|

시장보고서

상품코드

1667013

배리어재 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Barrier Material Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

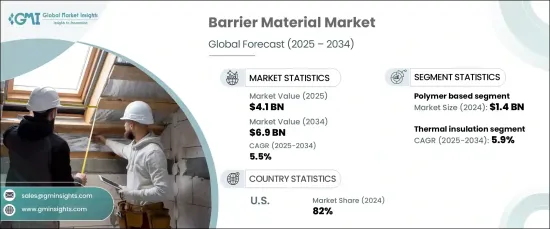

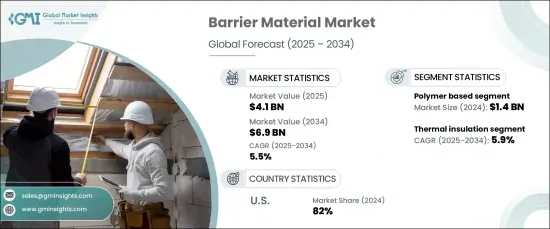

세계 배리어재 시장은 2024년 41억 달러로 평가되며 2025년부터 2034년까지 5.5%의 CAGR로 성장할 것으로 예상됩니다.

이러한 성장세는 건설, 자동차, 제약, 식품 포장 등 다양한 산업에서 안전과 보안을 강화하는 첨단 솔루션에 대한 수요가 급증하고 있는 데 따른 것입니다. 이들 산업이 외부 위협으로부터 제품 및 구조물을 보호하는 것을 최우선 과제로 삼으면서 배리어재에 대한 신뢰가 계속 높아지고 있습니다.

습기, 열 변동, 소리의 침입을 방지하는 데 필수적인 배리어재는 다양한 용도의 내구성과 효율성을 향상시키는 데 필수적입니다. 지속가능성에 대한 규제 감시가 강화됨에 따라 기업들은 최신 산업 표준을 충족하기 위해 친환경적이고 재활용 가능한 고성능 소재로 전환하고 있습니다. 또한, 기술 발전과 연구 개발 노력은 혁신을 촉진하고 특정 산업 요구에 맞는 최첨단 솔루션을 제공하여 궁극적으로 시장 잠재력을 확장하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 41억 달러 |

| 예상 금액 | 69억 달러 |

| CAGR | 5.5% |

재료 유형별로 시장은 금속 기반, 광물 기반, 폴리머 기반, 기타 카테고리로 분류됩니다. 폴리머 기반 부문은 2024년 14억 달러로 평가되며 2035년까지 연평균 5.6%의 성장률을 기록할 것으로 예상됩니다. 물의 침투를 방지하는 탁월한 능력으로 알려진 폴리머 기반 재료는 지붕, 지하실, 기초 시스템에 적합한 선택이며, 수해에 대한 우려가 높아짐에 따라 이에 대한 대응책으로 사용되고 있습니다. 이러한 재료는 환경적 요인으로부터 확실하게 보호할 수 있기 때문에 신축 및 개보수 프로젝트에서 필수적인 요소로 자리 잡고 있습니다. 한편, 금속계 재료는 해안 지역이나 오염이 심한 산업 지역과 같이 극한의 기상 조건에 노출된 환경에서는 구조적 내력에 필수적인 요소로 작용하고 있습니다.

시장을 기능별로 분류하면 방습, 단열, 방음, 방음, 방화, 기타 분야가 있습니다. 단열재는 2024년 41%의 시장 점유율을 차지했으며, 예측 기간 동안 연평균 5.9%의 CAGR로 성장할 것으로 예상됩니다. 에너지 비용 상승과 엄격한 에너지 효율 규제로 인해 고급 단열재에 대한 수요가 증가하고 있습니다. 이러한 소재는 특히 냉난방 시스템에서 열 손실을 줄이고 에너지 소비를 최적화하는 데 도움이 되며, 이는 지속가능성과 비용 효율적인 에너지 솔루션에 대한 전 세계적인 움직임과 일치합니다.

미국에서는 2024년 장벽재 시장이 지역별로 82%의 점유율을 차지했습니다. 이러한 우위는 플라스틱 폐기물을 줄이고 지속가능한 관행을 장려하기 위한 강력한 규제 프레임워크에 기인합니다. 기업들은 환경에 민감한 소비자들을 위해 재활용 가능한 다층 필름, 바이오폴리머 기반 플라스틱, 퇴비화 가능한 포장재 등 생분해성 및 저탄소발자국 소재에 대한 선호도가 높아지고 있습니다. 이러한 변화는 환경 보호에 대한 약속을 반영하는 것이며, 지속가능성 목표에 부합하는 업계의 지속적인 성장을 가능케 하는 것입니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 데이터

- 유료 정보 출처

- 공개 정보 출처

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 미치는 요인

- 이익률 분석

- 파괴

- 향후 전망

- 제조업체

- 유통업체

- 공급업체 상황

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 건설 활동 증가

- 제품 혁신 진전

- 업계의 잠재적 리스크와 과제

- 시장 포화와 치열한 경쟁

- 지속가능성에 대한 우려

- 성장 촉진요인

- 성장 가능성 분석

- Porters 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정과 예측 : 소재별, 2021-2035년

- 주요 동향

- 폴리머 기반

- 폴리염화비닐리덴(PVDC)

- 에틸렌 비닐 알코올(EVOH)

- 폴리에틸렌 나프탈레이트(PEN)

- 기타

- 금속 기반

- 광물 기반

- 지오신세틱 클레이 라이너(GCL)

