|

시장보고서

상품코드

1666710

파이프 단열재 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Pipe Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

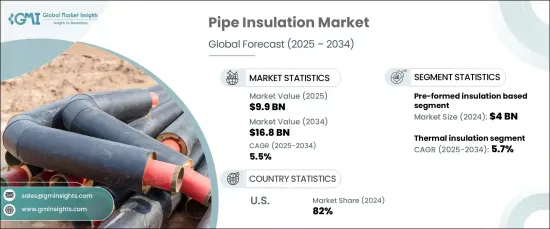

세계의 파이프 단열재 시장은 2024년에 99억 달러에 달하며, 2025-2034년에 CAGR 5.5%로 성장할 것으로 예측됩니다.

이러한 성장은 에너지 효율에 대한 관심 증가, 규제 기준 준수, 지속가능한 건설 방법의 채택 증가가 주요 요인으로 작용하고 있습니다. 파이프 단열재는 냉난방 시스템의 에너지 손실을 효과적으로 최소화하여 주거, 상업 및 산업 환경의 에너지 효율 향상에 기여합니다.

에너지 비용이 계속 상승하고 이산화탄소 배출량을 줄이는 것이 시급한 상황에서 파이프 단열재는 전체 에너지 소비를 줄일 수 있는 실용적인 솔루션으로 주목받고 있습니다. 배관 시스템의 온도를 일정하게 유지하여 냉난방에 필요한 에너지를 절감함으로써 장기적인 비용 절감과 지속가능성의 이점을 제공합니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 99억 달러 |

| 예상 금액 | 168억 달러 |

| CAGR | 5.5% |

제품 유형별로 시장은 성형 전 단열재, 경질 보드 단열재, 블랭킷 단열재, 롤 단열재, 스프레이 폼 단열재, 기타로 구분됩니다. 이 중 성형 전 단열재는 2024년 약 40억 달러의 매출을 창출하는 주요 부문으로 부상했습니다. 이 부문은 사용자 친화적인 설치 과정과 다양한 파이프 치수 및 구성에 대응할 수 있는 능력으로 인해 꾸준히 성장할 것으로 예상됩니다. 유리섬유와 미네랄울과 같은 재료를 사용하여 제조되는 프리폼 단열재는 인건비와 설치 시간을 줄여주기 때문에 모든 분야에서 선호되고 있습니다.

기능별로 시장은 단열, 방음, 방화, 기타로 분류됩니다. 단열재는 2024년 시장 점유율의 약 40%를 차지하며, 예측 기간 중 CAGR 5.7%로 성장할 것으로 예상됩니다. 단열재의 주요 역할은 파이프 내부의 온도를 일정하게 유지하여 에너지 낭비를 최소화하고 산업 공정의 성능을 최적화하는 것입니다. 이 기능은 효율성과 운영 비용 절감이 우선시되는 제조 및 에너지 생산과 같은 분야에서 특히 중요합니다.

지역별로는 미국이 북미 파이프 단열재 시장의 약 82%라는 큰 비중을 차지하고 있습니다. 엄격한 건축 법규와 에너지 효율 의무화로 인해 고급 단열 솔루션에 대한 수요가 증가하고 있습니다. 규제 프레임워크는 HVAC 및 배관 시스템의 에너지 손실을 줄이는 것을 목표로 하고 있으며, 고성능 단열재 채택을 촉진하고 있습니다.

파이프 단열재 시장은 에너지 절약에 대한 관심이 높아지고 효율적이고 지속가능한 인프라 솔루션에 대한 필요성이 증가함에 따라 강력한 성장이 예상됩니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차

- 2차

- 유료 소스

- 공적 소스

제2장 개요

제3장 업계 인사이트

- 업계 에코시스템 분석

- 밸류체인에 영향을 미치는 요인

- 이익률 분석

- 변혁

- 향후 전망

- 제조업체

- 유통업체

- 공급업체 상황

- 이익률 분석

- 주요 뉴스와 구상

- 규제 상황

- 영향요인

- 성장 촉진요인

- 건설 활동의 증가

- 제품 혁신의 진전

- 업계의 잠재적 리스크·과제

- 시장의 포화와 치열한 경쟁

- 지속가능성에 대한 우려

- 성장 촉진요인

- 성장 가능성 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추산·예측 : 제품 유형별, 2021-2035년

- 주요 동향

- 예비 성형 단열재

- 경질 보드 단열재

- 블랭킷 단열재

- 롤 단열재

- 스프레이 폼 단열재

- 기타(루스 필 단열재 등)

제6장 시장 추산·예측 : 재료 유형별, 2021-2035년

- 주요 동향

- 유리섬유

- 미네랄울

- 폴리우레탄

- 폴리에틸렌

- 엘라스토머 폼

- 고무

- 기타(규산칼슘 등)

제7장 시장 추산·예측 : 기능별, 2021-2035년

- 주요 동향

- 단열

- 방음

- 방화

- 기타(결로방지 등)

제8장 시장 추산·예측 : 최종 용도별, 2021-2035년

- 주요 동향

- 주택용

- 상업용

- 산업용

- 석유 및 가스

- 화학

- 에너지·전력

- 해양

- 기타(제약 등)

