|

시장보고서

상품코드

1684578

알루미늄캔 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Aluminum Cans Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

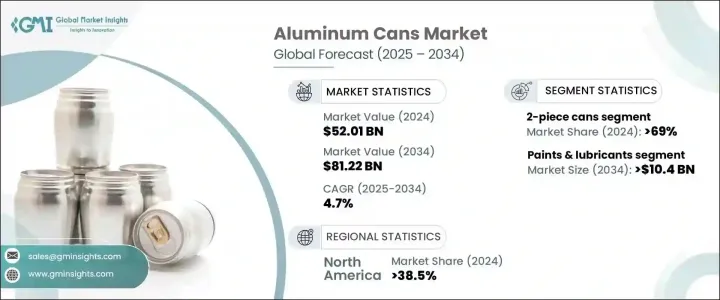

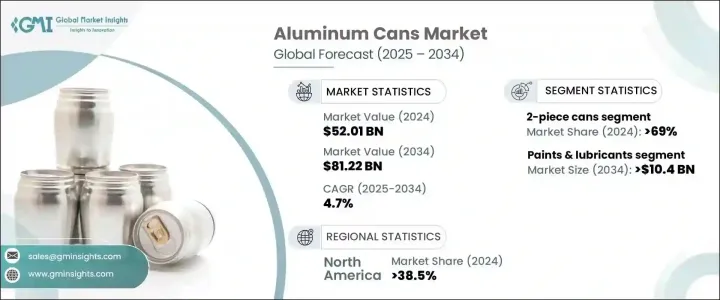

세계의 알루미늄 캔 시장은 2024년 520억 1,000만 달러로 평가되었으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 4.7%로 성장할 것으로 예측됩니다.

지속가능성과 편의성은 시장 동향을 형성하는 주요 요인이며, 알루미늄 캔은 재활용 가능하고 친환경적인 이점이 있기 때문에 지지를 모으고 있습니다. 소비자 선호의 변화가 수요를 더욱 자극하고 프리미엄 음료의 알루미늄 캔 패키지화가 진행되고 있습니다. 건강 지향 소비자는 고품질의 제품을 요구하기 때문에 알루미늄 캔이 들어간 프리미엄 워터, 크래프트 소다, 에너지 음료에 대한 수요가 급증하고 있습니다. 또한, 브랜드는 세계의 지속가능성 목표에 따라 플라스틱 폐기물을 줄이기 위해 알루미늄 캔을 채택하고 있습니다. 인쇄와 브랜딩의 기술적 진보는 제품의 매력을 높이고 음료 제조 업체에게 알루미늄 캔은 매력적인 선택입니다. 이 변화는 업계 전반에 걸쳐 지속 가능한 포장 솔루션으로의 움직임이 확산되고 있음을 반영합니다.

시장은 제품 유형별로 1피스캔, 2피스캔, 3피스캔으로 구분됩니다. 2피스캔이 업계를 선도했으며, 2024년 시장 점유율은 69%를 넘었습니다. 이 캔은 비용 효과, 경량 구조 및 재료 요구 사항을 줄임으로써 생산 비용과 환경에 미치는 영향을 줄이기 위해 인기를 얻고 있습니다. 그 디자인은 운송비와 이산화탄소 배출을 최소화하고 세계적으로 선호되는 옵션입니다. 음료 분야에서는 내구성과 산소와 오염물질로부터 보호하는 능력에 의해 2피스 알루미늄 캔이 널리 채용되어 보다 긴 유통 기한을 보증하고 있습니다. 브랜드화 기술의 향상은 특히 알루미늄 캔 수요가 계속 증가하고 있는 알코올 음료 분야에서 시장 성장을 더욱 촉진하고 있습니다. 재활용 효율이 높고 국제 환경 규제를 준수하기 때문에 알루미늄 캔은 제조업체와 소비자에게 선호되는 옵션이 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 520억 1,000만 달러 |

