|

시장보고서

상품코드

1684618

협심증 치료제 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Angina Pectoris Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

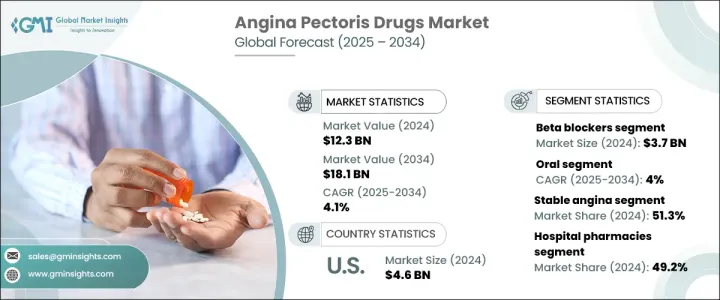

협심증 치료제 세계 시장은 2024년에는 123억 달러로 평가되었고, 2025년부터 2034년에 걸쳐 CAGR 4.1%로 성장할 것으로 예상됩니다.

이 성장은 심혈관 질환의 유병률 증가, 치료법의 상당한 진보, 급속한 노화가 주요 원인입니다. 식생활 교란, 운동 부족, 흡연, 스트레스, 비만 등 라이프 스타일과 관련된 건강 위험 증가는 협심증을 포함한 심혈관 질환의 발생률 상승에 기여합니다. 심장병의 유병률이 계속 상승하면서 효과적인 치료 옵션에 대한 수요도 확대되고 있습니다. 헬스케어 업계는 협심증 환자의 삶의 질 향상을 목표로 하는 기술 혁신으로 대응하고 있습니다. 또한 건강 관리에 대한 인식을 높이고 의료 인프라를 개선하고 약물에 대한 접근성을 높이는 요인이 시장의 성장을 더욱 강화하고 있습니다.

시장은 유형별로 분류되어 안정협심증이 부문을 선도하고 2024년에는 51.3%의 점유율을 차지하고 있습니다. 이 유형의 협심증은 가장 흔하며 예측 가능한 흉통을 특징으로하며 신체적 운동이나 정신적 스트레스에 의해 유발되는 경우가 많습니다. 안정 협심증은 그 유병률을 고려하면 특히 관상 동맥 질환 환자에서 흔히 볼 수 있기 때문에 시장에 큰 영향을 미칩니다. 질산제, 베타 차단제, 칼슘 채널 차단제 등의 확립된 치료 옵션을 이용할 수 있으므로, 이 질환의 효율적인 관리가 가능해져 환자와 헬스케어 전문가 사이에서 널리 사용되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 123억 달러 |

| 예측 금액 | 181억 달러 |

| CAGR | 4.1% |

투여 경로의 관점에서 협심증 치료제 시장은 경구제, 주사제, 외용제로 나뉩니다. 시장 점유율은 경구 약물이 선도하고 있으며 예측 기간 동안 CAGR 4%로 성장할 것으로 예측됩니다. 베타 차단제, 질산제, 칼슘 채널 차단제 등의 경구 약물은 일반적으로 편리함과 저렴한 가격으로 선호됩니다. 협심증 치료에는 건강 관리 시설을 자주 방문할 필요가 없으며, 쉽게 투여할 수 있는 경구약이 제일 선택이 되는 경우가 많습니다. 이러한 치료는 제조 및 유통 비용이 낮고 환자와 의료 제공업체 모두에게 매력적인 선택입니다. 협심증은 장기간의 치료가 필요하기 때문에 경구 약물은 매일 사용하기에 최적이며 환자의 컴플라이언스를 크게 향상시킬 수 있습니다.

미국의 협심증 치료제 시장은 2024년에 46억 달러가 되어 시장 전체의 성장을 견인하는 중요한 역할을 담당하고 있습니다. 이 나라에서는 협심증의 유병률이 증가하고 있으며, 보다 효과적인 치료법에 대한 수요도 함께 시장 확대에 박차를 가하고 있습니다. 게다가 미국은 의학연구와 기술 혁신의 리더가 되고 있으며, 선진적인 병용요법이나 β차단제의 강화 등 협심증 치료에 있어서 지속적인 개발이 시장 성장을 더욱 가속화하고 있습니다. 이러한 의약품 개발의 일관된 진보는 이 나라의 견고한 헬스케어 인프라와 함께 미국을 세계 시장의 미래 성공에 크게 공헌하는 나라로 자리매김하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 심혈관 질환의 유병률의 상승

- 의약품 개발의 진보

- 라이프 스타일과 관련된 위험 인자 증가

- 업계의 잠재적 위험 및 과제

- 약제에 따른 부작용

- 저침습 수술의 채용 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정 및 예측 : 유형별, 2021년-2034년

