|

시장보고서

상품코드

1665414

석유 및 가스용 검사 드론 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Inspection Drone in Oil and Gas Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

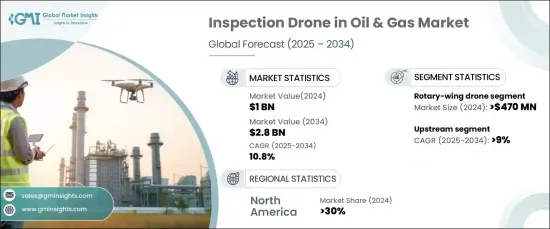

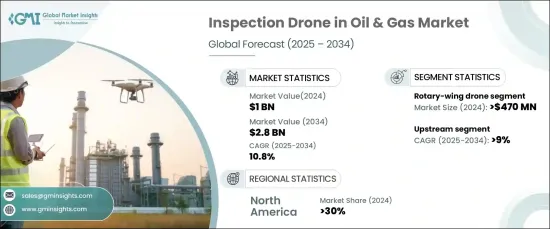

세계의 석유 및 가스용 검사 드론 시장은 2024년에 10억 달러로 평가되며, 2025-2034년에 CAGR 10.8%로 성장할 것으로 예측됩니다. 이러한 성장에는 효율적인 감시 솔루션에 대한 수요 증가와 드론 기술의 급속한 발전이 기여하고 있습니다. 기업은 운영 개선, 위험 감소, 안전성 향상을 위해 혁신적인 검사 시스템 개발에 우선순위를 두고 있습니다. 일상적인 점검, 인프라 평가, 업무 모니터링을 위한 드론의 사용이 증가함에 따라 이 분야의 전통적인 검사 업무가 크게 변화하고 있습니다. 안전 및 환경 규정 준수에 대한 규제 요건이 강화되면서 기존 방식에 대한 보다 신속하고 신뢰할 수 있는 대안을 제공하는 드론 기술의 채택을 촉진하고 있습니다. 또한 AI와 머신러닝을 드론 시스템에 통합함으로써 데이터 분석에 혁명을 일으켜 실시간 인사이트와 간소화된 의사결정 과정을 가능하게 하고 있습니다. 자동화와 업무 효율성에 대한 강조는 계속해서 시장의 궤도를 형성하고 있습니다.

시장은 드론의 유형에 따라 회전익 드론, 고정익 드론, 하이브리드 드론으로 구분됩니다. 회전익 드론은 2024년 상당한 시장 점유율을 차지하며 금액에서 4억 7,000만 달러를 넘었습니다. 이 드론은 제한된 공간에서 호버링 및 조종할 수 있는 능력으로 인해 널리 선호되고 있으며, 파이프라인 및 해양 플랫폼과 같은 고정 자산 검사에 이상적입니다. 이 기술을 사용하면 기존 검사 방법과 관련된 시간과 비용을 줄이면서 안전성과 효율성을 향상시킬 수 있습니다. 기업이 AI 지원 기술을 점점 더 많이 통합함에 따라 실시간 데이터에 기반한 향상된 의사결정 능력을 제공하는 회전익 드론에 대한 수요는 더욱 증가할 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 10억 달러 |

| 예상 금액 | 28억 달러 |

| CAGR | 10.8% |

시장은 또한 사업 유형에 따라 업스트림, 미드스트림, 다운스트림 부문으로 분류됩니다. 업스트림 부문은 2025-2034년 연평균 9% 이상의 견고한 성장이 예상됩니다. 이러한 성장은 탐사 현장, 시추 작업, 특히 외딴 곳이나 어려운 장소에서 탐사 현장, 시추 작업, 파이프라인의 고도화된 모니터링에 대한 요구가 증가함에 따른 것입니다. 드론은 안전성을 높이고, 검사 시간을 최소화하며, 운영 비용을 최적화함으로써 업스트림 작업에 필수적인 툴이 되고 있습니다. 탐사 활동에 대한 투자 증가와 지속가능성에 대한 관심은 이 부문에서 검사 드론에 대한 수요를 더욱 증폭시키고 있습니다.

