|

시장보고서

상품코드

1684658

산업용 레이저 시스템 시장 : 기회, 성장 촉진요인, 산업 동향 분석(2025-2034년)Industrial Laser Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

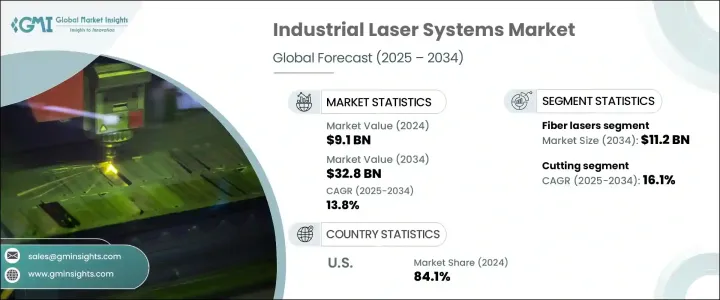

세계의 산업용 레이저 시스템 시장은 2024년에 91억 달러로 평가되었고, 2025년부터 2034년까지의 CAGR은 13.8%를 나타낼 전망입니다. 이러한 급증은 주로 제조, 자동차, 전자, 항공우주 등 다양한 산업에서 자동화 도입이 가속화되고 있기 때문입니다. 업계에서 운영 효율성, 정밀도, 비용 절감을 위해 노력함에 따라 이러한 첨단 레이저 기술에 대한 수요는 계속 증가하고 있습니다. 디지털 제조와 스마트 팩토리 솔루션에 초점을 맞춘 자동화 및 인더스트리 4.0 노력은 이러한 시스템의 필요성을 더욱 증폭시키고 있습니다. 산업용 레이저 시스템은 더 높은 생산성을 보장할 뿐만 아니라 다양한 분야에서 복잡한 설계와 고품질 출력물에 대한 증가하는 수요를 충족할 수 있도록 지원합니다.

파이버 레이저 분야는 2034년까지 112억 달러를 달성하여 시장의 주요 촉진요인 중 하나가 될 것으로 예측되고 있습니다. 파이버 레이저는 탁월한 에너지 효율성, 신뢰성, 다용도성으로 인해 상당한 주목을 받고 있습니다. 금속에서 플라스틱에 이르기까지 다양한 재료와 원활하게 작동하는 능력과 탁월한 빔 품질 덕분에 고정밀 레이저 작업이 필요한 산업에서 선호되는 선택입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 91억 달러 |

| 예측 금액 | 328억 달러 |

| CAGR | 13.8% |

다양한 용도 중에서 절단 분야가 가장 급성장하고 있으며 예측 기간 중 CAGR은 16.1%를 나타낼 전망입니다. 레이저 절단 시스템은 수많은 재료를 정밀하게 가공할 수 있어 유연성, 정확성, 일관성을 제공합니다.

2024년 미국은 산업용 레이저 시스템 시장에서 84.1%로 압도적인 점유율을 차지하고 있습니다. 이러한 우위는 자동화 및 레이저 기술 개발에 대한 막대한 투자와 함께 미국의 잘 구축된 제조 인프라에 기인한 것으로 볼 수 있습니다. 또한 지속적인 연구 개발 자금 지원과 함께 정부의 지원 정책이 이 분야의 성장을 가속화하고 있습니다. 산업용 레이저 시스템과 디지털 제조 및 스마트 팩토리 전략의 통합으로 채택이 확대되면서 미국의 다양한 산업 응용 분야에서 지속적인 수요가 증가하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차

- 2차

- 유료

- 공적

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혼란

- 장래의 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향요인

- 성장 촉진요인

- 산업 전반에 걸친 자동화 채택 증가

- 레이저 기술의 발전

- 소형화 및 고정밀 부품에 대한 수요 증가

- 신흥 산업에서의 용도의 확대

- 제조 기술에 대한 정부 지원 및 투자

- 업계의 잠재적 위험 및 과제

- 높은 초기 투자 및 운영 비용

- 기술적 복잡성과 제한된 숙련된 인력

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계 및 예측 : 레이저 유형별(2021-2034년)

- 주요 동향

- 파이버 레이저

- 고체 레이저

- CO2 레이저

- 다이오드 레이저

- 기타 레이저

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 절단

- 용접

- 마킹

- 드릴링

- 조각

- 기타 산업용도

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 반도체 및 전자 제품 제조

- 자동차 제조

- 항공 우주 및 방위

- 의료 기기

- 금속 가공 및 기계

- 가전

- 기타

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- ALPHA Laser GmbH

- Amada Co., Ltd.

- Bystronic AG

- Coherent, Inc.

- EKSPLA

- FANUC Corporation

- Hanslaser Technology Co., Ltd.

