|

시장보고서

상품코드

1667113

서큘러 폴리머 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Circular Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

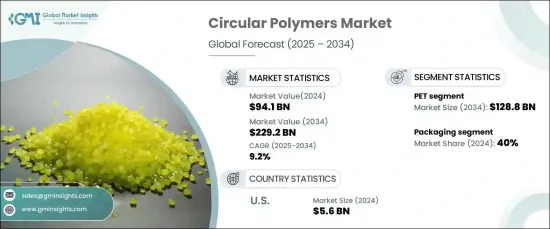

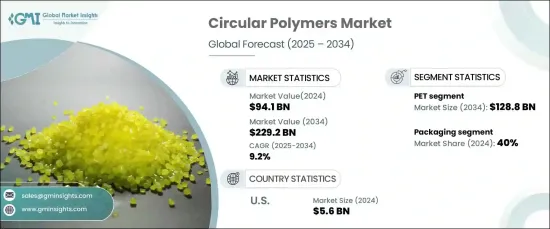

세계의 서큘러 폴리머 시장은 2024년에 941억 달러에 이르렀으며, 2025년부터 2034년에 걸쳐 9.2%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다.

환경에 대한 우려가 커지고 천연자원의 이용가능량이 감소함에 따라, 산업계에서는 폐기물의 삭감과 자원효율의 극대화에 중점을 둔 실천을 채용하는 경향이 강해지고 있습니다. 이러한 지속가능한 자원 관리로의 전환은 제조, 포장, 소비재 등 다양한 분야에 걸쳐 있어 서큘러 폴리머 수요를 끌어올리고 있습니다.

환경의 지속가능성에 대한 소비자 의식 증가는 구매 의사결정에 큰 영향을 미치고, 서큘러 폴리머로 포장된 제품에 대한 수요를 높이고 있습니다. 소비자는 플라스틱 폐기물의 유해한 영향을 의식하게 되어, 보다 환경 친화적인 대체품을 적극적으로 요구하게 되어 있습니다. 결과적으로 내구성 있고 지속 가능한 제품에 대한 수요가 증가함에 따라 제조업체는 포장 솔루션으로 서큘러 폴리머를 채택했습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025년-2034년 |

| 시작금액 | 941억 달러 |

| 예측 금액 | 2,292억 달러 |

| CAGR | 9.2% |

시장은 주로 폴리머 유형으로 구분되며 PET, 폴리에틸렌, 폴리 프로파일렌, PVC 등이 있습니다. 이 중 PET 분야는 2024년에 504억 달러를 창출했으며, 2034년에는 1,288억 달러에 이를 것으로 예측되고 있습니다. PET(폴리에틸렌 테레프탈레이트)는 뛰어난 재활용성과 다용도로 서큘러 폴리머 시장에서 지지를 받고 있습니다. 포장, 특히 병과 용기에 널리 사용되는 PET는 높은 회수율의 혜택을 받으며 재활용을 위한 안정적인 공급을 보장합니다. 또한 PET는 여러 재활용 사이클을 통해 그 특성을 유지할 수 있으므로 폐쇄 루프 시스템에 이상적입니다. 또한 화학적 해중합과 같은 재활용 기술의 발전으로 PET의 품질이 향상되고 재사용 가능성이 높아지고 있습니다.

서큘러 폴리머 시장에서는 포장이 주요 용도 분야이며 2024년에는 40%의 점유율을 차지했습니다. 이 성장의 원동력이 되고 있는 것은 플라스틱 폐기물과 싸우고 산업계 전체에서 지속가능성에 대한 대처를 강화할 필요성입니다. 서큘러 폴리머는 성능과 효율성을 유지하면서 환경 부하를 줄이기 때문에 패키징에서의 사용이 증가하고 있습니다. 지속 가능한 포장으로의 이동은 식품, 음료, 소비재, 의약품 등의 분야에서 두드러집니다. 브랜드는 소비자 수요에 부응하고 규제 기준을 충족하기 위해 환경 친화적인 패키징 솔루션을 요구하고 있습니다. 서큘러 폴리머, 특히 재생 PET(r-PET)는 내구성이 뛰어나고 재활용 가능하고 고품질의 대체 패키지를 제공합니다.

미국의 서큘러 폴리머 시장은 2024년 56억 달러로 평가되었습니다. 이 시장의 성장은 지속 가능한 폐기물 관리와 미사용 플라스틱의 사용 감소를 추진하는 규제가 큰 요인이 되고 있습니다. 친환경 제품, 특히 패키징에 대한 소비자 선호 증가는 제조업체에게 재활용 폴리머를 채택하도록 촉구합니다. 화학 재활용과 같은 첨단 재활용 기술에 대한 투자로 재활용 재료의 품질이 향상되고 다양한 산업 분야에서의 용도가 확대되고 있습니다. 기업의 지속가능성에 대한 노력과 주요 기업의 탄소 중립에 대한 헌신도 서큘러 폴리머의 보급을 뒷받침하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차

