|

시장보고서

상품코드

1667110

제로 에미션 항공기 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Zero Emission Aircraft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

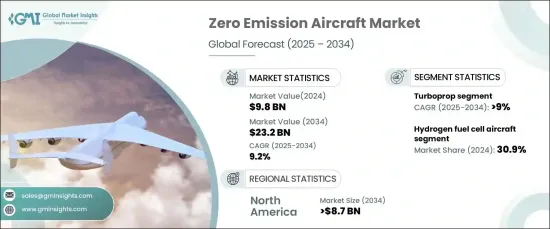

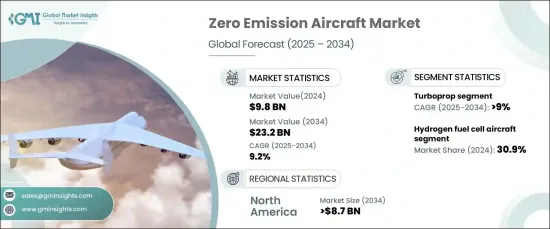

세계 제로 에미션 항공기 시장은 2024년 98억 달러에 이르렀으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 9.2%로 성장할 것으로 예상됩니다.

환경에 대한 우려가 높아지고 지속 가능한 여행 옵션에 대한 소비자 수요가 급증하는 가운데, 환경 친화적인 항공 솔루션에 대한 요구는 전례 없이 높아지고 있습니다. 여행자들이 보다 친환경적인 선택을 추구하는 경향이 커지고 있는 가운데, 항공사는 지속가능성 목표에 부합하기 때문에 제로 방출 항공기를 선호합니다. 기업은 또한 사회적 책임 목표를 달성하기 위해 이러한 환경을 배려한 솔루션을 채택하는 한편 투자자는 환경, 사회, 거버넌스(ESG) 기준의 준수를 추진하여 보다 깨끗한 기술의 채용을 가속화하고 있습니다.

시장은 항공기 유형별로 배터리 전기 항공기, 수소 연료전지 항공기, 하이브리드 전기 항공기, 태양전지 항공기로 구분됩니다. 2024년에는 수소연료전지 분야가 30.9%의 점유율로 시장을 선도했습니다. 수소 연료전지 항공기는 연료전지를 이용하여 발전하여 기존의 제트 연료를 대체하는 지속 가능한 대체 연료를 제공합니다. 이 기술은 특히 단거리에서 중거리 비행에 적합하며 운항 중 배출가스가 전혀 발생하지 않습니다. 연료전지 시스템의 지속적인 혁신으로 효율성이 향상되고 수소는 항공의 이산화탄소 배출량을 크게 줄이는 중요한 솔루션이 되었습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025년-2034년 |

| 시작금액 | 98억 달러 |

| 예측 금액 | 232억 달러 |

| CAGR | 9.2% |

항공기 유형별로 시장은 터보프롭, 터보 팬, 혼합 날개 기계(BWB), 완전 전기 개념으로 나뉩니다. 이 중 터보프롭 분야는 2025년부터 2034년의 CAGR이 9%를 나타낼 전망입니다. 연료 효율과 짧은 활주로에의 적합성으로 알려진 터보프롭 기계는 전기 추진과 지속 가능한 연료를 도입하여 혁명을 일으키고 있습니다. 이러한 기술의 진보에 의해 터보프롭기는 지역 노선이나 단거리 노선에 이상적인 것이 되고 있습니다. 하이브리드 전기 기술과 배터리 기술의 통합은 항공기가 이러한 용도에 필요한 성능을 유지할 수 있도록 하면서 배출량을 더욱 줄여줍니다.

북미 제로 에미션 항공기 시장은 항공 관련 이산화탄소 배출량 감소를 목표로 하는 많은 투자와 정부의 이니셔티브에 힘입어 2034년까지 87억 달러를 창출할 것으로 예상됩니다. 이 지역은 전기 및 수소를 동력원으로 하는 항공기 개발을 주도하고 있으며 기존 제조업체와 혁신적인 신흥 기업 모두가 크게 기여하고 있습니다. 이러한 발전은 지역 항공 여행의 지속가능성을 지원할뿐만 아니라 업계 전반에 걸쳐 깨끗한 기술을 널리 채택하는 데에도 기여합니다. 이 분야의 북미 리더십은 세계 항공 기준을 형성하고 세계 배출 감소 목표를 달성하는데 중요한 역할을 합니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차

- 2차

- 유료소스

- 공적소스

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 변혁

- 장래의 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 깨끗한 항공기술에 대한 정부지원 증가

- 지속 가능하고 환경 친화적인 항공 솔루션에 대한 수요 증가

- 배터리와 연료전지 시스템의 기술적 진보

- 항공사에 대한 이산화탄소 배출량 감축 압력 증가

- 그린항공 인프라와 충전 네트워크 확대

- 업계의 잠재적 리스크 및 과제

- 제로에미션 항공기의 개발 및 제조 비용의 높이

- 현재의 배터리 기술에서의 항속 거리와 에너지 밀도의 한계

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 항공기 유형별, 2021년-2034년

- 주요 동향

- 배터리 전기 항공기

- 수소 연료전지 항공기

- 하이브리드 전기 항공기

- 솔라 전기 항공기

제6장 시장 추정 및 예측 : 유형별, 2021년-2034년

- 주요 동향

- 터보프롭

- 터보 팬 시스템

- 혼합익기(BWB)

- 완전 전동 컨셉

제7장 시장 추정 및 예측 : 용량별, 2021년-2034년

- 주요 동향

- 9-30

- 31-60

- 61-100

- 101-150

- 150 이상

제8장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 상업

- 군사

- 일반

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Ampaire Inc.

