|

시장보고서

상품코드

1684197

PVC 랩 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)PVC Cling Film Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

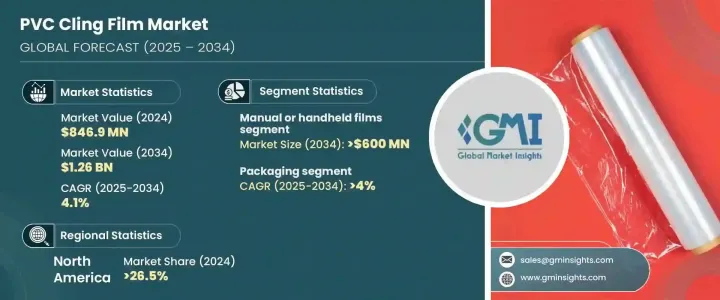

세계의 PVC 랩 시장은 2024년에 8억 4,690만 달러로 평가되었고, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 4.1%로 성장할 것으로 예측됩니다.

이 성장의 주요 원동력은 환경 친화적이고 지속 가능한 패키징 솔루션에 대한 수요 증가입니다. 환경문제에 대한 의식이 고조되고 플라스틱 폐기물 규제가 엄격해지면서 세계의 지속가능성에 대한 노력에 따른 재활용 가능한 소재로의 이동이 명확해지고 있습니다. 소비자와 제조업체 모두 이산화탄소 배출량을 줄이고, 계속 발전하는 재활용 기준을 충족하는 보다 친환경적인 옵션을 선호합니다. 지속가능한 포장에 대한 선호도 증가는 특히 식품 및 비식품 포장과 같은 분야에서 두드러지며, 환경 친화적인 선택이 표준이 되고 있습니다. 이러한 추세가 소비자 행동을 형성하는 동안 PVC 랩, 특히 보다 지속 가능한 형태의 필름에 대한 수요는 급증할 것으로 예상됩니다.

시장은 기계 필름과 수동 또는 핸드헬드 필름으로 나뉘며, 수동 분야는 성장 측면에서 유력한 후보로 부상하고 있습니다. 2034년까지 수동 PVC 랩 부문은 6억 달러를 창출할 것으로 예상됩니다. 이 성장은 특히 가정이나 소규모 포장 작업에서 식품 보존을 위해 수동 필름을 널리 사용하는 것이 주요 원인입니다. 수동 랩은 식품을 신선하게 유지하기 위한 실용적이고 예산 친화적인 솔루션입니다. 이 랩은 간단하고 비용 효율적이며 사용하기 쉽기 때문에 효율적이고 저렴한 식품 보존 방법을 찾고있는 소비자에게 선택됩니다. 널리 이용가능하고 다재다능한 것이 또한 이 분야에서의 우위성을 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 8억 4,690만 달러 |

| 예측 금액 | 12억 6,000만 달러 |

| CAGR | 4.1% |

최종 용도의 경우 PVC 랩 시장은 식품 포장과 비식품 포장으로 크게 나뉩니다. 식품 포장 분야가 선도하고 있으며, 2025년부터 2034년까지 CAGR 4%의 성장이 전망되고 있습니다. PVC 랩은 유통 기한을 연장하고 오염물질로부터 보호함으로써 고기와 야채에서 과일까지 신선한 식품의 보존에 중요한 역할을 합니다. 특히 페이스가 빠른 라이프스타일 속에서 신선하고 편리한 식사와 포장 크기의 소형화가 중시되고, 기본적인 식품 보존 도구로서 PVC 랩 수요가 높아지고 있습니다. 이동 중에도 먹을 수 있는 음식, 즉각적으로 먹을 수 있는 제품, 온라인 식품 배달의 인기는 고품질의 효과적인 패키징 솔루션의 필요성을 더욱 높여줍니다.

북미, 특히 미국은 2024년 PVC 랩 시장 점유율의 26.5%를 차지했습니다. 이 지역은 신선하고 시각적으로 호소하는 편리한 식품에 대한 수요 증가로 현저한 성장을 이루고 있습니다. 빨리 먹을 수 있는 다이어트 증가, 온라인 식품 택배 서비스의 붐, 운송 중 제품 품질 유지에 대한 주목은 내구성 있고 효과적인 포장 옵션의 필요성을 추진하는 주요 요인입니다. 또한, 투명성과 내구성을 향상시키는 필름 제조 기술 혁신이 시장 확대에 기여하고 있으며, 제조업체는 식품 포장 분야의 고품질 랩에 대한 수요 증가에 확실히 대응할 수 있습니다.

목차

제1장 조사 방법 및 조사 범위

- 시장 범위 및 정의

- 기본 추정 및 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 데이터

- 유료 정보원

- 공적 정보원

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 파괴

- 장래 전망

- 제조업체

- 유통업체

- 주요 뉴스 및 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 지속 가능한 패키징 솔루션에 대한 수요 증가

- 필름 기술 및 성능의 진보

- 필름의 경량화, 박막화에 의한 비용 효율화

- 신선도 유지에 대한 소비자 기호의 고조

- 진화하는 규제 요건에 대응

- 업계의 잠재적 위험 및 과제

- 첨단 필름의 높은 제조 비용

- PVC 대체품 시장에서의 강한 존재감

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 기계용 필름

- 핸드헬드 필름

제6장 시장 추계 및 예측 : 두께별(2021-2034년)

