|

시장보고서

상품코드

1684686

중앙 차량 컨트롤러 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Central Vehicle Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

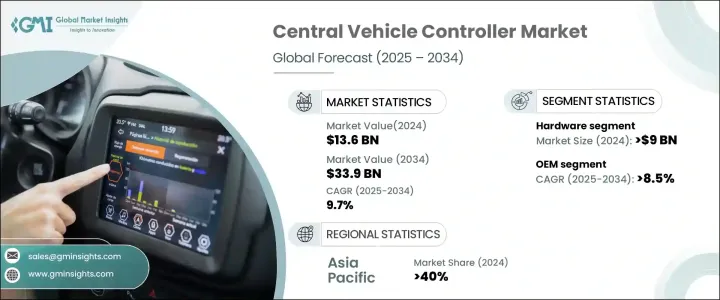

중앙차량 컨트롤러 세계 시장은 2024년 136억 달러로 평가되었으며, 전기차(EV)의 보급과 첨단 차량 제어 시스템에 대한 요구 증가를 배경으로 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 9.7%로 성장할 것으로 예상됩니다.

자동차 제조업체가 효율성을 높이고 하드웨어 복잡성을 줄이는 혁신적인 솔루션을 찾는 동안 CVC는 최신 차량 아키텍처의 핵심 구성 요소로 부상하고 있습니다. 이 컨트롤러는 여러 차량 기능을 중앙 집중식 시스템에 통합하여 에너지 최적화, 실시간 데이터 활용, 차량 전반의 성능을 향상시킵니다. 제어 조작을 간소화함으로써 제조업체는 적응형 크루즈 컨트롤, 레인키핑 어시스턴스, 자율 주행 기능 등의 지능형 기능을 통합할 수 있습니다.

차량의 전기화와 커넥티비티가 업계의 우선사항이 되는 가운데, 이러한 선진적인 컨트롤러 수요는 계속 급증하고 있습니다. 또한 스마트 이동성 솔루션과 소프트웨어 정의 차량의 상승이 CVC 기술에 대한 투자를 더욱 가속화하여 자동차 제조업체는 성능, 안전성 및 지속가능성을 높일 수 있습니다. 저배출 가스와 차량 효율 향상을 요구하는 규제 압력이 높아짐에 따라 자동차 업계는 뛰어난 기능성, 비용 절감, 진화하는 모빌리티 에코시스템과의 원활한 통합을 실현하는 집중 제어 아키텍처로의 전환을 적극적으로 진행하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 136억 달러 |

| 예측 금액 | 339억 달러 |

| CAGR | 9.7% |

시장은 하드웨어 구성 요소와 소프트웨어 구성 요소로 구분되며, 2024년에는 하드웨어 부문이 90억 달러로 우위를 차지했습니다. 이 부문의 급격한 확대는 중앙 집중식 차량 제어를 지원하는 고성능 컴퓨팅 시스템에 대한 수요 증가로 인한 것입니다. 이러한 하드웨어 솔루션은 실시간 네비게이션, 자동 브레이크, 예지 보전 등 고급 차량 기능을 구현하는 데 중요한 역할을 합니다. EV의 증산과 ADAS(선진운전지원시스템)의 추진에 따라 자동차 제조업체는 차량의 인텔리전스와 응답성을 높이는 에너지 효율적인 하드웨어 솔루션에 많은 투자를 하고 있습니다. 자동차 기술이 발전함에 따라 강력한 프로세서, 첨단 센서 및 인공지능 기반 제어 시스템의 통합이이 부문의 추가 성장을 가속할 것으로 예상됩니다.

최종 용도별로 시장은 상대방 브랜드 제조(OEM)와 애프터마켓으로 분류되며, OEM은 이 부문을 선도하고 있습니다. OEM 시장은 2025년부터 2034년에 걸쳐 CAGR 8.5%로 성장할 것으로 예상됩니다. 이는 자동차 제조업체의 집중형 차량 아키텍처로의 시프트가 원동력이 되고 있습니다. 이러한 시스템을 통해 제조업체는 생산 공정을 간소화하고 하드웨어 중복성을 줄이고 차량 효율을 높일 수 있습니다. CVC 통합을 통해 자동차 제조업체는 배기 가스, 사이버 보안 및 차량 안전에 대한 엄격한 규제 기준을 충족할 수 있습니다. 자동차가 소프트웨어 중심이 됨에 따라 OEM은 연결성 향상, 유지 보수 비용 절감, 차량 설계의 미래를 고려하여 이러한 시스템의 채택을 선호합니다.