북미는 2024년 세계 시장을 주도하며 매출 점유율의 30% 이상을 차지했습니다. 특히 미국은 업무 효율성과 엄격한 안전 규정 준수를 중요시하는 미국 시장의 성장세가 두드러지며, AI 및 머신러닝과 같은 첨단 기술을 드론 시스템에 통합하여 실시간 데이터 분석을 통해 기업이 프로세스를 간소화하고, 잠재적인 문제를 신속하게 파악하며, 다운타임을 줄일 수 있도록 돕고 있습니다. 다운타임을 줄일 수 있도록 돕고 있습니다. 혁신과 효율성을 중시하는 이 지역의 태도는 계속해서 시장 성장을 가속하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 어프로치

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도 산출

- 시장 추산의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 범위와 정의

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 공급업체 상황

- 부품 제조업체

- 제조업체

- 유통업체

- 최종 용도

- 이익률 분석

- 기술과 혁신 전망

- 특허 분석

- 규제 상황

- 사용 사례

- 사용 사례 1

- 이점

- 투자수익률

- 사용 사례 2

- 이점

- 투자수익률

- 사용 사례 1

- 사례 연구

- 사례 연구 1

- 소비자명

- 과제

- 해결책

- 영향

- 사례 연구 2

- 소비자명

- 과제

- 해결책

- 영향

- 사례 연구 1

- 영향요인

- 촉진요인

- 실시간 모니터링에 대한 수요 증가

- 드론의 기술적 진보

- 자산관리 솔루션에 대한 수요 증가

- 원격 검사에서 안전 프로토콜의 강화

- 업계의 잠재적 리스크 & 과제

- 데이터 통합과 분석의 과제

- 첨단드론 시스템의 도입에 수반하는 고비용

- 촉진요인

- 성장 가능성 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추산·예측 : 드론별, 2021-2034년

- 주요 동향

- 고정익 드론

- 회전익 드론

- 하이브리드 드론

제6장 시장 추산·예측 : 페이로드별, 2021-2034년

- 주요 동향

- 카메라

- LiDAR

- 가스 탐지기

- 기타

제7장 시장 추산·예측 : 동작별, 2021-2034년

- 주요 동향

- 업스트림

- 미드스트림

- 다운스트림

제8장 시장 추산·예측 : 용도별, 2021-2034년

- 주요 동향

- 파이프라인 검사

- 플레어 스택 검사

- 탱크 검사

- 환경 모니터링

- 갱정검사

- 기타

제9장 시장 추산·예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 국영 석유회사(NOC)

- 독립계 석유회사(IOC)

제10장 시장 추산·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카공화국

- 사우디아라비아

제11장 기업 개요

- 3D Robotics

- Airobotics

- Autel Robotics

- Cyberhawk

- DJI Enterprise

- DroneBase

- DroneDeploy

- FLIR Systems

- Flyability

- GRIFF Aviation

- IdeaForge

- InspecTech Aero Services

- Kespry

- Percepto

- PrecisionHawk

- Quantum Systems

- senseFly

- Sky-Futures(ICR Group)

- Terra Drone

- Vantage Robotics

The Global Inspection Drone In Oil And Gas Market was valued at USD 1 billion in 2024 and is projected to grow at a CAGR of 10.8% from 2025 to 2034. This growth is fueled by the rising demand for efficient monitoring solutions and the rapid advancements in drone technology. Companies are prioritizing the development of innovative inspection systems to improve operations, reduce risks, and enhance safety. The increasing use of drones to conduct routine checks, assess infrastructure, and monitor operations has significantly transformed traditional inspection practices in the sector. Stricter regulatory requirements for safety and environmental compliance are also driving the adoption of drone technologies, which offer a faster and more reliable alternative to conventional methods. Additionally, incorporating AI and machine learning into drone systems is revolutionizing data analysis, enabling real-time insights and streamlined decision-making processes. The focus on automation and operational efficiency continues to shape the market's trajectory.

