|

시장보고서

상품코드

1684558

칼시뉴린 억제제 시장 : 기회, 성장 촉진요인, 산업 동향 분석(2025-2034년)Calcineurin Inhibitors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

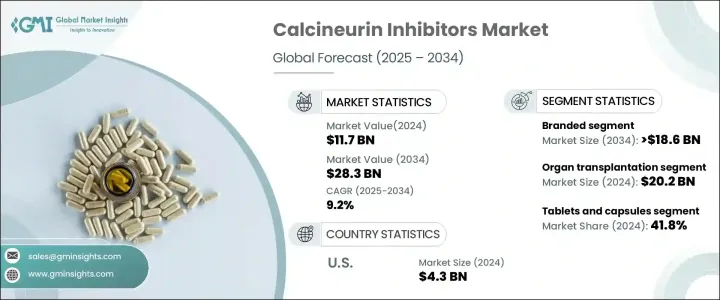

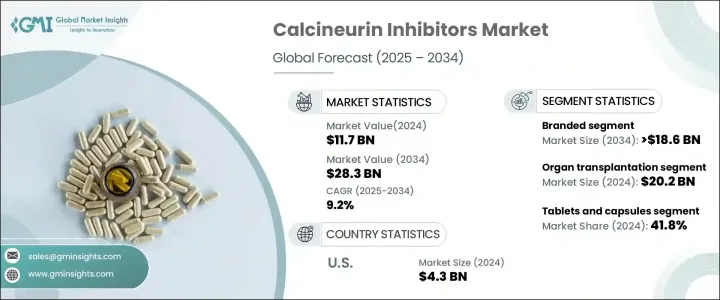

세계의 칼시뉴린 억제제 시장은 2024년에 117억 달러로 평가되었으며, 2025년부터 2034년까지 연평균 성장률(CAGR) 9.2%로 성장할 것으로 예측됩니다.

이러한 시장 성장은 주로 자가 면역 질환의 유병률 증가와 전 세계적으로 증가하는 장기 이식 건수에 의해 촉진됩니다. 칼시뉴린 억제제는 특히 신장, 간, 심장, 폐 이식과 같이 수요가 많은 시술에서 면역 체계를 억제하여 장기 거부를 예방하기 때문에 이식 의학에서 필수적입니다. 이식 성공을 보장하는 데 있어 이러한 약물의 중요한 역할은 계속해서 채택을 촉진하여 시장 수요를 증가시키고 있습니다. 글로벌 의료 환경이 진화함에 따라 인구 고령화 및 장기 부전 발생률 증가 등의 요인으로 인해 장기 이식이 필요한 사람의 수가 증가함에 따라 이러한 면역 억제제에 대한 수요가 더욱 견고해졌습니다.

칼시뉴린 억제제 시장 내 경쟁은 브랜드와 제네릭 옵션으로 세분화됩니다. 시장의 상당 부분을 차지하는 브랜드 부문은 9%의 성장률로 선두를 달릴 것으로 예상됩니다. 2034년에는 186억 달러에 달할 것으로 예상됩니다. 브랜드 칼시뉴린 억제제는 입증된 효능, 강력한 안전성 프로파일, 임상시험 데이터의 탄탄한 뒷받침으로 인해 의료 전문가들 사이에서 여전히 선호되는 선택입니다. 이러한 제품은 엄격한 품질 표준을 충족하도록 제조되어 일관성과 신뢰성을 보장합니다. 따라서 장기 거부 반응의 위험을 최소화하는 것이 성공 여부에 달려 있는 중요한 이식 프로토콜에서 가장 중요한 옵션입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 117억 달러 |

| 예측 금액 | 283억 달러 |

| CAGR | 9.2% |

칼시뉴린 억제제는 주로 장기 이식, 자가 면역 질환, 기타 특수 응용 분야의 세 가지 분야에서 활용되고 있습니다. 장기 이식 부문은 2025년부터 2034년까지 202억 달러의 매출을 창출할 것으로 예상되며, 이는 이식 후 치료에서 이러한 약물의 중심적인 역할을 강조합니다. 신체의 면역 반응을 효과적으로 관리하는 능력은 이식된 장기의 생존을 보장하기 때문에 전 세계 이식 의학에서 없어서는 안 될 필수 요소입니다. 면역 억제 요법이 장기 거부 반응을 예방하는 초석으로 남아 있기 때문에 칼시뉴린 억제제는 이 부문을 계속 지배하고 있습니다.