아시아태평양은 여전히 가장 규모가 큰 지역 시장이며 2024년 세계 점유율의 40%를 차지했습니다. 이 지역의 우위는 EV 채용 증가, 정부의 강력한 인센티브, 자동차 기술의 대폭적인 진보에 의해 추진되고 있습니다. 중국, 일본, 한국 등의 국가들은 자동차의 전동화에 많은 투자를 하고 있으며, 자동차 제조업체는 에너지 관리와 성능을 강화하기 위해 집중 제어 시스템의 통합을 촉구하고 있습니다. 세제 우대 조치, 배출 감축 의무, 스마트 이동성 인프라에 대한 투자가이 지역에서 CVC 기술의 채택을 더욱 가속화하고 있습니다. 지능형 운송 솔루션에 대한 관심이 높아짐에 따라 아시아태평양은 세계 중앙 차량 컨트롤러 시장에서 리더십을 유지할 것으로 예상됩니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도의 산출

- 시장추계의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 범위와 정의

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 부품 제조업체

- 제조업체

- 유통업체

- 최종 사용자

- 이익률 분석

- 기술 혁신의 상황

- 특허 분석

- 규제 상황

- 비용 분석

- ADAS(선진 운전 지원 시스템)의 진화

- 영향요인

- 성장 촉진요인

- ADAS(선진 운전 지원 시스템) 수요 증가

- 전기차 및 하이브리드차의 채용 증가

- 자동차의 안전성과 규제 준수의 중시의 고조

- 커넥티비티와 스마트 차량 기능의 통합에 대한 주목 증가

- 업계의 잠재적 위험 및 과제

- 시스템 개발 비용의 높이

- CVC 시스템과 기존 자동차 플랫폼 간의 통합 복잡성

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 컴포넌트별, 2021년-2034년

- 주요 동향

- 하드웨어

- 마이크로컨트롤러

- 메모리 유닛

- 통신 모듈

- 컨트롤러 영역 네트워크(CAN)

- 로컬 인터커넥트 네트워크(LIN)

- 플렉스 레이

- 이더넷

- 기타

- 소프트웨어

- 운영 체제

- 미들웨어

- 용도 소프트웨어

제6장 시장 추정 및 예측 : 차량별, 2021년-2034년

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

제7장 시장 추정 및 예측 : 추진력별, 2021년-2034년

- 주요 동향

- ICE

- 전기자동차

- 배터리 전기자동차(BEV)

- 플러그인 하이브리드 자동차(PHEV)

- 하이브리드 전기자동차(HEV)

제8장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- ADAS와 안전 시스템

- 바디 컨트롤 & 컴포트 시스템

- 파워트레인 매니지먼트

- 인포테인먼트 시스템

- 차량 다이나믹스 & 컨트롤

- 기타

제9장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- Aptiv

- Bosch

- Continental

- Denso

- Ford Motors

- General Motors

- 현대자동차

- Infineon Technologies

- Magna International

- NVIDIA

- NXP Semiconductors

- Qualcomm

- Renesas Electronics

- STMicroelectronics

- Tesla

- Texas Instruments

- Toyota Motor

- Valeo

- Volkswagen

- ZF Friedrichshafen

The Global Central Vehicle Controller Market was valued at USD 13.6 billion in 2024 and is poised to expand at a CAGR of 9.7% between 2025 and 2034, driven by the increasing adoption of electric vehicles (EVs) and the growing need for advanced vehicle control systems. As automakers seek innovative solutions to enhance efficiency and reduce hardware complexity, CVCs have emerged as a critical component in modern vehicle architecture. These controllers consolidate multiple vehicle functions into a centralized system, improving energy optimization, real-time data utilization, and overall vehicle performance. By streamlining control operations, CVCs enable manufacturers to integrate intelligent features such as adaptive cruise control, lane-keeping assistance, and autonomous driving capabilities.