The market is segmented by drone type into rotary-wing, fixed-wing, and hybrid drones. Rotary-wing drones held a substantial market share in 2024, exceeding USD 470 million in value. These drones are widely preferred due to their ability to hover and maneuver in confined spaces, making them ideal for inspecting stationary assets like pipelines and offshore platforms. Their use enhances safety and efficiency while reducing the time and cost associated with traditional inspection methods. As companies increasingly integrate AI-enabled technologies, the demand for rotary-wing drones is expected to grow further, offering improved decision-making capabilities based on real-time data.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 10.8% |

The market is also categorized by operation type into upstream, midstream, and downstream segments. The upstream segment is forecasted to witness a robust CAGR of over 9% between 2025 and 2034. This growth is attributed to the rising need for advanced monitoring of exploration sites, drilling operations, and pipelines, especially in remote and challenging locations. Drones are becoming an indispensable tool for upstream operations by enhancing safety, minimizing inspection times, and optimizing operational costs. Increased investments in exploration activities and a focus on sustainability further amplify the demand for inspection drones in this segment.

North America led the global market in 2024, capturing over 30% of the revenue share. The United States, in particular, has seen significant growth due to its emphasis on operational efficiency and compliance with stringent safety regulations. The integration of advanced technologies like AI and machine learning into drone systems is enabling real-time data analysis, helping companies streamline processes, identify potential issues quickly, and reduce downtime. The region's strong focus on innovation and efficiency continues to bolster market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Manufacturer

- 3.2.3 Distributors

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Used cases

- 3.7.1 Used case 1

- 3.7.1.1 Benefits

- 3.7.1.2 ROI

- 3.7.2 Used case 2

- 3.7.2.1 Benefits

- 3.7.2.2 ROI

- 3.7.1 Used case 1

- 3.8 Case study

- 3.8.1 Case study 1

- 3.8.1.1 Consumer name

- 3.8.1.2 Challenge

- 3.8.1.3 Solution

- 3.8.1.4 Impact

- 3.8.2 Case study 2

- 3.8.2.1 Consumer name

- 3.8.2.2 Challenge

- 3.8.2.3 Solution

- 3.8.2.4 Impact

- 3.8.1 Case study 1

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for real-time monitoring

- 3.9.1.2 Technological advancements in drone capabilities

- 3.9.1.3 Rising demand for asset management solutions

- 3.9.1.4 Enhanced safety protocols for remote inspections

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Challenges in data integration and analysis

- 3.9.2.2 High costs associated with implementing advanced drone systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Drone, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Fixed-wing drone

- 5.3 Rotary-wing drone

- 5.4 Hybrid drone

Chapter 6 Market Estimates & Forecast, By Payload, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Cameras

- 6.3 LiDAR

- 6.4 Gas detectors

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Operation, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Upstream

- 7.3 Midstream

- 7.4 Downstream

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Pipeline inspection

- 8.3 Flare stack inspection

- 8.4 Tank inspection

- 8.5 Environmental monitoring

- 8.6 Well site inspection

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 National Oil Companies (NOCs)

- 9.3 Independent Oil Companies (IOCs)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 3D Robotics

- 11.2 Airobotics

- 11.3 Autel Robotics

- 11.4 Cyberhawk

- 11.5 DJI Enterprise

- 11.6 DroneBase

- 11.7 DroneDeploy

- 11.8 FLIR Systems

- 11.9 Flyability

- 11.10 GRIFF Aviation

- 11.11 IdeaForge

- 11.12 InspecTech Aero Services

- 11.13 Kespry

- 11.14 Percepto

- 11.15 PrecisionHawk

- 11.16 Quantum Systems

- 11.17 senseFly

- 11.18 Sky-Futures (ICR Group)

- 11.19 Terra Drone

- 11.20 Vantage Robotics