|

시장보고서

상품코드

1684522

해군 함정 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Naval Vessels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

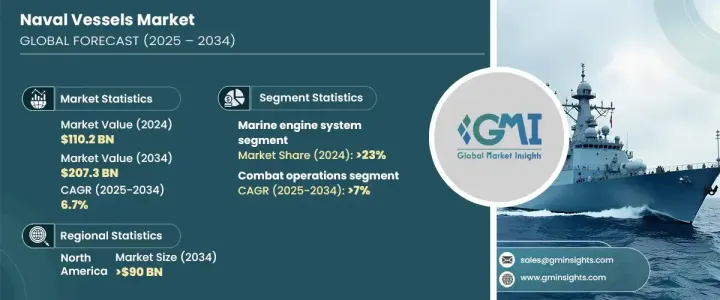

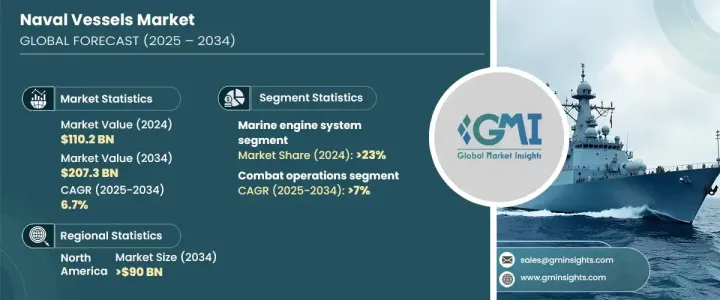

세계의 해군 함정 시장은 2024년에 1,102억 달러에 이르렀고, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 6.7%를 나타낼 것으로 전망됩니다. 이 성장 궤도는 세계 안보 위협이 증가하고 있음을 반영하고 있으며 고급 공격 및 방어 무기 시스템에 대한 수요가 전례 없이 급증하고 있습니다. 세계 정부 및 방위기관은 해상 안보를 강화하고 진화하는 위협에 대처하기 위해 최첨단 해군 기술에 많은 투자를 하고 있습니다. 해군 함정의 근대화는 인공지능(AI), 자율시스템, 선진추진기술의 통합과 함께 시장 전망을 재구성하고 있습니다. 지정학적 긴장 증가와 해양 영토를 둘러싼 분쟁은 국가 안보 전략에서 해군 함정의 중요한 역할을 더욱 강조하고 있습니다. 게다가 친환경 추진 시스템으로의 전환은 운영 효율성과 함께 지속가능성을 강조하고 엄격한 환경규제에 대한 대응을 보여줍니다.

시장은 시스템별로 선박용 엔진 시스템, 무기 발사 시스템, 제어 시스템, 전기 시스템, 통신 시스템 등으로 구분됩니다. 이 중 선박용 엔진시스템 분야는 2024년 시장 점유율의 23%를 차지했으며 향후 수년간 크게 확대될 것으로 예측됩니다. 해군 함정의 추진 기술은 급속히 진보하고 있으며, 하이브리드 시스템이나 바이오연료 구동 시스템으로의 시프트가 현저합니다. 이러한 기술은 기존의 연료 엔진에 전기 모터를 통합하는 것으로, 최신의 구축함이나 잠수함의 전술적·운용적 요구에 대응하는 것과 동시에, 환경상의 의무에도 합치하고 있습니다. 에너지 효율적인 시스템의 추진은 성능을 저하시키지 않고 군사 작전의 이산화탄소 배출량을 줄이는 데 중점을 두고 있음을 반영합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 1,102억 달러 |

| 예측 금액 | 2,073억 달러 |

| CAGR | 6.7% |

용도별로는 연안 작전, 수색 구조 임무, 전투 작전, 지뢰 대책(MCM) 작전 등으로 분류됩니다. 전투작전 분야는 2034년까지 연평균 복합 성장률(CAGR) 7%를 기록하며 강력하게 성장할 것으로 예상됩니다. 극초음속 미사일 기술, 지향성 에너지 시스템, 정밀 어뢰 등의 혁명적 진보는 해군 전투 부대의 능력을 변화시키고 있습니다. 이 기술은 무기의 사거리, 정확성 및 전반적인 효과를 향상시키고 해안 및 기타 지역에 뛰어난 방어 능력을 제공합니다. 게다가 AI와 자율기술의 통합은 해군 작전을 근본적으로 바꾸어 신속한 위협 감지, 합리화된 임무 수행, 여러 영역에 걸친 상황 인식의 강화를 가능하게 하고 있습니다.