| 예측 금액 | 812억 2,000만 달러 |

| CAGR | 4.7% |

최종 사용자별로는 식품, 음료, 퍼스널케어 및 화장품, 의약품, 도료 및 윤활유 등으로 분류됩니다. 도료 및 윤활유 분야는 CAGR 8.1% 이상 성장하여 2034년에는 104억 달러 이상에 달할 것으로 예상됩니다. 알루미늄 캔은 경량성, 누설 방지 및 내식성으로 인해 제품의 무결성을 유지하는 데 도움이 되기 때문에 이 분야에서 널리 사용됩니다. 대체 포장과 비교하여, 알루미늄 캔은 지속가능성에 대한 노력에 따라 안전한 보관 및 운송을 보장하는 보다 비용 효율적인 솔루션을 제공합니다. 고성능 코팅제 및 윤활제에 대한 수요 증가는 알루미늄 캔의 채택을 더욱 가속화하고 있습니다. 알루미늄 캔은 제품을 가혹한 조건에서 보호하고 건조 및 누출을 방지하기 때문입니다. 포장 기술의 첨단화에 의해 누출되기 어려운 설계나 탬퍼링 방지도 강화되어, 알루미늄 캔은 산업 분야에서 점점 선호되는 옵션이 되고 있습니다. 도시화와 산업화 동향 증가는 효율적인 포장 솔루션에 대한 수요를 높이고 시장 확대에 기여하고 있습니다.

2024년 시장은 미국의 왕성한 수요에 견인되어 북미가 38.5%의 점유율을 차지해 시장을 선도했습니다. 소비자는 지속가능하고 재활용 가능한 포장을 점점 선호하게 되고, 음료 제조자는 경량 콘테이너 및 재활용 기술의 향상에 주력하게 되고 있습니다. 프리미엄 음료의 상승은 맞춤형 시각에 호소하는 알루미늄 캔 수요를 더욱 촉진하고 있습니다. 기업의 플라스틱에서 벗어나면서 알루미늄 포장이 각광을 받고 있습니다. 인도에서는 환경 의식을 높이고 비용 효율적인 제조 공정으로 시장이 급성장하고 있습니다. 현지 제조업체는 국내외 시장에 적합한 경량 재활용 가능한 캔을 개발하고 있습니다. 지속가능성과 합리적인 가격에 대한 관심 증가는 특히 청량음료와 맥주 산업에서 시장 성장을 지속할 것으로 예상됩니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차

- 2차

- 유료소스

- 공적소스

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 밸류체인에 영향을 주는 요인

- 변혁

- 미래의 전망

- 제조업체

- 유통업체

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 프리미엄 음료 브랜드가 알루미늄 캔 수요를 견인

- 신선도 유지 패키지로서의 알루미늄 캔에 대한 긍정적인 인식

- 알루미늄캔의 높은 재활용률이 시장 수요 촉진

- Ready-to-Drink(RTD) 음료 수요 급증

- 음료 브랜드와 포장의 전략적 파트너십

- 업계의 잠재적 리스크 및 과제

- 수송 중 캔의 함몰이나 손상에 대한 취약성

- 포장 기준의 규제 장벽과 준수 비용

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 1피스 캔

- 2피스 캔

- 3피스 캔

제6장 시장 추계 및 예측 : 용량별, 2021-2034년

- 주요 동향

- 200ml 이하

- 201-450ml

- 451-700ml

- 701-1000ml

- 1000ml 이상

제7장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 식품

- 음료

- 퍼스널케어 및 화장품

- 의약품

- 도료 및 윤활유

- 기타

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Ajanta Bottle

- Albott Containers

- Baixicans

- Ball Corporation

- Canpack

- CCL Industries

- Ceylon Beverage Can

- Crown Holdings

- Envases Group

- GZI Industries

- Nampak

- Orora Packaging

- Scan Holdings

- Shiba Containers

- Silgan Containers

- Swan Industries

- Thai Beverage Can

- Toyo Seikan

The Global Aluminum Cans Market, valued at USD 52.01 billion in 2024, is set to grow at a CAGR of 4.7% from 2025 to 2034. Sustainability and convenience are key drivers shaping market trends, as aluminum cans gain traction due to their recyclability and eco-friendly benefits. Changing consumer preferences have further fueled demand, with premium beverages increasingly packaged in aluminum cans. Health-conscious consumers seek high-quality products, leading to a surge in demand for premium water, craft sodas, and energy drinks in aluminum packaging. Additionally, brands are adopting aluminum cans to align with global sustainability goals and reduce plastic waste. Technological advancements in printing and branding also enhance product appeal, making aluminum cans an attractive choice for beverage companies. This shift reflects a broader move toward sustainable packaging solutions across industries.

