|

시장보고서

상품코드

1666531

HVDC 컨버터 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)HVDC Converter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

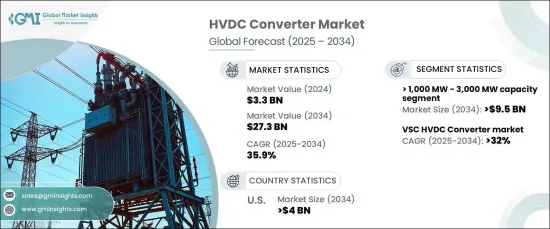

세계의 HVDC 컨버터 시장은 2024년에 33억 달러로 기록되었고, 2025년부터 2034년까지의 CAGR은 35.9%로 예외적인 성장을 이룰 것으로 전망됩니다.

시장 확대의 배경은 특히 세계가 신재생에너지로 전환하는 가운데, 보다 효율적인 송전시스템에 대한 요구가 높아지고 있습니다. HVDC 기술은 광대한 거리를 최소한의 손실로 송전할 수 있는 점에서 두드러지며, 세계의 노후화된 에너지 인프라를 현대화하는 이상적인 솔루션이 되고 있습니다. 풍력발전이나 태양광발전 등 재생가능에너지 통합에 대한 주목이 높아짐에 따라 기존의 송전망에는 신속한 적응이 요구되고 있습니다. 따라서, 송전의 과제를 극복하는 신뢰성 높은 수단을 제공하는 HVDC 컨버터의 채용이 확대되고 있습니다. 신재생에너지 프로젝트에 대한 투자, 국경을 넘어 전력 연결 추진, 송전망 인프라의 지속적인 진보도 시장 성장의 주요 요인이 되고 있습니다.

신재생에너지 통합을 선호하는 국가가 늘어남에 따라 대용량 HVDC 시스템의 필요성은 전례 없이 높아지고 있습니다. 용량이 1,000MW에서 3,000MW인 시스템은 2034년까지 95억 달러를 생산할 것으로 예상됩니다. 이 시스템은 해상 풍력 발전소 및 태양광 발전 설비와 같은 대규모 재생 가능 에너지 프로젝트에 필수적이며 장거리의 효율적인 송전을 보장하고 도시 인구의 에너지 수요에 대응합니다. 또한 국경을 넘은 전력거래를 지원하고 신재생에너지 발전에 의존하는 지역을 연결하는 중요한 역할도 담당하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 33억 달러 |

| 예측 금액 | 273억 달러 |

| CAGR | 35.9% |

특히 전압원 컨버터(VSC) 기술은 2034년까지 연평균 복합 성장률(CAGR)이 32%로 급속한 보급이 전망되고 있습니다. VSC는 매우 다재다능하며 신재생 에너지 통합을 강화하면서 복잡한 송전망의 전력 흐름을 관리하는 데 이상적입니다. 취약한 계통과 고립된 계통에서 효과적으로 작동하고 다단자 연결을 지원하는 VSC의 능력은 해외 및 도시 지역의 에너지 용도 모두에게 매력적인 선택입니다. VSC는 기존의 계통 연계 컨버터(LCC)와는 달리 탁월한 그리드 제어와 유연성을 제공하기 위해 최신 송전 시스템에 가장 적합한 기술로 자리매김하고 있습니다.

미국의 HVDC 컨버터 시장은 2034년까지 40억 달러를 창출할 것으로 예상됩니다. 이 성장의 원동력은 인프라 노후화, 청정 에너지 추진, 장거리 HVDC 변속 프로젝트 수요 증가입니다. 풍력 발전소와 태양광 발전소와 같은 재생 가능 에너지 생산 기지와 대도시 지역을 연결해야 할 필요성은 HVDC 시스템의 중요성 증가를 뒷받침합니다. 청정 에너지를 지원하는 미국 연방 정부의 정책과 재생 가능 에너지의 통합을 촉진하는 규제 프레임 워크는 HVDC 기술에 대한 투자를 가속화하고 있습니다. 그 결과 미국에서는 VSC 기반 HVDC 시스템이 점점 선호되고 있습니다. 이 시스템은 다양한 에너지원을 원활하게 통합할 수 있는 유연성을 제공하며 동시에 발전하는 송전망 수요에도 대응할 수 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 시장 추계·예측 파라미터