- 주요 동향

- 안정협심증

- 불안정 협심증

- 미세혈관협심증

- 협심증

제6장 시장 추정 및 예측 : 약제 클래스별, 2021년-2034년

- 주요 동향

- β차단제

- 질산약

- 항혈소판약

- 칼슘 채널 차단제

- 항응고제

- ACE 억제제

- 약제 클래스별

제7장 시장 추정 및 예측 : 투여 경로별, 2021년-2034년

- 주요 동향

- 경구제

- 주사제

- 국소

제8장 시장 추정 및 예측 : 유통 채널별, 2021년-2034년

- 주요 동향

- 병원 약국

- 소매 약국

- 온라인 약국

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- AdvaCare Pharma

- Amgen

- AstraZeneca

- Bayer

- Boehringer Ingelheim International

- Eli Lilly and Company

- Gilead Sciences

- GlaxoSmithKline

- Merck

- Novartis

- Otsuka Pharmaceutical

- Pfizer

- Sanofi

The Global Angina Pectoris Drugs Market was valued at USD 12.3 billion in 2024 and is expected to grow at a steady rate of 4.1% CAGR between 2025 and 2034. This growth is largely driven by the increasing prevalence of cardiovascular diseases, significant advancements in therapeutic treatments, and a rapidly aging population. The rise in lifestyle-related health risks-such as poor diets, lack of physical activity, smoking, stress, and obesity-has contributed to a higher incidence of cardiovascular conditions, including angina. As the prevalence of heart disease continues to rise, the demand for effective treatment options is also expanding. The healthcare industry is responding with innovations aimed at improving the quality of life for patients dealing with angina. Additionally, factors such as rising healthcare awareness, improved healthcare infrastructure, and increasing accessibility to medication are further fueling the growth of this market.

The market is categorized by type, with stable angina leading the segment, accounting for a 51.3% share in 2024. This form of angina is the most common and is characterized by chest pain that is predictable and often triggered by physical exertion or emotional stress. Given its prevalence, stable angina has a significant impact on the market, especially as it is commonly found in patients with coronary artery disease. The availability of well-established treatment options-such as nitrates, beta-blockers, and calcium channel blockers-ensures efficient management of the condition, encouraging their widespread use among patients and healthcare professionals alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.3 Billion |

| Forecast Value | $18.1 Billion |

| CAGR | 4.1% |

In terms of administration route, the angina pectoris drug market is divided into oral, injectable, and topical formulations. Oral medications take the lead in terms of market share and are projected to grow at a 4% CAGR throughout the forecast period. Oral drugs, such as beta-blockers, nitrates, and calcium channel blockers, are commonly preferred due to their convenience and affordability. They are often the first choice for treating angina, as they can be easily administered without the need for frequent visits to healthcare facilities. These treatments offer lower manufacturing and distribution costs, making them an attractive option for both patients and providers. Given that angina pectoris requires long-term treatment, oral medications are ideal for daily use and can significantly enhance patient compliance.

The U.S. angina pectoris drug market, valued at USD 4.6 billion in 2024, plays a critical role in driving the overall market growth. The country's increasing prevalence of angina, combined with a demand for more effective therapies, has spurred market expansion. Moreover, the U.S. continues to be a leader in medical research and innovation, with ongoing developments in angina treatments, including advanced combination therapies and enhanced beta blockers, further accelerating market growth. This consistent advancement in drug development, coupled with the country's robust healthcare infrastructure, positions the U.S. as a significant contributor to the future success of the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiovascular diseases

- 3.2.1.2 Advancements in drug development

- 3.2.1.3 Increasing lifestyle-related risk factors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects associated with the drugs

- 3.2.2.2 Growing adoption of minimally invasive surgeries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Stable angina

- 5.3 Unstable angina

- 5.4 Microvascular angina

- 5.5 Prinzmetal angina

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Beta blockers

- 6.3 Nitrates

- 6.4 Anti-platelets

- 6.5 Calcium channel blockers

- 6.6 Anticoagulants

- 6.7 ACE inhibitors

- 6.8 Other drug classes

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

- 7.4 Topical

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AdvaCare Pharma

- 10.2 Amgen

- 10.3 AstraZeneca

- 10.4 Bayer

- 10.5 Boehringer Ingelheim International

- 10.6 Eli Lilly and Company

- 10.7 Gilead Sciences

- 10.8 GlaxoSmithKline

- 10.9 Merck

- 10.10 Novartis

- 10.11 Otsuka Pharmaceutical

- 10.12 Pfizer

- 10.13 Sanofi