제9장 시장 추산·예측 : 유통 채널별, 2021-2035년

- 주요 동향

- 직접

- 간접

제10장 시장 추산·예측 : 지역별, 2021-2035년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- UAE

- 사우디아라비아

- 남아프리카공화국

제11장 기업 개요

- 3M

- Alfa Laval

- Armacell International

- BASF

- Covestro

- Huntsman Corporation

- Insulation Technologies

- Johns Manville

- Kingspan Group

- Knauf Insulation

- Owens Corning

- Rockwool International

- Saint Gobain

- Shenzhen Lanxuan Industrial

- Thermaflex

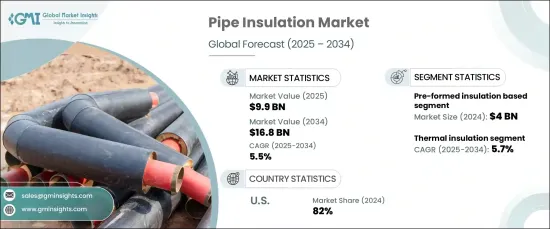

The Global Pipe Insulation Market was valued at USD 9.9 billion in 2024 and is expected to grow at a CAGR of 5.5% from 2025 to 2034. This growth is largely driven by the increasing focus on energy efficiency, compliance with regulatory standards, and the rising adoption of sustainable construction practices. Insulating pipes effectively minimizes energy loss in heating and cooling systems, contributing to improved energy efficiency in residential, commercial, and industrial settings.

As energy costs continue to climb and the urgency to reduce carbon emissions intensifies, pipe insulation is gaining prominence as a practical solution to lower overall energy consumption. It helps maintain consistent temperatures in piping systems, reducing the energy required for heating or cooling, thus offering long-term cost savings and sustainability benefits.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.9 Billion |

| Forecast Value | $16.8 Billion |

| CAGR | 5.5% |

The market is segmented by product type into pre-formed insulation, rigid board insulation, blanket insulation, roll insulation, spray foam insulation, and others. Among these, pre-formed insulation emerged as a leading segment, generating approximately USD 4 billion in revenue in 2024. This segment is projected to grow steadily, owing to its user-friendly installation process and ability to accommodate various pipe dimensions and configurations. Manufactured using materials such as fiberglass and mineral wool, pre-formed insulation reduces labor costs and installation time, making it a preferred choice across sectors.

By function, the market is categorized into thermal insulation, acoustic insulation, fire protection, and others. Thermal insulation accounted for around 40% of the market share in 2024 and is anticipated to grow at a CAGR of 5.7% over the forecast period. Its primary role is to maintain temperature consistency in pipes, thus minimizing energy waste and optimizing performance in industrial processes. This functionality is particularly important in sectors like manufacturing and energy production, where efficiency and operational cost reduction are priorities.

Regionally, the United States dominates the North America pipe insulation market, holding a substantial share of approximately 82%. Stricter building codes and energy-efficiency mandates are fueling demand for advanced insulation solutions. Regulatory frameworks aim to reduce energy loss in HVAC and plumbing systems, boosting the adoption of high-performance insulation materials.

The pipe insulation market is poised for robust growth, driven by the increasing emphasis on energy conservation and the need for efficient and sustainable infrastructure solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing construction activities

- 3.6.1.2 Growing product innovation

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Market saturation and intense competition

- 3.6.2.2 Sustainability concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2035 (USD Million) (Thousand Square Feet)

- 5.1 Key trends

- 5.2 Pre-formed insulation

- 5.3 Rigid board insulation

- 5.4 Blanket insulation

- 5.5 Roll insulation

- 5.6 Spray Foam insulation

- 5.7 Others (loose fill insulation, etc.)

Chapter 6 Market Estimates & Forecast, By Material Type, 2021-2035 (USD Million) (Thousand Square Feet)

- 6.1 Key trends

- 6.2 Fiberglass

- 6.3 Mineral wool

- 6.4 Polyurethane

- 6.5 Polyethylene

- 6.6 Elastomeric foam

- 6.7 Rubber

- 6.8 Others (calcium silicate, etc.)

Chapter 7 Market Estimates & Forecast, By Function, 2021-2035 (USD Million) (Thousand Square Feet)

- 7.1 Key trends

- 7.2 Thermal insulation

- 7.3 Acoustic insulation

- 7.4 Fire protection

- 7.5 Others (condensation control, etc.)

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2035 (USD Million) (Thousand Square Feet)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

- 8.4.1 Oil & gas

- 8.4.2 Chemical

- 8.4.3 Energy & power

- 8.4.4 Marine

- 8.4.5 Others (pharmaceutical, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2035 (USD Million) (Thousand Square Feet)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2035 (USD Million) (Thousand Square Feet)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 3M

- 11.2 Alfa Laval

- 11.3 Armacell International

- 11.4 BASF

- 11.5 Covestro

- 11.6 Huntsman Corporation

- 11.7 Insulation Technologies

- 11.8 Johns Manville

- 11.9 Kingspan Group

- 11.10 Knauf Insulation

- 11.11 Owens Corning

- 11.12 Rockwool International

- 11.13 Saint Gobain

- 11.14 Shenzhen Lanxuan Industrial

- 11.15 Thermaflex