- 예측 계산

- 데이터 소스

- 1차

- 2차

- 유료

- 공개

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 전략적 전망

- 혁신과 지속가능성의 전망

제5장 시장 규모와 예측 : 용량별(2021-2034년), 10억 달러

- 주요 동향

- 500MW 미만

- 500 MW 이상-1,000 MW

- 1,000 MW-3,000 MW

- 3,000 MW 이상

제6장 시장 규모와 예측 : 구성별(2021-2034년), 10억 달러

- 주요 동향

- 모노폴라

- 바이폴라

- BTB(Back to back)

- 기타

제7장 시장 규모와 예측 : 컨버터별(2021-2034년), 10억 달러

- 주요 동향

- LCC

- VSC

- 기타

제8장 시장 규모와 예측 : 지역별(2021-2034년), 10억 달러

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 노르웨이

- 아시아태평양

- 중국

- 인도

- 한국

- 호주

- 세계 기타 지역

제9장 기업 프로파일

- ABB

- Bharat Heavy Electricals

- CG Power and Industrial Solutions

- General Electric

- Hitachi

- Hyosung Heavy Industries

- Power Grid Corporation of India

- Rongxin Power

- Siemens Energy

- Toshiba

The Global HVDC Converter Market, valued at USD 3.3 billion in 2024, is poised for exceptional growth, with a CAGR of 35.9% from 2025 to 2034. The market expansion is driven by a growing need for more efficient power transmission systems, especially as the world transitions to renewable energy sources. HVDC technology stands out for its ability to transmit electricity over vast distances with minimal loss, making it an ideal solution for modernizing aging energy infrastructures worldwide. The increasing focus on renewable energy integration, such as wind and solar power, is placing pressure on the existing grids to adapt quickly. As such, HVDC converters, which offer a reliable means of overcoming transmission challenges, are seeing significant adoption. Investment in renewable energy projects, the push for cross-border electricity connections, and ongoing advancements in grid infrastructure are also key factors contributing to the market growth.

As more countries prioritize renewable energy integration, the need for high-capacity HVDC systems has never been more urgent. Systems with capacities ranging from 1,000 MW to 3,000 MW are expected to generate USD 9.5 billion by 2034. These systems are vital for large-scale renewable energy projects, such as offshore wind farms and solar power installations, ensuring efficient power transmission over long distances and addressing the energy demands of urban populations. They also play a crucial role in supporting cross-border electricity trade, connecting regions that rely on renewable energy generation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.3 Billion |

| Forecast Value | $27.3 Billion |

| CAGR | 35.9% |

In particular, the voltage source converter (VSC) technology is anticipated to see a rapid increase in adoption, with a CAGR of 32% through 2034. VSCs are highly versatile and ideal for managing power flow in complex grids while enhancing renewable energy integration. Their ability to operate effectively in weak or isolated grids and support multi-terminal connections makes them an attractive option for both offshore and urban energy applications. Unlike traditional line-commutated converters (LCC), VSCs provide superior grid control and flexibility, positioning them as the technology of choice for modern power transmission systems.

The U.S. HVDC converter market is expected to generate USD 4 billion by 2034. This growth is driven by a combination of aging infrastructure, the push for cleaner energy, and an increased demand for long-distance HVDC transmission projects. The need to connect renewable energy production centers, such as wind and solar farms, with major urban areas underscores the growing relevance of HVDC systems. U.S. federal policies supporting clean energy and regulatory frameworks aimed at facilitating renewable energy integration are accelerating investments in HVDC technology. As a result, the U.S. is seeing an increasing preference for VSC-based HVDC systems, which offer the flexibility to seamlessly integrate diverse energy sources while meeting evolving grid demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 – 2034 (MW, USD Billion)

- 5.1 Key trends

- 5.2 < 500 MW

- 5.3 ≥ 500 MW - 1,000 MW

- 5.4 > 1,000 MW - 3,000 MW

- 5.5 > 3,000 MW

Chapter 6 Market Size and Forecast, By Configuration, 2021 – 2034 (MW, USD Billion)

- 6.1 Key trends

- 6.2 Monopolar

- 6.3 Bipolar

- 6.4 Back to back

- 6.5 Others

Chapter 7 Market Size and Forecast, By Converter, 2021 – 2034 (MW, USD Billion)

- 7.1 Key trends

- 7.2 LCC

- 7.3 VSC

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (MW, USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Norway

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 South Korea

- 8.4.4 Australia

- 8.5 Rest of World

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Bharat Heavy Electricals

- 9.3 CG Power and Industrial Solutions

- 9.4 General Electric

- 9.5 Hitachi

- 9.6 Hyosung Heavy Industries

- 9.7 Power Grid Corporation of India

- 9.8 Rongxin Power

- 9.9 Siemens Energy

- 9.10 Toshiba