving its adoption in key markets.

In terms of vehicle type, passenger vehicles dominated the market in 2024 with a commanding 74% share. Increasing consumer demand for fuel-efficient and environmentally friendly vehicles is a key factor in the segment growth. Rising awareness of emissions and sustainability is encouraging automakers to develop low-emission technologies, leading to cleaner and more efficient catalytic converters for passenger vehicles.

The U.S. market for automotive three-way catalytic converters captured an impressive 80% share in 2024. Regulatory mandates focused on reducing vehicle emissions are spurring manufacturers to adopt cutting-edge catalyst technologies. Innovations in materials, substrate designs, and heat-resistant components are enhancing the efficiency and durability of converters, ensuring compliance with evolving environmental standards. Federal incentives and investments in clean technologies are further accelerating growth in the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Distribution channel

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Cost analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rapid investment in R&D and new product development

- 3.9.1.2 Increasing environmental regulations

- 3.9.1.3 Technological advancements in catalytic converters

- 3.9.1.4 Rising demand for fuel-efficient vehicles

- 3.9.1.5 Growing vehicle demand in emerging markets

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High manufacturing costs

- 3.9.2.2 Regulatory hurdles and compliance issues

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Platinum-based

- 5.3 Palladium-based

- 5.4 Rhodium-based

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCVs)

- 6.3.2 Heavy Commercial Vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 ANZ

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Benteler

- 10.3 BorgWarner

- 10.4 Bosal

- 10.5 Calsonic

- 10.6 Corning

- 10.7 Delphi

- 10.8 Denso

- 10.9 Eberspächer

- 10.10 Faurecia

- 10.11 Haldex

- 10.12 Johnson Matthey

- 10.13 Magna

- 10.14 Marelli

- 10.15 Sango

- 10.16 Tenneco

- 10.17 Umicore

- 10.18 Valeo

- 10.19 Walker Exhaust Systems

- 10.20 Yutaka

(주말 및 공휴일 제외)