With vehicle electrification and connectivity becoming industry priorities, the demand for these advanced controllers continues to surge. Additionally, the rise of smart mobility solutions and software-defined vehicles has further fueled investments in CVC technologies, allowing automakers to enhance performance, safety, and sustainability. As regulatory pressures for lower emissions and enhanced vehicle efficiency grow, the automotive industry is actively transitioning toward centralized control architectures that offer superior functionality, reduced costs, and seamless integration with evolving mobility ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.6 Billion |

| Forecast Value | $33.9 Billion |

| CAGR | 9.7% |

The market is segmented into hardware and software components, with the hardware segment dominating in 2024 at USD 9 billion. The rapid expansion of this segment is attributed to the rising demand for high-performance computing systems that support centralized vehicle control. These hardware solutions play a crucial role in enabling sophisticated vehicle functionalities, including real-time navigation, automated braking, and predictive maintenance. With the increasing production of EVs and the push for advanced driver assistance systems (ADAS), automakers are investing heavily in energy-efficient hardware solutions that enhance vehicle intelligence and responsiveness. As automotive technology advances, the integration of powerful processors, advanced sensors, and artificial intelligence-based control systems is expected to drive further growth in this segment.

By end-use, the market is categorized into original equipment manufacturers (OEMs) and the aftermarket, with OEMs leading the segment. The OEM market is projected to expand at a CAGR of 8.5% from 2025 to 2034, driven by automakers' shift toward centralized vehicle architectures. These systems allow manufacturers to streamline production processes, reduce hardware redundancy, and enhance vehicle efficiency. The integration of CVCs enables automakers to meet stringent regulatory standards related to emissions, cybersecurity, and vehicle safety. As vehicles become more software-centric, OEMs are prioritizing the adoption of these systems to improve connectivity, reduce maintenance costs, and future-proof their vehicle designs.

Asia Pacific remains the largest regional market, accounting for 40% of the global share in 2024. The region's dominance is fueled by the rising adoption of EVs, strong government incentives, and significant advancements in automotive technology. Countries such as China, Japan, and South Korea are investing heavily in vehicle electrification, prompting automakers to integrate centralized control systems for enhanced energy management and performance. Tax benefits, emission reduction mandates, and investments in smart mobility infrastructure further accelerate the adoption of CVC technologies in the region. With a growing focus on intelligent transportation solutions, Asia Pacific is expected to maintain its leadership in the global central vehicle controller market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Manufacturers

- 3.2.3 Distributors

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Cost analysis

- 3.8 Evolution of Advanced Driver Assistance Systems (ADAS)

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for Advanced Driver Assistance Systems (ADAS)

- 3.9.1.2 Rising adoption of electric and hybrid vehicles

- 3.9.1.3 Growing emphasis on vehicle safety and regulatory compliance

- 3.9.1.4 Enhanced focus on connectivity and integration of smart vehicle features

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High cost of system development

- 3.9.2.2 Integration complexity of CVC systems with existing automotive platforms

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Microcontroller

- 5.2.2 Memory unit

- 5.2.3 Communication module

- 5.2.3.1 Controller Area Network (CAN)

- 5.2.3.2 Local Interconnect Network (LIN)

- 5.2.3.3 FlexRay

- 5.2.3.4 Ethernet

- 5.2.4 Others

- 5.3 Software

- 5.3.1 Operating system

- 5.3.2 Middleware

- 5.3.3 Application software

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric vehicles

- 7.3.1 Battery Electric Vehicles (BEV)

- 7.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 7.3.3 Hybrid Electric Vehicles (HEV)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 ADAS & safety system

- 8.3 Body control & comfort system

- 8.4 Powertrain management

- 8.5 Infotainment system

- 8.6 Vehicle dynamics and control

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Bosch

- 11.3 Continental

- 11.4 Denso

- 11.5 Ford Motors

- 11.6 General Motors

- 11.7 Hyundai Motors

- 11.8 Infineon Technologies

- 11.9 Magna International

- 11.10 NVIDIA

- 11.11 NXP Semiconductors

- 11.12 Qualcomm

- 11.13 Renesas Electronics

- 11.14 STMicroelectronics

- 11.15 Tesla

- 11.16 Texas Instruments

- 11.17 Toyota Motor

- 11.18 Valeo

- 11.19 Volkswagen

- 11.20 ZF Friedrichshafen