미국의 칼시뉴린 억제제 시장은 2024년 43억 달러 규모로 2025년부터 2034년까지 8.4%의 연평균 성장률을 보일 것으로 예상됩니다. 미국은 이러한 약물의 핵심 시장으로, 세계 최고의 이식 센터, 강력한 환급 정책, 연구 개발에 대한 강력한 투자로 시장을 주도하고 있습니다. 또한 장기 부전으로 이어지는 당뇨병과 고혈압과 같은 만성 질환의 높은 발병률은 칼시뉴린 억제제에 대한 수요를 더욱 증폭시킵니다. 이러한 요인으로 인해 미국은 글로벌 시장에서 지배적인 위치를 차지하고 있으며, 이 부문에서 지속적인 성장과 혁신을 보장하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 장기 이식 건수 증가

- 자가 면역 질환의 유병률 증가

- 면역 억제 연구 및 개발 활동의 급증

- 업계의 잠재적 리스크 및 과제

- 부작용 및 대체 치료법의 가용성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 상환 시나리오

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 향후 시장 동향

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 브랜드

- 타크로리무스

- 사이클로스포린

- 기타 브랜드 제품

- 제네릭

- 타크로리무스

- 사이클로스포린

- 기타 제네릭 의약품

제6장 시장 추계 및 예측 : 용량별(2021-2034년)

- 주요 동향

- 정제 및 캡슐

- 연고제

- 주사제

- 기타 제형

제7장 시장 추계 및 예측 : 적응증별(2021-2034년)

- 주요 동향

- 장기 이식

- 자가 면역 질환

- 기타 적응증

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- abbvie

- astellas

- Aurinia

- Biocon

- Dr. Reddy's

- Glenmark

- LUPIN

- Novartis

- Roche

- VIATRIS

The Global Calcineurin Inhibitors Market, valued at USD 11.7 billion in 2024, is projected to expand at a CAGR of 9.2% from 2025 to 2034. This market growth is primarily fueled by the increasing prevalence of autoimmune disorders and the rising number of organ transplants across the globe. Calcineurin inhibitors are essential in transplant medicine, as they suppress the immune system to prevent organ rejection, particularly in high-demand procedures such as kidney, liver, heart, and lung transplants. The critical role these medications play in ensuring transplant success continues to drive their adoption, thus enhancing their market demand. As the global healthcare landscape evolves, the increasing number of individuals requiring organ transplants-due to factors like aging populations and the rising incidence of organ failure-has further solidified the demand for these immunosuppressive drugs.

Within the calcineurin inhibitors market, the competition is segmented into branded and generic options. The branded segment, accounting for a significant portion of the market, is anticipated to lead with a growth rate of 9%. By 2034, it is expected to reach USD 18.6 billion. Branded calcineurin inhibitors remain the preferred choice among healthcare professionals because of their proven efficacy, strong safety profiles, and solid backing from clinical trial data. These products are manufactured to meet rigorous quality standards, ensuring consistency and reliability. This makes them the go-to option in critical transplant protocols, where success depends on minimizing the risk of organ rejection.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.7 Billion |

| Forecast Value | $28.3 Billion |

| CAGR | 9.2% |

Calcineurin inhibitors are utilized primarily in three areas: organ transplantation, autoimmune diseases, and other specialized applications. The organ transplantation segment is expected to generate USD 20.2 billion between 2025 and 2034, underlining the central role of these drugs in post-transplant care. Their ability to manage the body's immune response effectively ensures the survival of transplanted organs, making them indispensable in transplant medicine worldwide. As immunosuppressive therapy remains the cornerstone of preventing organ rejection, calcineurin inhibitors continue to dominate this segment.

In the United States, the calcineurin inhibitors market, valued at USD 4.3 billion in 2024, is projected to grow at a CAGR of 8.4% from 2025 to 2034. The U.S. is a key market for these medications, with the presence of world-leading transplant centers, strong reimbursement policies, and a robust investment in research and development driving the market forward. Moreover, the high rates of chronic conditions such as diabetes and hypertension, which often lead to organ failure, further amplify the demand for calcineurin inhibitors. These factors position the U.S. as a dominant force in the global market, ensuring continued growth and innovation within the sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing number of organ transplant procedures

- 3.2.1.2 Rising prevalence of autoimmune diseases

- 3.2.1.3 Surge in immunosuppressive research and development activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects and the availability of alternative treatments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Pipeline analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded

- 5.2.1 Tacrolimus

- 5.2.2 Cyclosporine

- 5.2.3 Other branded products

- 5.3 Generic

- 5.3.1 Tacrolimus

- 5.3.2 Cyclosporine

- 5.3.3 Other generic products

Chapter 6 Market Estimates and Forecast, By Dosage, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Tablets and capsules

- 6.3 Ointments

- 6.4 Injections

- 6.5 Other dosage forms

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Organ transplantation

- 7.3 Autoimmune disease

- 7.4 Other indications

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 abbvie

- 9.2 astellas

- 9.3 Aurinia

- 9.4 Biocon

- 9.5 Dr. Reddy’s

- 9.6 Glenmark

- 9.7 LUPIN

- 9.8 Novartis

- 9.9 Roche

- 9.10 VIATRIS