- Aurora Flight Sciences(The Boeing Company)

- BETA Technologies, Inc.

- Bye Aerospace

- Equator Aircraft AS

- Evektor, spol. s ro

- Eviation

- Heart Aerospace

- Joby Aero, Inc.

- Lilium GmbH

- PIPISTREL doo

- Rolls-Royce plc

- Wright Electric

- ZeroAvia, Inc.

The Global Zero Emission Aircraft Market reached USD 9.8 billion in 2024 and is projected to grow at a robust CAGR of 9.2% from 2025 to 2034. With rising environmental concerns and a surge in consumer demand for sustainable travel options, the need for eco-friendly aviation solutions is higher than ever. As travelers increasingly seek greener alternatives, airlines prioritize zero-emission aircraft to align with sustainability goals. Corporations are also embracing these eco-conscious solutions to meet their social responsibility targets, while investors are pushing for adherence to environmental, social, and governance (ESG) standards, accelerating the adoption of cleaner technologies.

The market is segmented by aircraft type into battery electric, hydrogen fuel cell, hybrid electric, and solar electric aircraft. In 2024, the hydrogen fuel cell segment leads the market with a 30.9% share. Hydrogen-powered aircraft utilize fuel cells to generate electricity, providing a sustainable alternative to traditional jet fuels. This technology is especially suitable for short- to medium-haul flights, producing zero emissions during operation. Ongoing innovations in fuel cell systems are improving their efficiency, establishing hydrogen as a key solution to drastically reduce carbon footprints in aviation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.8 billion |

| Forecast Value | $23.2 billion |

| CAGR | 9.2% |

By aircraft type, the market is also divided into turboprop, turbofan, blended-wing body (BWB), and fully electric concepts. Among these, the turboprop segment is the fastest-growing, with a CAGR of 9% during 2025-2034. Known for its fuel efficiency and compatibility with shorter runways, the turboprop aircraft is being revolutionized through the incorporation of electric propulsion and sustainable fuels. These technological advancements are making turboprops ideal for regional and short-haul routes. The integration of hybrid-electric and battery technologies further reduces emissions while ensuring the aircraft maintains the performance required for these applications.

North America zero emission aircraft market is expected to generate USD 8.7 billion by 2034, fueled by significant investments and government initiatives aimed at reducing aviation-related carbon emissions. The region is leading the way in the development of electric and hydrogen-powered aircraft, with strong contributions from both established manufacturers and innovative startups. These advancements are not only supporting regional air travel sustainability but also contributing to the wider adoption of cleaner technologies across the industry. North America's leadership in this space is instrumental in shaping global aviation standards and achieving global emission reduction goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing government support for clean aviation technologies

- 3.6.1.2 Rising demand for sustainable and eco-friendly aviation solutions

- 3.6.1.3 Technological advancements in battery and fuel cell systems

- 3.6.1.4 Growing pressure for airlines to reduce carbon emissions

- 3.6.1.5 Expansion of green aviation infrastructure and charging networks

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and production costs of zero-emission aircraft

- 3.6.2.2 Limited range and energy density of current battery technology

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Aircraft Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Battery electric aircraft

- 5.3 Hydrogen fuel cell aircraft

- 5.4 Hybrid electric aircraft

- 5.5 Solar electric aircraft

Chapter 6 Market Estimates & Forecast, By Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Turboprop

- 6.3 Turbofan system

- 6.4 Blended-Wing Body (BWB)

- 6.5 Fully electrical concept

Chapter 7 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 9 to 30

- 7.3 31 to 60

- 7.4 61 to 100

- 7.5 101 to 150

- 7.6 More than 150

Chapter 8 Market Estimates & Forecast, By End-use, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Military

- 8.4 General

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ampaire Inc.

- 10.2 Aurora Flight Sciences (The Boeing Company)

- 10.3 BETA Technologies, Inc.

- 10.4 Bye Aerospace

- 10.5 Equator Aircraft AS

- 10.6 Evektor, spol. s r. o.

- 10.7 Eviation

- 10.8 Heart Aerospace

- 10.9 Joby Aero, Inc.

- 10.10 Lilium GmbH

- 10.11 PIPISTREL d.o.o.

- 10.12 Rolls-Royce plc

- 10.13 Wright Electric

- 10.14 ZeroAvia, Inc.