|

시장보고서

상품코드

1667123

회로 차단식 전환 스위치 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Circuit Breaker Based Transfer Switch Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

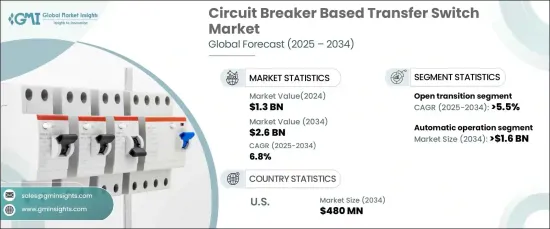

세계의 회로 차단식 전환 스위치 시장은 2024년 13억 달러에 이르고, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 6.8%로 전망됩니다.

이러한 성장의 주요 원인은 건강 관리, 데이터센터, 산업 시설 등의 중요한 산업에서 신뢰할 수 있는 전력 전송 솔루션에 대한 수요가 증가하고 있다는 것입니다. 이 분야는 무정전 전력 공급에 크게 의존하고 있으며 회로 차단식 전환 스위치, 정전 및 장애가 발생하더라도 부드럽고 효율적인 전력 전환을 실현합니다.

지속적이고 고품질의 전력에 대한 의존도가 증가함에 따라 이러한 장치의 채택을 더욱 강화하고 있습니다. 전력 중단을 방지하고 고장을 처리하며 가혹한 조건에서도 완벽한 성능을 발휘하는 이러한 장비는 현대 전력 인프라에서 필수적입니다. 기업과 조직이 지속적인 비즈니스 연속성을 선호하는 동안 고급 전력 전송 솔루션에 대한 수요가 급증하고 있습니다. 이러한 성장은 특히 신재생에너지원과 하이브리드 전력시스템의 통합이 진행되고 있는 것에 영향을 받고 있으며, 모두 효율적인 운용에는 첨단 전력 관리 솔루션이 필요합니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작금액 | 13억 달러 |

| 예측금액 | 26억 달러 |

| CAGR | 6.8% |

자동화 및 백업 전원 시스템의 급증도 시장 확대를 뒷받침하는 중요한 요소입니다. 정전 시 자동으로 원활한 전력 전송을 수행하는 자동 전송 스위치(ATS)는 특히 전력 중단이 허용되지 않는 환경에서 빠르게 확산되고 있습니다. 원격 모니터링, 스마트 제어, 고급 자동화 등의 이점도 더해져, ATS는 높은 신뢰성이 요구되는 부문에 있어서 중요한 솔루션이 되고 있습니다.

이러한 시스템은 정전 시 운영 효율성을 높이는 데 필수적인 역할을 하며, 병원, 데이터센터, 산업 운영 등과 같은 중요한 용도에서 매우 귀중한 존재가 되었습니다. 이러한 솔루션에 대한 수요 증가는 신흥 경제 국가의 인프라 개발에 의해 더욱 강화되고 있습니다. 신흥경제국은 지속적이고 안정적인 전력공급에 대한 요구 증가에 대응하기 위해 에너지 인프라 업그레이드에 주력하고 있습니다.

시장의 자율주행 부문은 2034년까지 16억 달러에 달할 것으로 예상됩니다. ATS의 광범위한 채택은 특히 엄격한 전력 신뢰성을 요구하는 산업에서 이러한 성장의 주요 추진력이 되었습니다. 이러한 시스템은 정전 시 자동 백업 전원을 제공하여 기업에 안심감을 주고 가동 중지 시간의 위험을 줄입니다. 한편, 저렴한 가격과 신뢰성으로 인기 있는 오픈 트랜지션 회로 차단기식 전환 스위치 시장은 CAGR 5.5%의 성장이 전망되고 있습니다. 이러한 스위치는 일반적으로 단시간 정전이 허용되는 중요도가 낮은 응용 분야에서 사용되기 때문에 정전이 자주 발생하는 상업 부문 및 산업 부문에 가장 적합한 옵션이 되었습니다.

미국 회로 차단기 전환 스위치 시장은 2034년까지 4억 8,000만 달러에 이를 전망입니다. 이 성장의 주요 요인은 에너지 인프라의 현대화에 점점 더 많은 힘을 쏟고 있으며 다양한 부서에서 백업 전원 솔루션에 대한 수요가 증가하고 있다는 것입니다. 미국은 특히 정전의 영향을 받기 쉽기 때문에 안정적인 전원 관리 시스템의 필요성이 더욱 커지고 있습니다. 또한 에너지 효율 향상을 목표로 하는 규제에 대한 노력이 계속되고 있으며, 자동화 기술의 진보도 이러한 필수적인 전원 솔루션의 지속적인 채용을 뒷받침할 것으로 예상됩니다.