- IPG Photonics Corporation

- Jenoptik AG

- Lasea SA

- Laserline GmbH

- Lumentum Holdings Inc.

- Lumibird Group

- Mitsubishi Electric Corporation

- NKT Photonics A/S

- Prima Industrie SpA

- Synrad, Inc.

- Telesis Technologies, Inc.

- Trumpf GmbH Co. KG

- Universal Laser Systems, Inc.

The Global Industrial Laser Systems Market, valued at USD 9.1 billion in 2024, is poised for significant growth, with a projected CAGR of 13.8% from 2025 to 2034. This surge is largely driven by the accelerating adoption of automation across various industries such as manufacturing, automotive, electronics, and aerospace. Industrial laser systems are becoming indispensable in modern production lines due to their ability to deliver high precision and efficiency in processes like cutting, welding, engraving, and marking. As industries strive for greater operational efficiency, precision, and reduced costs, the demand for these advanced laser technologies continues to grow. Automation and Industry 4.0 initiatives, which focus on digital manufacturing and smart factory solutions, further amplify the need for these systems. Industrial laser systems not only ensure higher productivity but also enable businesses to meet the increasing demand for intricate designs and high-quality outputs across various sectors.

The fiber laser segment is expected to achieve USD 11.2 billion by 2034, becoming one of the market's leading drivers. Fiber lasers are gaining significant traction due to their unmatched energy efficiency, reliability, and versatility. Their ability to work seamlessly with a variety of materials-ranging from metals to plastics-coupled with their exceptional beam quality, makes them the preferred choice for industries requiring high-precision laser operations. Moreover, fiber lasers are celebrated for their low maintenance and compact design, which make them ideal for a wide array of industrial applications. As technological advancements continue to unfold, the range of applications for fiber lasers expands, contributing to this segment's impressive growth forecast.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.1 Billion |

| Forecast Value | $32.8 Billion |

| CAGR | 13.8% |

Among various applications, the cutting segment is projected to be the fastest-growing, with an anticipated CAGR of 16.1% during the forecast period. The demand for precise and high-speed cutting solutions is skyrocketing as industries seek to minimize material waste and optimize operational efficiency. Laser cutting systems enable the precise processing of numerous materials, providing flexibility, accuracy, and consistency. As industrial production increasingly embraces automation, laser cutting systems are becoming integral to cutting-edge manufacturing processes, particularly with the integration of high-power laser technologies that enhance performance and throughput.

In 2024, the United States accounted for a dominant 84.1% share of the industrial laser systems market. This dominance can be attributed to the country's well-established manufacturing infrastructure, along with substantial investments in automation and laser technology development. Moreover, supportive government policies, along with ongoing research and development funding, are accelerating growth in this sector. The integration of industrial laser systems with digital manufacturing and smart factory initiatives only broadens their adoption, driving sustained demand across diverse industrial applications in the U.S.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising adoption of automation across industries

- 3.6.1.2 Advancements in laser technology

- 3.6.1.3 Growing demand for miniaturized and high-precision components

- 3.6.1.4 Expanding applications in emerging industries

- 3.6.1.5 Government support and investments in manufacturing technologies

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial investment and operating costs

- 3.6.2.2 Technical complexity and limited skilled workforce

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type of Laser, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Fiber lasers

- 5.3 Solid-state lasers

- 5.4 CO2 lasers

- 5.5 Diode lasers

- 5.6 Other laser types

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Cutting

- 6.3 Welding

- 6.4 Marking

- 6.5 Drilling

- 6.6 Engraving

- 6.7 Other industrial applications

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Semiconductor and electronics manufacturing

- 7.3 Automotive manufacturing

- 7.4 Aerospace and defense

- 7.5 Medical devices

- 7.6 Metal fabrication and machinery

- 7.7 Consumer electronics

- 7.8 Other industrial sectors

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ALPHA Laser GmbH

- 9.2 Amada Co., Ltd.

- 9.3 Bystronic AG

- 9.4 Coherent, Inc.

- 9.5 EKSPLA

- 9.6 FANUC Corporation

- 9.7 Hanslaser Technology Co., Ltd.

- 9.8 IPG Photonics Corporation

- 9.9 Jenoptik AG

- 9.10 Lasea S.A.

- 9.11 Laserline GmbH

- 9.12 Lumentum Holdings Inc.

- 9.13 Lumibird Group

- 9.14 Mitsubishi Electric Corporation

- 9.15 NKT Photonics A/S

- 9.16 Prima Industrie S.p.A.

- 9.17 Synrad, Inc.

- 9.18 Telesis Technologies, Inc.

- 9.19 Trumpf GmbH + Co. KG

- 9.20 Universal Laser Systems, Inc.