- 주요 동향

- 10 미크론까지

- 10-15 미크론

- 15-20 미크론

- 20 미크론 이상

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 식품 포장

- 고기, 닭고기 및 해산물

- 신선한 식품

- 냉동식품

- 베이커리 및 과자류

- 기타

- 비식품 포장

- 공업제품

- 일렉트로닉스

- 의료 및 의약품

- 기타

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- BenKai

- Berry Global

- Boston Polymers

- Changzhou Plastics Researching and Manufacturing

- CL Industries India

- Divya Plastic Industries

- Galaxy Converting

- IPG

- Jiashan Hengyu Plastic

- Magnum Packaging

- Maskati Bros

- Nan Ya Plastics

- NRR Industries

- Pactiv Evergreen

- Pragya Flexifilm Industries

- Qingdao Kingchuan Packaging

- Shenzhen Jingfeng Industrial

- US Packaging and Wrapping

- Zhengzhou Eming Aluminium Industry

The Global PVC Cling Film Market reached USD 846.9 million in 2024 and is projected to grow at a CAGR of 4.1% from 2025 to 2034. A key driver behind this growth is the increasing demand for eco-friendly and sustainable packaging solutions. With rising awareness of environmental challenges and more stringent plastic waste regulations, there is a clear shift toward recyclable materials that align with global sustainability efforts. Consumers and manufacturers alike are prioritizing greener options that reduce carbon footprints and meet the ever-evolving recycling standards. The growing preference for sustainable packaging is particularly visible in sectors like food and non-food packaging, where eco-conscious choices are becoming the norm. As these trends continue to shape consumer behavior, the demand for PVC cling film, especially in its more sustainable forms, is expected to surge.

The market is divided into machine films and manual or handheld films, with the manual segment emerging as a strong contender in terms of growth. By 2034, the manual PVC cling film segment is projected to generate USD 600 million. This growth is largely attributed to the widespread use of manual films for food storage, particularly in households and small-scale packaging operations. Manual cling films offer a practical and budget-friendly solution for keeping food fresh. The simplicity, cost-effectiveness, and ease of use of these films make them the go-to choice for consumers looking for an efficient and affordable food preservation method. Their widespread availability and versatility further contribute to their dominance in this sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $846.9 Million |

| Forecast Value | $1.26 Billion |

| CAGR | 4.1% |

When it comes to end-use applications, the PVC cling film market is largely split between food and non-food packaging. The food packaging segment is leading the way and is expected to grow at a CAGR of 4% from 2025 to 2034. PVC cling films play a vital role in the preservation of fresh food, from meats and vegetables to fruits, by extending shelf life and protecting against contaminants. With a growing focus on fresh, convenient meals and smaller packaging sizes, especially in fast-paced lifestyles, the demand for PVC cling films as a fundamental food storage tool is rising. The popularity of on-the-go meals, ready-to-eat products, and online food deliveries further bolsters the need for high-quality, effective packaging solutions.

North America, particularly the United States, accounted for 26.5% of the PVC cling film market share in 2024. This region is experiencing significant growth, driven by the increasing demand for fresh, visually appealing, and convenient food products. The rise of ready-to-eat meals, the boom in online food delivery services, and the focus on maintaining product quality during transportation are key factors propelling the need for durable and effective packaging options. Additionally, technological innovations in film production, which improve clarity and durability, are contributing to the market's expansion, ensuring that manufacturers can meet the growing demand for high-quality cling films in the food packaging sector.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Key news & initiatives

- 3.3 Regulatory landscape

- 3.4 Impact forces

- 3.4.1 Growth drivers

- 3.4.1.1 Rising demand for sustainable packaging solutions

- 3.4.1.2 Advancements in film technology and performance

- 3.4.1.3 Cost efficiency through lighter, thinner films

- 3.4.1.4 Increased consumer preference for freshness retention

- 3.4.1.5 Compliance with evolving regulatory requirements

- 3.4.2 Industry pitfalls & challenges

- 3.4.2.1 High production costs of advanced films

- 3.4.2.2 Strong market presence of PVC alternatives

- 3.4.1 Growth drivers

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Machine films

- 5.3 Manual or handheld films

Chapter 6 Market Estimates & Forecast, By Thickness, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Up to 10 microns

- 6.3 10 to 15 microns

- 6.4 15-20 microns

- 6.5 Above 20 microns

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Food packaging

- 7.2.1 Meat poultry, & seafood

- 7.2.2 Fresh produce

- 7.2.3 Frozen food

- 7.2.4 Bakery and confectionery

- 7.2.5 Others

- 7.3 Non-food packaging

- 7.3.1 Industrial goods

- 7.3.2 Electronics

- 7.3.3 Medical and pharmaceutical

- 7.3.4 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BenKai

- 9.2 Berry Global

- 9.3 Boston Polymers

- 9.4 Changzhou Plastics Researching and Manufacturing

- 9.5 CL Industries India

- 9.6 Divya Plastic Industries

- 9.7 Galaxy Converting

- 9.8 IPG

- 9.9 Jiashan Hengyu Plastic

- 9.10 Magnum Packaging

- 9.11 Maskati Bros

- 9.12 Nan Ya Plastics

- 9.13 NRR Industries

- 9.14 Pactiv Evergreen

- 9.15 Pragya Flexifilm Industries

- 9.16 Qingdao Kingchuan Packaging

- 9.17 Shenzhen Jingfeng Industrial

- 9.18 US Packaging and Wrapping

- 9.19 Zhengzhou Eming Aluminium Industry