목차

제1장 조사 방법과 조사 범위

- 시장의 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차

- 2차

- 유상

- 공적

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

제4장 경쟁 구도

- 전략 대시보드

- 혁신과 지속가능성의 전망

제5장 시장 규모와 예측 : 조작별, 2021-2034년

- 주요 동향

- 수동

- 비자동

- 자동

- 바이패스 분리

제6장 시장 규모와 예측 : 트랜지션별, 2021-2034년

- 주요 동향

- 폐쇄

- 개방

제7장 시장 규모와 예측 : 설치별, 2021-2034년

- 주요 동향

- 긴급 시스템

- 법정 시스템

- 중요 업무 전원 시스템

- 옵션 대기 시스템

제8장 시장 규모와 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 러시아

- 영국

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

- 라틴아메리카

- 브라질

- 아르헨티나

제9장 기업 프로파일

- ABB

- AEG Power Solutions

- Briggs & Stratton

- Caterpillar

- Cummins

- DAIER

- Eaton

- Generac Power Systems

- General Electric

- Kohler

- Midwest Electric Products

- One Two Three Electric

- Peterson

- Schneider Electric

- Siemens

- Taylor Power Systems

- Vertiv Group

The Global Circuit Breaker Based Transfer Switch Market reached USD 1.3 billion in 2024 and is expected to exhibit a CAGR of 6.8% from 2025 to 2034. This growth is primarily driven by the increasing demand for reliable power transfer solutions across critical industries such as healthcare, data centers, and industrial facilities. These sectors depend heavily on uninterrupted power supply, and circuit breaker-based transfer switches ensure smooth and efficient power transitions in the event of outages or failures.

The rising reliance on continuous, high-quality power is further boosting the adoption of these devices. Their ability to prevent power disruptions, handle faults, and provide seamless performance under harsh conditions makes them essential in modern power infrastructure. As businesses and organizations continue to prioritize operational continuity, the demand for advanced power transfer solutions is soaring. This growth is particularly influenced by the increasing integration of renewable energy sources and hybrid power systems, both of which require sophisticated power management solutions to operate efficiently.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 6.8% |

The surge in automation and backup power systems is another critical factor fueling the market's expansion. Automated transfer switches (ATS), which provide automatic, seamless power transfers during outages, are rapidly gaining traction, especially in environments where power disruptions are not an option. With the added benefits of remote monitoring, smart controls, and advanced automation, ATS has become a key solution for sectors demanding high reliability.

These systems play an integral role in enhancing operational efficiency during power outages, making them invaluable in critical applications like hospitals, data centers, and industrial operations. The growing demand for these solutions is further bolstered by infrastructure developments in emerging economies, which are focusing on upgrading energy infrastructure to meet the increasing need for continuous, stable power delivery.

The automatic operation segment of the market is expected to reach USD 1.6 billion by 2034. The widespread adoption of ATS is a major driver of this growth, particularly in industries with stringent power reliability needs. These systems provide automatic backup power during outages, offering businesses peace of mind and reducing the risk of downtime. On the other hand, the open transition circuit breaker-based transfer switch market, which is popular for its affordability and dependability, is expected to grow at a CAGR of 5.5%. These switches are commonly used in less-critical applications where brief power interruptions are acceptable, making them a go-to option for commercial and industrial sectors that frequently experience power disruptions.

In the U.S., the circuit breaker-based transfer switch market is poised to reach USD 480 million by 2034. This growth is primarily attributed to the nation's increasing focus on modernizing its energy infrastructure and the rising demand for backup power solutions across various sectors. The U.S. is particularly vulnerable to power disruptions, which further underscores the need for reliable power management systems. Additionally, ongoing regulatory efforts aimed at improving energy efficiency and advancements in automation technologies are expected to drive the continued adoption of these essential power solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Operations, 2021 – 2034 (‘000 Units, USD Million)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Non-automatic

- 5.4 Automatic

- 5.5 By-pass isolation

Chapter 6 Market Size and Forecast, By Transition, 2021 – 2034 (‘000 Units, USD Million)

- 6.1 Key trends

- 6.2 Closed

- 6.3 Open

Chapter 7 Market Size and Forecast, By Installation, 2021 – 2034 (‘000 Units, USD Million)

- 7.1 Key trends

- 7.2 Emergency systems

- 7.3 Legally required systems

- 7.4 Critical operations power systems

- 7.5 Optional standby systems

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (‘000 Units, USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Russia

- 8.3.4 UK

- 8.3.5 Italy

- 8.3.6 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 South Africa

- 8.5.3 Saudi Arabia

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 AEG Power Solutions

- 9.3 Briggs & Stratton

- 9.4 Caterpillar

- 9.5 Cummins

- 9.6 DAIER

- 9.7 Eaton

- 9.8 Generac Power Systems

- 9.9 General Electric

- 9.10 Kohler

- 9.11 Midwest Electric Products

- 9.12 One Two Three Electric

- 9.13 Peterson

- 9.14 Schneider Electric

- 9.15 Siemens

- 9.16 Taylor Power Systems

- 9.17 Vertiv Group