북미는 특히 구축함과 잠수함 분야에서 해군 함정 시장의 주요 기업로 남아 있습니다. 이 지역은 미국이 해군 능력 강화에 주력하고 있기 때문에 2034년까지 900억 달러 시장 규모에 이를 것으로 예측되고 있습니다. 미국은 극초음속 무기와 자율 시스템에 대한 엄청난 투자로 시장을 주도하고 있으며 전략적 이점과 타의 추종을 불허하는 운영 효율성을 확보하고 있습니다. 해군 함정 시장의 성장은 방위 투자 증가, 추진 기술의 진보, AI와 자율형 솔루션의 채용 확대에 의해 촉진되어 세계의 해상 안보에 있어서 중요한 역할을 확고히 하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 데이터

- 유료 소스

- 공적 소스

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 방해

- 향후 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향요인

- 성장 촉진요인

- 지정학적 긴장의 고조와 군사 근대화

- 방위 예산 증가

- 잠수함을 기반으로 한 전략 방어에 대한 수요 증가

- 해양 안보에 대한 주목 고조

- 해군 함대의 다양화에 대한 주목 고조

- 업계의 잠재적 위험 및 과제

- 높은 개발 비용과 유지 보수 비용

- 지정학적 불안정성과 규제상의 제약

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계·예측 : 함정 유형별(2021-2034년)

- 주요 동향

- 구축함

- 호위함

- 잠수함

- 코르벳함

- 항공모함

- 기타

제6장 시장 추계·예측 : 시스템별(2021-2034년)

- 주요 동향

- 선박 엔진 시스템

- 무기 발사 시스템

- 제어 시스템

- 전기 시스템

- 통신 시스템

- 기타

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 수색 및 구조

- 전투 작전

- 기뢰 대책(MCM) 작전

- 해안 작전

- 기타

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Austal

- BAE Systems

- Damen Shipyards

- Fincantieri

- General Dynamics

- Hanwha Ocean

- HD Korea Shipbuilding

- Huntington Ingalls

- Larsen &Toubro

- Lockheed Martin

- Naval Group

- ThyssenKrupp

The Global Naval Vessels Market reached USD 110.2 billion in 2024 and is poised to grow at a CAGR of 6.7% between 2025 and 2034. This growth trajectory reflects the rising prevalence of security threats across the globe, which has led to an unprecedented surge in demand for advanced offensive and defensive weapon systems. Governments and defense organizations worldwide are investing heavily in cutting-edge naval technologies to strengthen their maritime security and address evolving threats. The modernization of naval fleets, combined with the integration of artificial intelligence (AI), autonomous systems, and advanced propulsion technologies, is reshaping the market landscape. Increasing geopolitical tensions and disputes over maritime territories further underscore the critical role of naval vessels in national security strategies. Additionally, the transition toward eco-friendly propulsion systems demonstrates the sector's response to stringent environmental regulations, emphasizing sustainability alongside operational efficiency.

The market is segmented by system into marine engine systems, weapon launch systems, control systems, electrical systems, communication systems, and others. Among these, the marine engine systems segment accounted for 23% of the market share in 2024 and is anticipated to expand significantly in the coming years. Propulsion technologies for naval vessels are advancing rapidly, with a notable shift toward hybrid and biofuel-driven systems. These technologies integrate electric motors with conventional fuel engines, aligning with environmental mandates while addressing the tactical and operational needs of modern destroyers and submarines. The push for energy-efficient systems reflects a growing emphasis on reducing the carbon footprint of military operations without compromising performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $110.2 billion |

| Forecast Value | $207.3 billion |

| CAGR | 6.7% |

By application, the market is categorized into coastal operations, search and rescue missions, combat operations, Mine Countermeasures (MCM) operations, and others. The combat operations segment is expected to witness robust growth, registering a CAGR of 7% through 2034. Revolutionary advancements such as hypersonic missile technology, directed energy systems, and precision torpedoes are transforming the capabilities of naval combat forces. These technologies enhance weapon range, accuracy, and overall effectiveness, providing superior defense capabilities for coastal regions and beyond. Furthermore, the integration of AI and autonomous technologies has fundamentally changed naval operations, enabling rapid threat detection, streamlined mission execution, and enhanced situational awareness across multiple domains.

North America remains a key player in the naval vessels market, particularly in the destroyers and submarines segments. The region is projected to generate USD 90 billion in value by 2034, driven by the United States' focus on advancing naval capabilities. The U.S. continues to lead the market with substantial investments in hypersonic weapons and autonomous systems, ensuring strategic dominance and unmatched operational efficiency. The naval vessels market growth is fueled by rising defense investments, advancements in propulsion technologies, and the growing incorporation of AI and autonomous solutions, solidifying its critical role in global maritime security.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing geopolitical tensions and military modernization

- 3.6.1.2 Increasing defense budgets

- 3.6.1.3 Growing demand for submarine-based strategic defense

- 3.6.1.4 Rising focus on maritime security

- 3.6.1.5 Increased focus on naval fleet diversification

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and maintenance costs

- 3.6.2.2 Geopolitical instability and regulatory constraints

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vessel Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Destroyers

- 5.3 Frigates

- 5.4 Submarines

- 5.5 Corvettes

- 5.6 Aircraft carriers

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By System, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Marine engine system

- 6.3 Weapon launch system

- 6.4 Control system

- 6.5 Electrical system

- 6.6 Communication system

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Search and rescue

- 7.3 Combat operations

- 7.4 Mine countermeasures (MCM) operations

- 7.5 Coastal Operations

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Austal

- 9.2 BAE Systems

- 9.3 Damen Shipyards

- 9.4 Fincantieri

- 9.5 General Dynamics

- 9.6 Hanwha Ocean

- 9.7 HD Korea Shipbuilding

- 9.8 Huntington Ingalls

- 9.9 Larsen & Toubro

- 9.10 Lockheed Martin

- 9.11 Naval Group

- 9.12 ThyssenKrupp