The market is segmented by product type into 1-piece, 2-piece, and 3-piece cans, with 2-piece cans leading the industry, holding over 69% market share in 2024. These cans are gaining popularity due to their cost-effectiveness, lightweight structure, and reduced material requirements, which lower production costs and environmental impact. Their design minimizes transportation expenses and carbon emissions, making them a preferred choice globally. The beverage sector widely adopts 2-piece aluminum cans for their durability and ability to protect against oxygen and contaminants, ensuring a longer shelf life. Improved branding techniques further enhance market growth, particularly in the alcoholic beverage segment, where demand for aluminum cans continues to rise. The recycling efficiency and adherence to international environmental regulations make these cans a preferred option among manufacturers and consumers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $52.01 Billion |

| Forecast Value | $81.22 Billion |

| CAGR | 4.7% |

By end-user, the market is categorized into food, beverage, personal care & cosmetics, pharmaceuticals, paints & lubricants, and others. The paints & lubricants segment is expected to grow at a CAGR of over 8.1% and exceed USD 10.4 billion by 2034. Aluminum cans are widely used in this sector due to their lightweight, leak-proof, and corrosion-resistant properties, which help maintain product integrity. Compared to alternative packaging, aluminum cans offer a more cost-effective solution that ensures safe storage and transportation while aligning with sustainability initiatives. Increasing demand for high-performance coatings and lubricants has further accelerated the adoption of aluminum cans, as they protect products from exposure to harsh conditions and prevent drying or leakage. Advancements in packaging technology have also enhanced spill-proof designs and tamper resistance, making aluminum cans an increasingly preferred choice in the industrial sector. The rising trend of urbanization and industrialization is driving higher demand for efficient packaging solutions, contributing to market expansion.

North America led the market in 2024, holding a 38.5% share, driven by strong demand in the United States. Consumers increasingly prefer sustainable and recyclable packaging, prompting beverage manufacturers to focus on lightweight containers and improved recycling technologies. The rise of premium beverages has further fueled demand for customized and visually appealing aluminum cans. As businesses shift away from plastic, aluminum packaging has gained prominence. In India, the market is experiencing rapid growth due to rising environmental awareness and cost-effective manufacturing processes. Local manufacturers are developing lightweight, recyclable cans suitable for domestic and international markets. The increasing focus on sustainability and affordability is expected to sustain market growth, particularly in the soft drink and beer industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Disruptions

- 3.1.3 Future outlook

- 3.1.4 Manufacturers

- 3.1.5 Distributors

- 3.2 Profit margin analysis

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Premium beverage brands driving demand for aluminum cans

- 3.5.1.2 Positive perception of aluminum cans as a freshness retention packaging

- 3.5.1.3 High recycling rate of aluminum cans enhancing market demand

- 3.5.1.4 Surge in demand for ready-to-drink (RTD) beverages

- 3.5.1.5 Strategic partnerships between beverage brands and packaging

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Vulnerability of cans to denting and damage during transportation

- 3.5.2.2 Regulatory barriers and compliance costs for packaging standards

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 1-piece cans

- 5.3 2-piece cans

- 5.4 3-piece cans

Chapter 6 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Up to 200 ml

- 6.3 201 to 450 ml

- 6.4 451 to 700 ml

- 6.5 701 to 1000 ml

- 6.6 more than 1000 ml

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Food

- 7.3 Beverage

- 7.4 Personal care & cosmetic

- 7.5 Pharmaceutical

- 7.6 Paints & lubricants

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Ajanta Bottle

- 9.2 Albott Containers

- 9.3 Baixicans

- 9.4 Ball Corporation

- 9.5 Canpack

- 9.6 CCL Industries

- 9.7 Ceylon Beverage Can

- 9.8 Crown Holdings

- 9.9 Envases Group

- 9.10 GZI Industries

- 9.11 Nampak

- 9.12 Orora Packaging

- 9.13 Scan Holdings

- 9.14 Shiba Containers

- 9.15 Silgan Containers

- 9.16 Swan Industries

- 9.17 Thai Beverage Can

- 9.18 Toyo Seikan