- 2차

- 유료소스

- 공적소스

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 변혁

- 장래의 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향요인

- 성장 촉진요인

- 카본 풋 프린트를 삭감하기 위해서 재활용 소재를 사용하는 것의 의식이 각 업계에서 높아지고 있다

- 포장업계에 있어서의 재활용 가능한 재료의 채용 증가가 시장을 견인하고 있다

- 재생 플라스틱의 보급을 향한 적극적인 대처

- 업계의 잠재적 리스크 및 과제

- 재생 플라스틱보다 미사용 플라스틱을 사용하는 경향

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 규모와 예측 : 폴리머별, 2021년-2034년

- 주요 동향

- PET

- 폴리에틸렌

- 폴리프로필렌

- PVC

- 기타

제6장 시장 규모와 예측 : 용도별, 2021년-2034년

- 주요 동향

- 포장

- 건축 및 건설

- 자동차

- 전기 및 전자

- 농업

- 기타

제7장 시장 규모와 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제8장 기업 프로파일

- Advanced Circular Polymers

- ALBA Group

- Banyan

- BASF

- Borealis

- Circular Polymers

- Dow

- ExxonMobil

- KW Plastics

- PlastiCycle

- Quality Circular Polymers

- SABIC

- The Shakti Plastic Industries

- Total Energies

- Veolia

The Global Circular Polymers Market reached USD 94.1 billion in 2024 and is projected to grow at a robust CAGR of 9.2% between 2025 and 2034. As environmental concerns intensify and the availability of natural resources dwindles, industries are increasingly adopting practices that focus on waste reduction and maximizing resource efficiency. This shift toward sustainable resource management spans various sectors, including manufacturing, packaging, and consumer goods, boosting the demand for circular polymers.

Rising awareness among consumers about environmental sustainability has significantly influenced purchasing decisions, driving demand for products packaged in circular polymers. Consumers are becoming more conscious of the detrimental impact of plastic waste and are actively seeking more environmentally friendly alternatives. As a result, manufacturers are turning to circular polymers for packaging solutions to meet the growing demand for durable and sustainable products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $94.1 Billion |

| Forecast Value | $229.2 Billion |

| CAGR | 9.2% |

The market is primarily segmented by polymer type, including PET, polyethylene, polypropylene, PVC, and others. Among these, the PET segment generated USD 50.4 billion in 2024 and is projected to reach USD 128.8 billion by 2034. PET (Polyethylene Terephthalate) is favored in the circular polymer market due to its exceptional recyclability and versatility. Widely used in packaging, especially for bottles and containers, PET benefits from high recovery rates, ensuring a consistent supply for recycling. Its ability to retain its properties through multiple recycling cycles makes it ideal for closed-loop systems. Furthermore, advances in recycling technologies, like chemical depolymerization, are improving PET's quality and enhancing its reuse potential.

Packaging is the dominant application segment in the circular polymers market, accounting for a 40% share in 2024. This growth is driven by the need to combat plastic waste and enhance sustainability efforts across industries. Circular polymers are increasingly used in packaging because they help reduce environmental impact while maintaining performance and efficiency. The shift toward sustainable packaging is noticeable across sectors such as food, beverage, consumer goods, and pharmaceuticals. Brands are increasingly seeking eco-friendly packaging solutions to cater to consumer demand and meet regulatory standards. Circular polymers, particularly recycled PET (r-PET), provide a durable, recyclable, and high-quality alternative for packaging.

U.S. circular polymers market was valued at USD 5.6 billion in 2024. The growth in this market is largely driven by regulations promoting sustainable waste management and a reduction in the use of virgin plastics. The rising consumer preference for eco-friendly products, particularly in packaging, is encouraging manufacturers to adopt recycled polymers. Investment in advanced recycling technologies, such as chemical recycling, is improving the quality of recycled materials, broadening their applications across various industries. Corporate sustainability initiatives and commitments to carbon neutrality by leading companies are also driving the widespread adoption of circular polymers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising awareness among various industries to use recycled materials to reduce their carbon footprints

- 3.6.1.2 Increasing adoption of recyclable materials in the packaging industry is driving the market

- 3.6.1.3 Favorable initiatives to promote recycled plastics

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Inclination toward the use of virgin plastics over recycled polymers

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Polymer, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 PET

- 5.3 Polyethylene

- 5.4 Polypropylene

- 5.5 PVC

- 5.6 Others

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Packaging

- 6.3 Building & construction

- 6.4 Automotive

- 6.5 Electrical & electronics

- 6.6 Agriculture

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Advanced Circular Polymers

- 8.2 ALBA Group

- 8.3 Banyan

- 8.4 BASF

- 8.5 Borealis

- 8.6 Circular Polymers

- 8.7 Dow

- 8.8 ExxonMobil

- 8.9 KW Plastics

- 8.10 PlastiCycle

- 8.11 Quality Circular Polymers

- 8.12 SABIC

- 8.13 The Shakti Plastic Industries

- 8.14 Total Energies

- 8.15 Veolia