- 석고

- 기타(미네랄 우드 등)

- 기타(섬유 소재 기반 등)

제6장 시장 추정과 예측 : 기능별, 2021-2035년

- 주요 동향

- 방습

- 단열

- 방음

- 방화

- 기타(방사선 배리어, 실링재 등)

제7장 시장 추정과 예측 : 배리어 유형별, 2021-2035년

- 주요 동향

- 일시적 배리어

- 항구 배리어

제8장 시장 추정과 예측 : 건설 유형별, 2021-2035년

- 주요 동향

- 신축

- 레트로피트

제9장 시장 추정과 예측 : 최종 용도별, 2021-2035년

- 주요 동향

- 주택

- 상업

- 산업·창고

- 인프라 시설

제10장 시장 추정과 예측 : 유통 채널별, 2021-2035년

- 주요 동향

- 직접

- 간접

제11장 시장 추정과 예측 : 지역별, 2021-2035년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- UAE

- 사우디아라비아

- 남아프리카공화국

제12장 기업 개요

- 3M

- BASF

- Dow

- Geosynthetics

- Gundle/SLT Environmental

- H.B. Fuller

- Honeywell International

- Owosso

- Pall Corporation

- Renolit

- Saint-Gobain

- Sika

- Solvay

- TenCate Geosynthetics

- Trelleborg

The Global Barrier Material Market was valued at USD 4.1 billion in 2024 and is poised to grow at a CAGR of 5.5% between 2025 and 2034. This upward trajectory is fueled by surging demand for advanced solutions that enhance safety and security across diverse industries such as construction, automotive, pharmaceuticals, and food packaging. As these sectors prioritize protecting their products and structures from external threats, the reliance on barrier materials continues to rise.

Barrier materials, essential for preventing moisture intrusion, thermal fluctuations, and sound penetration, are critical to improving the durability and efficiency of various applications. With increasing regulatory scrutiny on sustainability, businesses are transitioning toward eco-friendly, recyclable, and high-performance materials to meet modern industry standards. Moreover, technological advancements and R&D efforts are driving innovation, offering cutting-edge solutions tailored to meet specific industry needs, ultimately expanding the market's potential.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 5.5% |

By material type, the market is segmented into metal-based, mineral-based, polymer-based, and other categories. The polymer-based segment, valued at USD 1.4 billion in 2024, is expected to grow at a CAGR of 5.6% through 2035. Renowned for their superior ability to prevent water infiltration, polymer-based materials are the go-to choice for roofing, basement, and foundation systems, addressing the growing concerns about water damage. These materials have become indispensable for both new construction and renovation projects, offering reliable protection against environmental factors. Meanwhile, metal-based materials are vital in environments exposed to extreme weather conditions, such as coastal regions or industrial zones prone to high pollution, making them an essential component for structural resilience.

When categorized by function, the market includes moisture prevention, thermal insulation, soundproofing, fire protection, and other segments. Thermal insulation commanded a significant 41% market share in 2024 and is projected to grow at a 5.9% CAGR during the forecast period. Rising energy costs and stringent energy efficiency regulations have heightened the demand for advanced thermal barriers. These materials are instrumental in reducing heat loss and optimizing energy consumption, particularly in heating and cooling systems, aligning with the global focus on sustainability and cost-effective energy solutions.

In the United States, the barrier material market accounted for 82% of the regional share in 2024. This dominance is driven by robust regulatory frameworks aimed at reducing plastic waste and encouraging sustainable practices. Businesses are increasingly adopting biodegradable, low-carbon-footprint materials, including recyclable multi-layer films, biopolymer-based plastics, and compostable packaging, to cater to eco-conscious consumers. This shift reflects a commitment to environmental stewardship and positions the industry for continued growth in alignment with sustainability goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing construction activities

- 3.6.1.2 Growing product innovation

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Market saturation and intense competition

- 3.6.2.2 Sustainability concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polymer based

- 5.2.1 Polyvinylidene chloride (PVDC)

- 5.2.2 Ethylene vinyl alcohol (EVOH)

- 5.2.3 Polyethylene naphthalate (PEN)

- 5.3 Others

- 5.4 Metal based

- 5.5 Mineral based

- 5.5.1 Geosynthetic clay liners (GCLs)

- 5.5.2 Gypsum

- 5.6 Others (mineral wood, etc.)

- 5.7 Others (fibrous material based, etc.)

Chapter 6 Market Estimates & Forecast, By Function, 2021-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Moisture prevention

- 6.3 Thermal insulation

- 6.4 Sound proofing

- 6.5 Fire protection

- 6.6 Others (radiation barrier, sealant, etc.)

Chapter 7 Market Estimates & Forecast, By Type of Barrier, 2021-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Temporary barriers

- 7.3 Permanent barriers

Chapter 8 Market Estimates & Forecast, By Type of Construction, 2021-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 New construction

- 8.3 Retrofit

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial and warehousing

- 9.5 Infrastructure facility

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2021-2035 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 3M

- 12.2 BASF

- 12.3 Dow

- 12.4 Geosynthetics

- 12.5 Gundle/SLT Environmental

- 12.6 H.B. Fuller

- 12.7 Honeywell International

- 12.8 Owosso

- 12.9 Pall Corporation

- 12.10 Renolit

- 12.11 Saint-Gobain

- 12.12 Sika

- 12.13 Solvay

- 12.14 TenCate Geosynthetics

- 12.15 Trelleborg